|

|

|

AGENDA

Audit & Risk Committee meeting

Monday, 23 February 2026

|

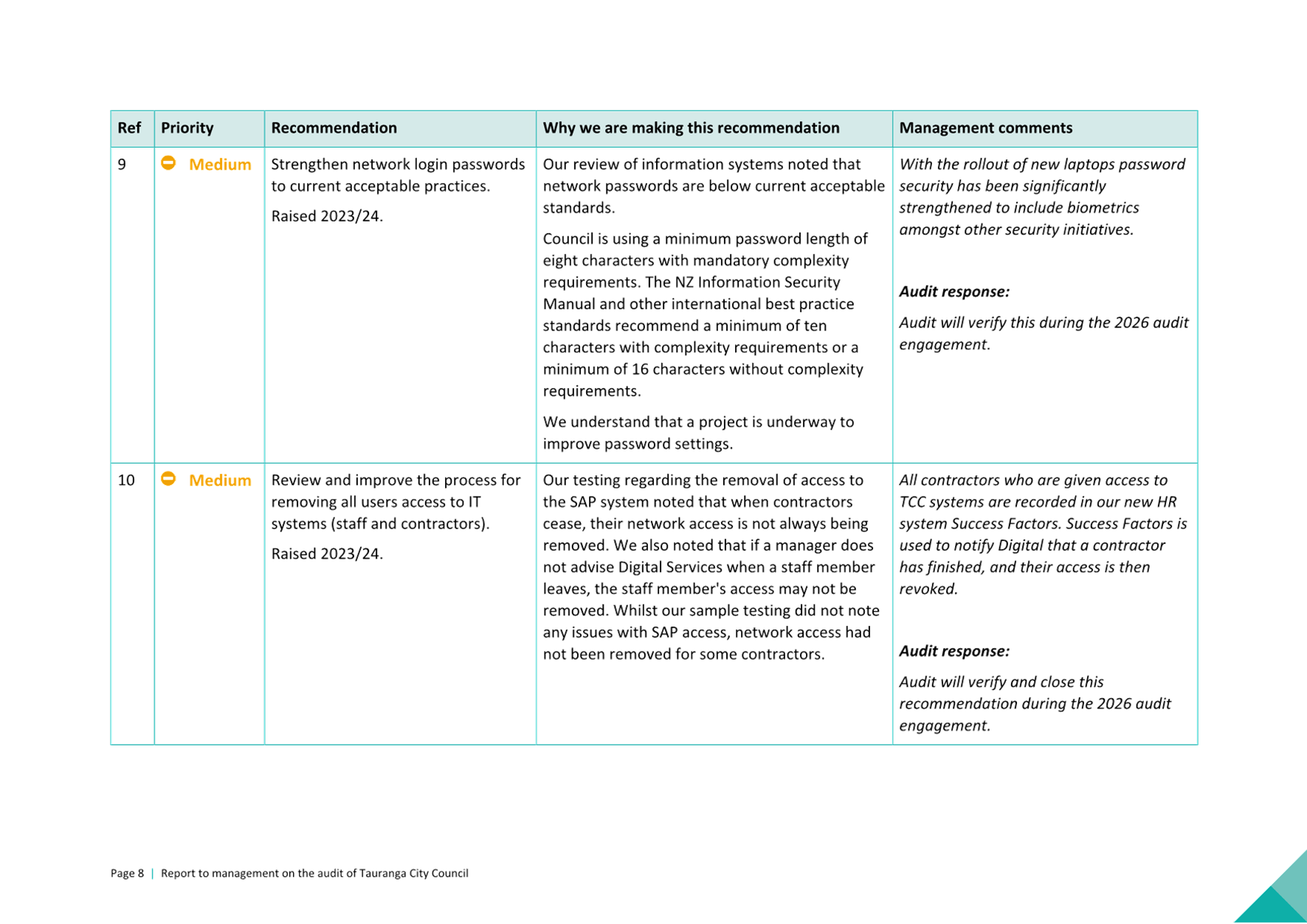

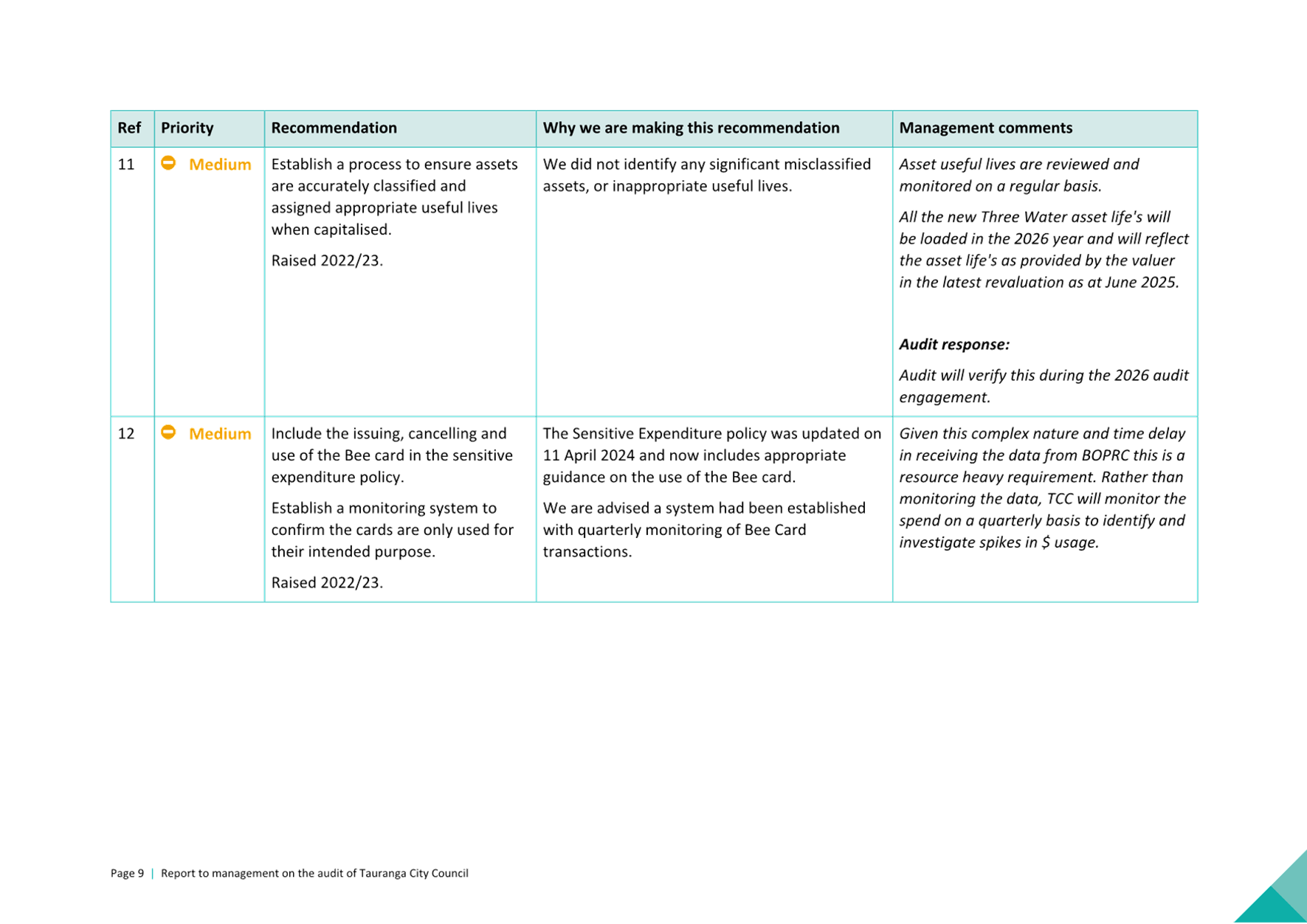

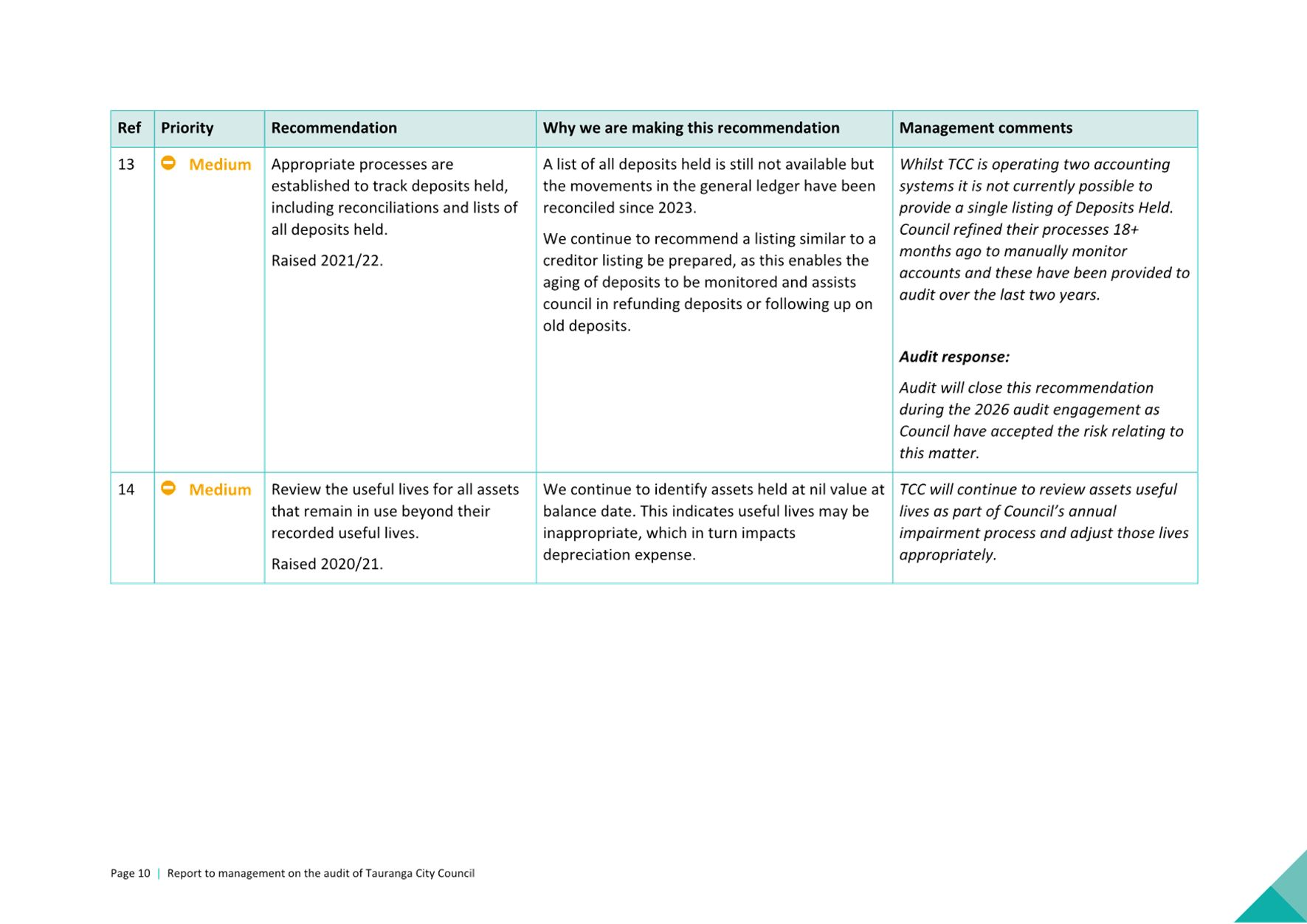

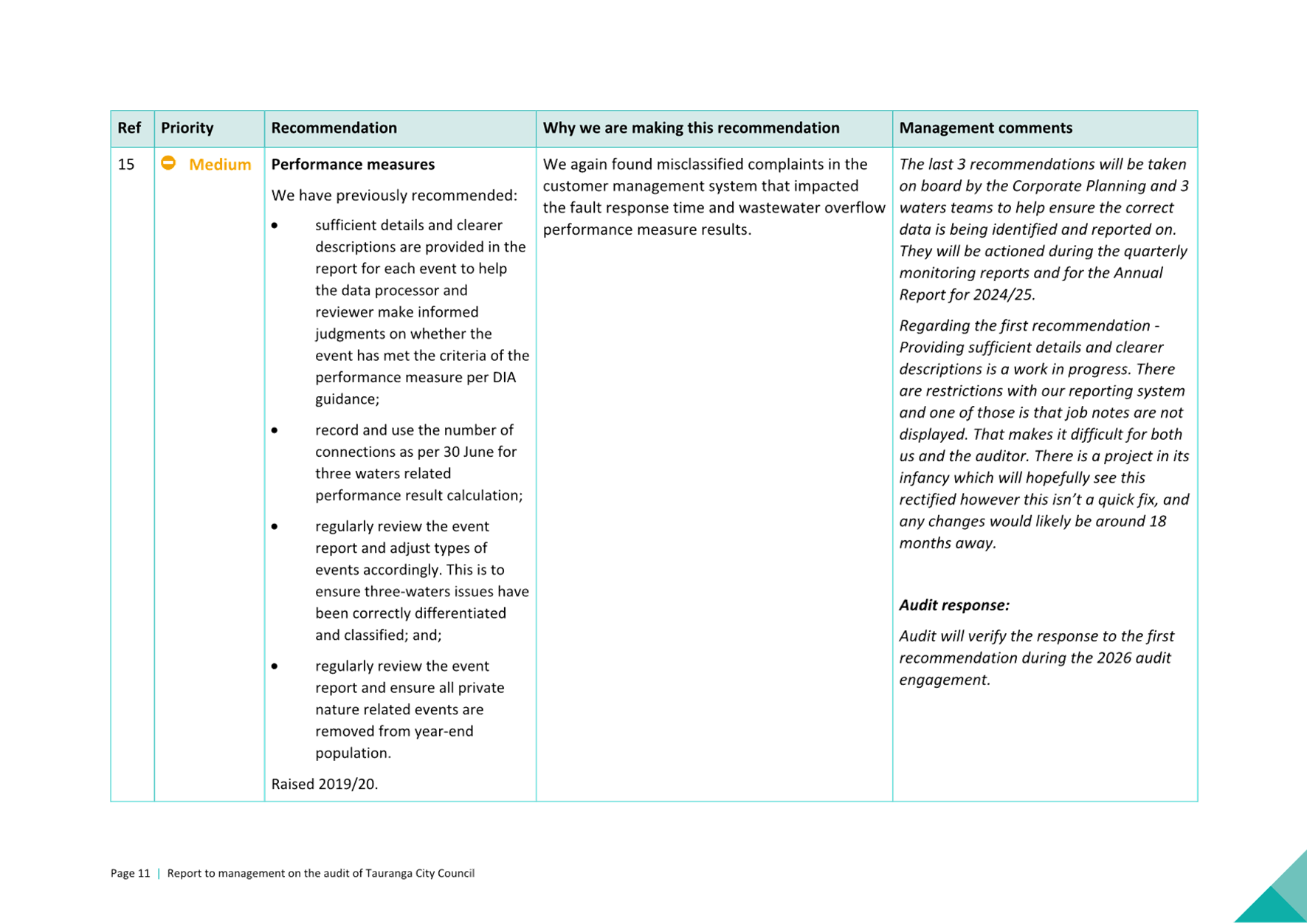

|

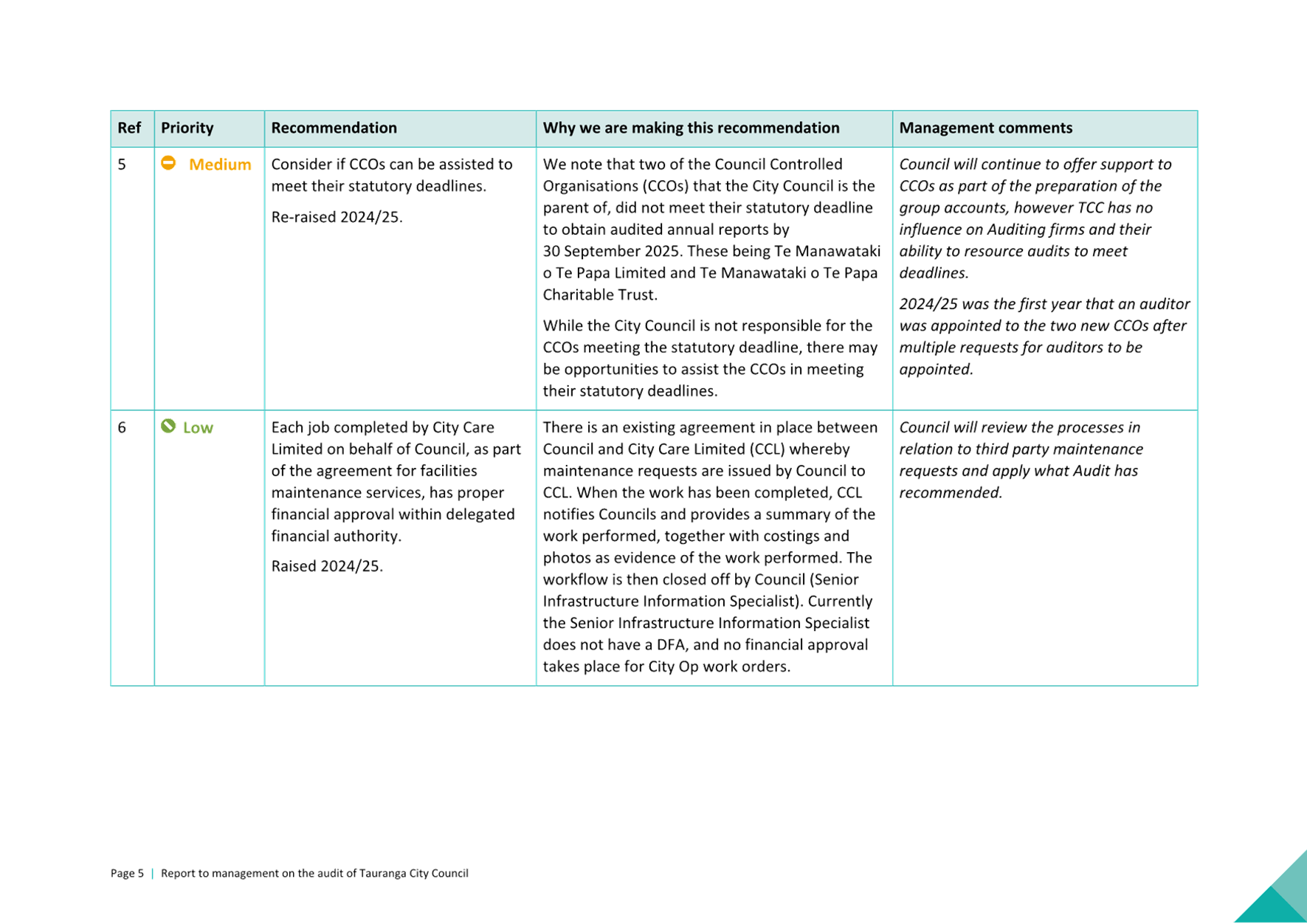

I hereby give notice that a Audit & Risk

Committee meeting will be held on:

|

|

Date:

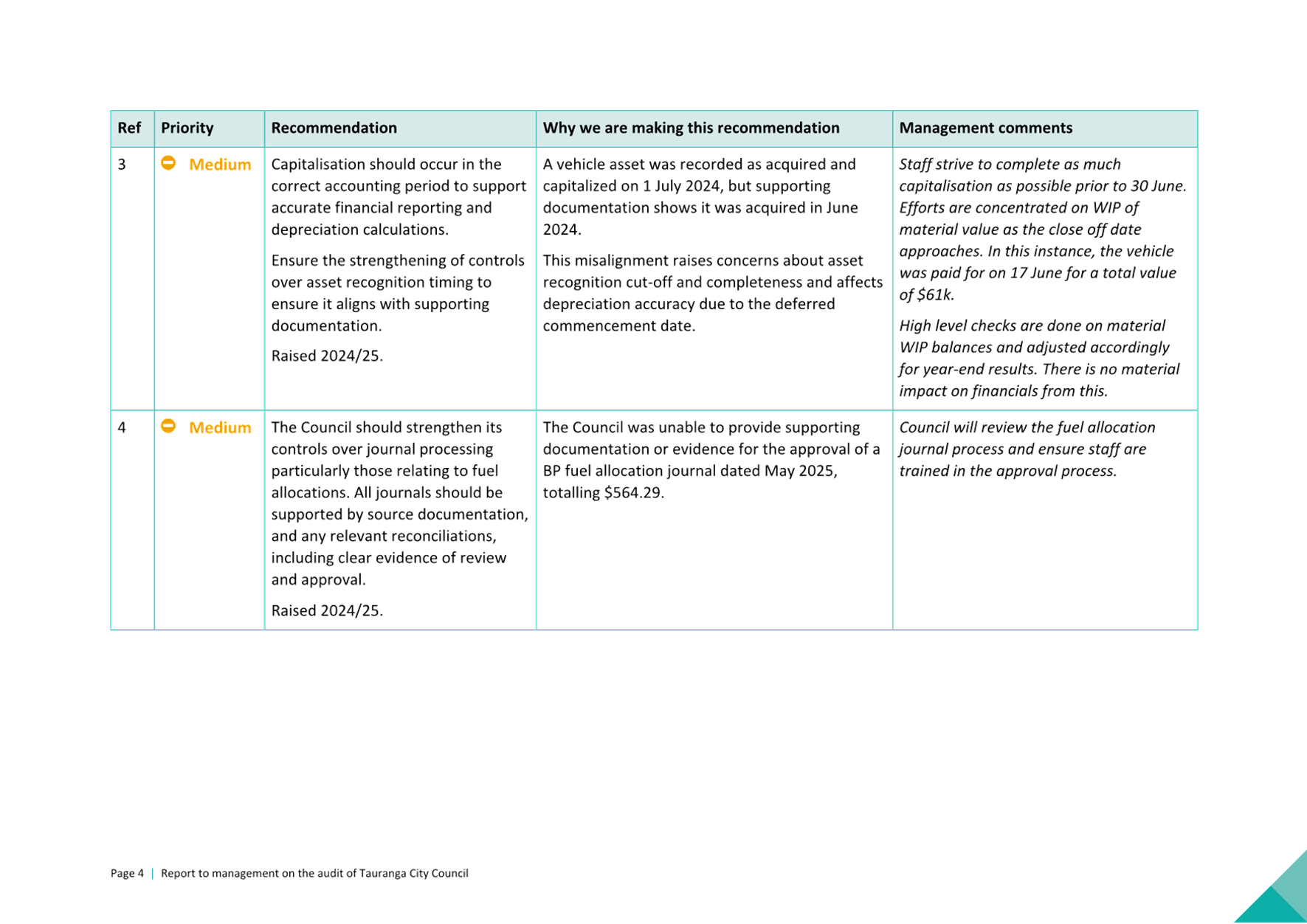

|

Monday, 23 February 2026

|

|

Time:

|

9:00 am

|

|

Location:

|

Tauranga City Council Chambers

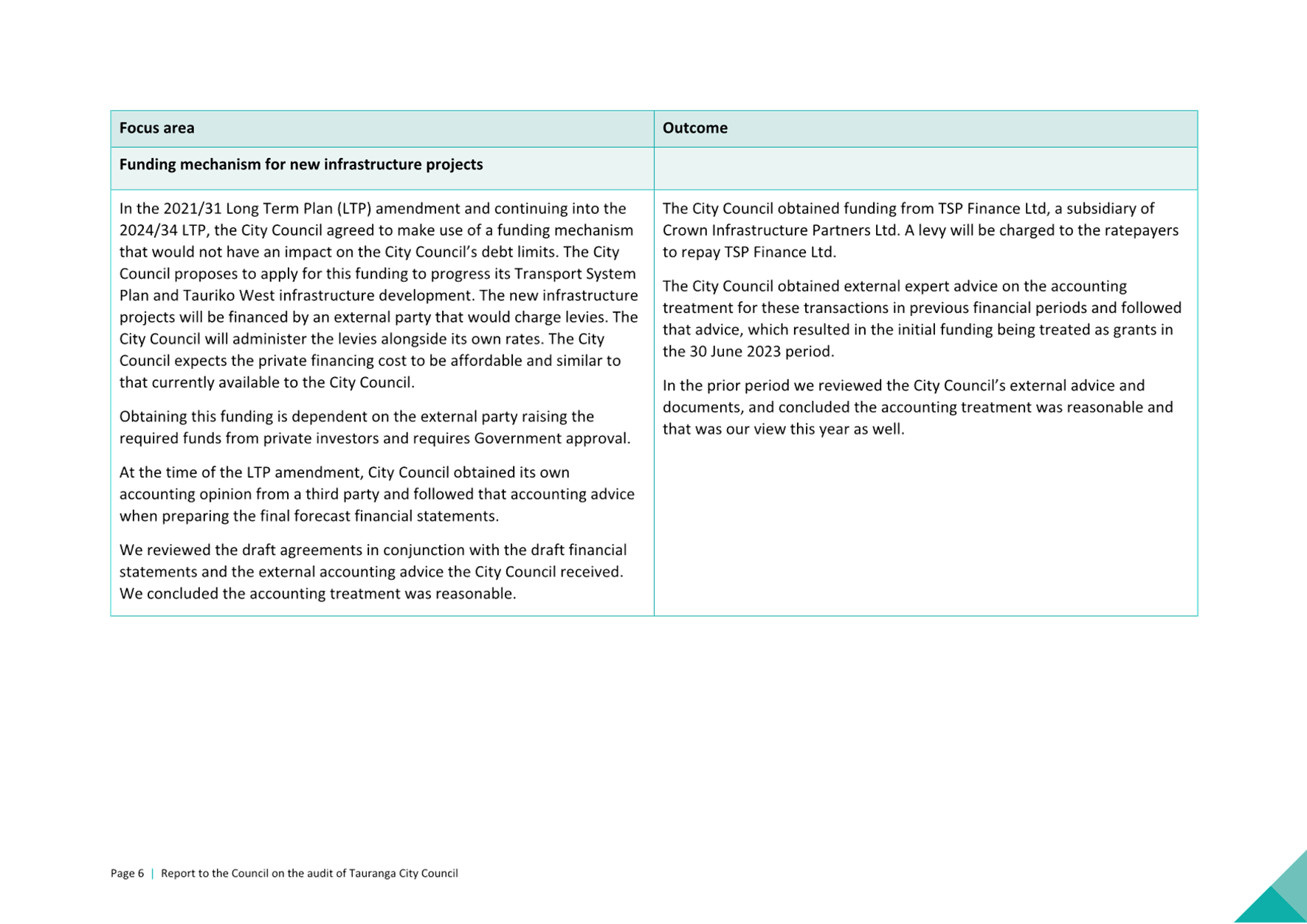

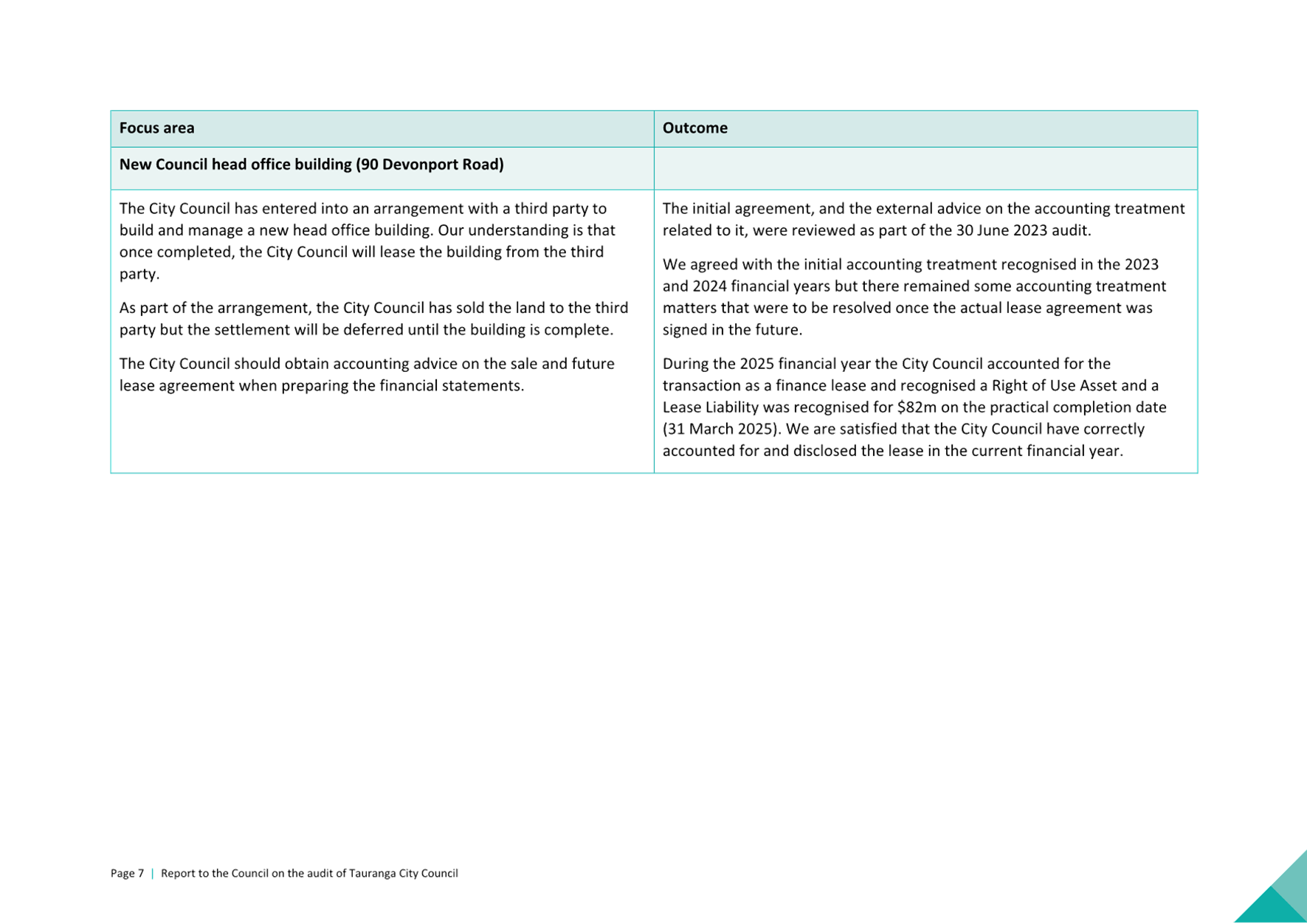

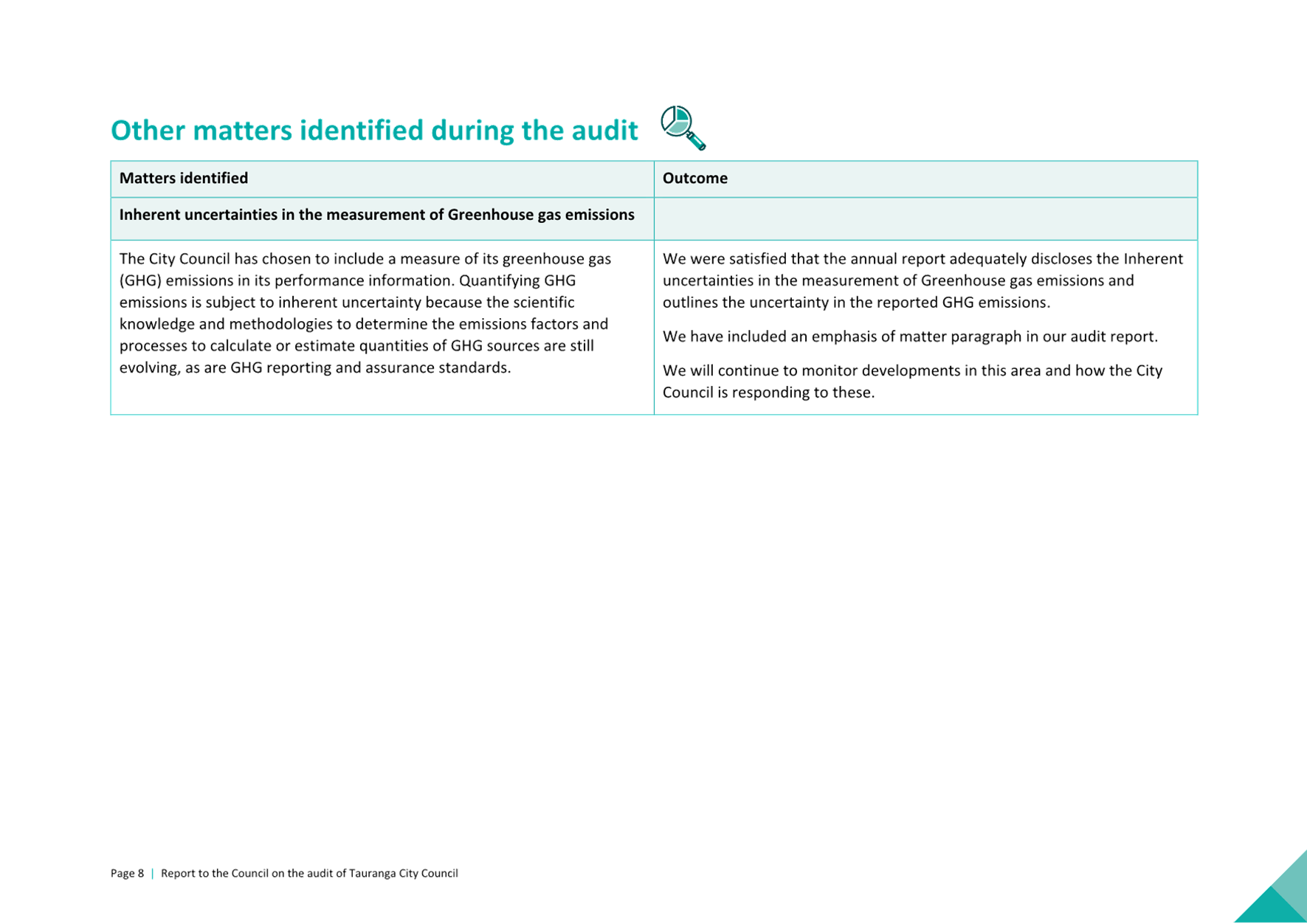

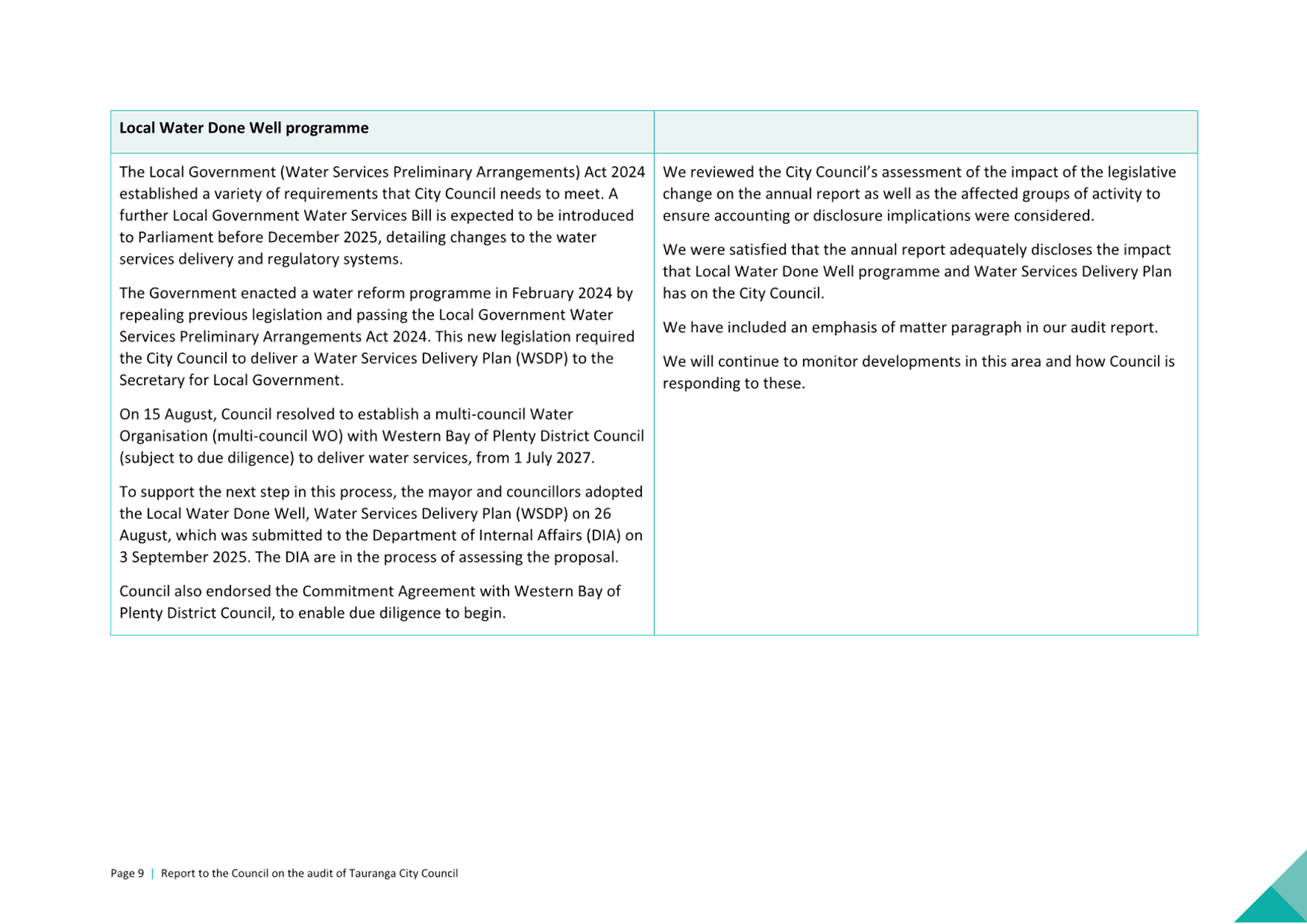

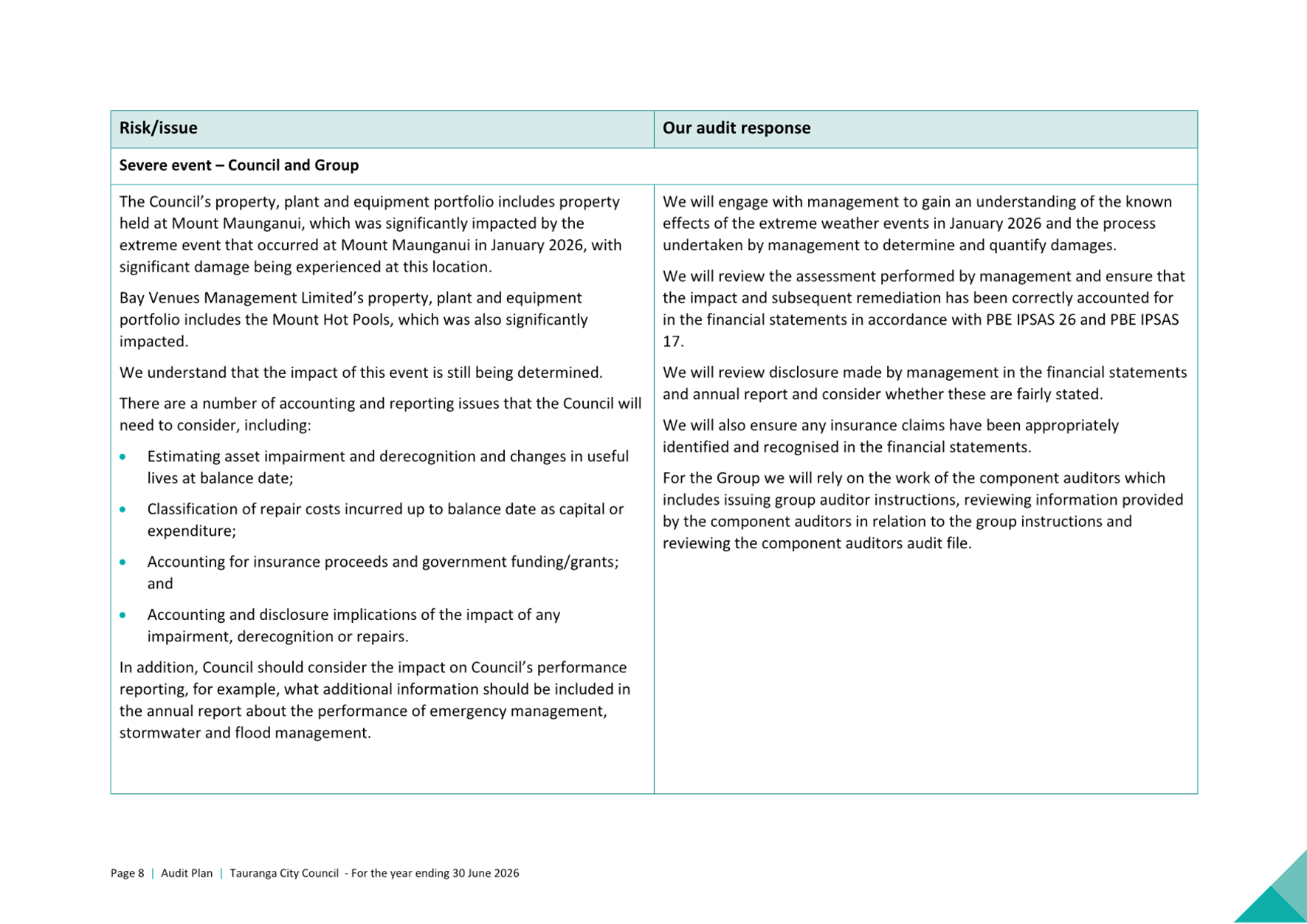

L1, 90 Devonport Road

Tauranga

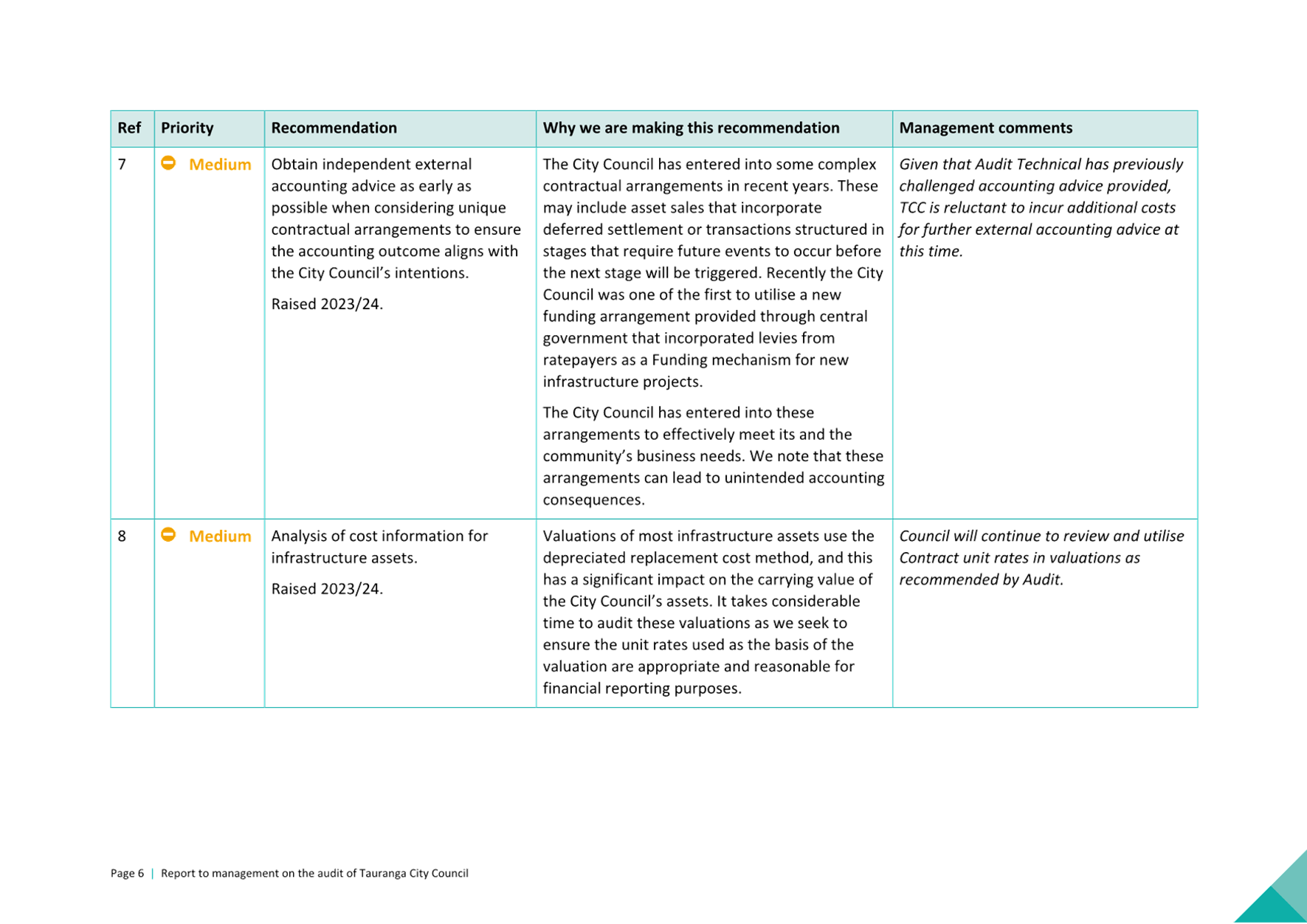

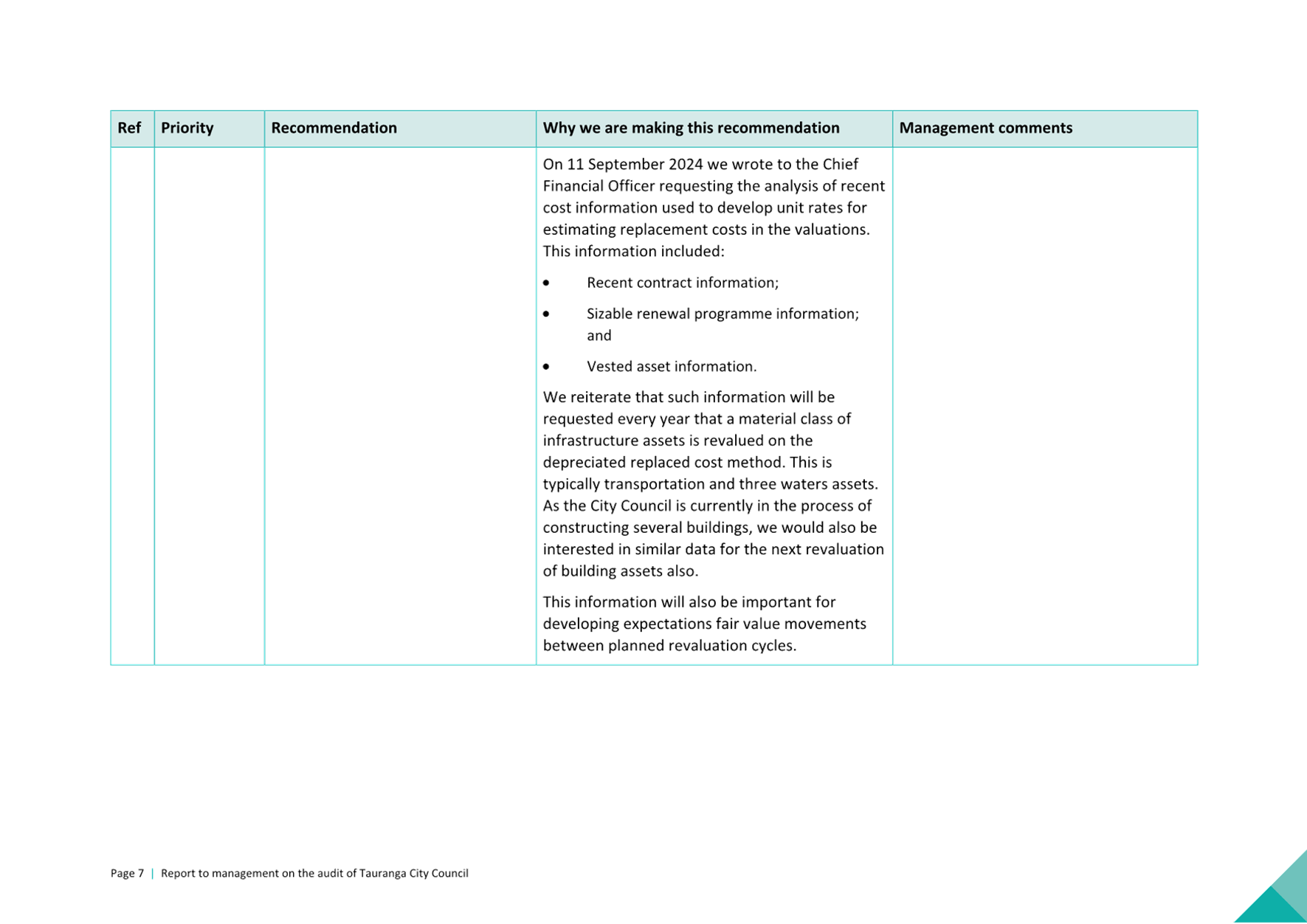

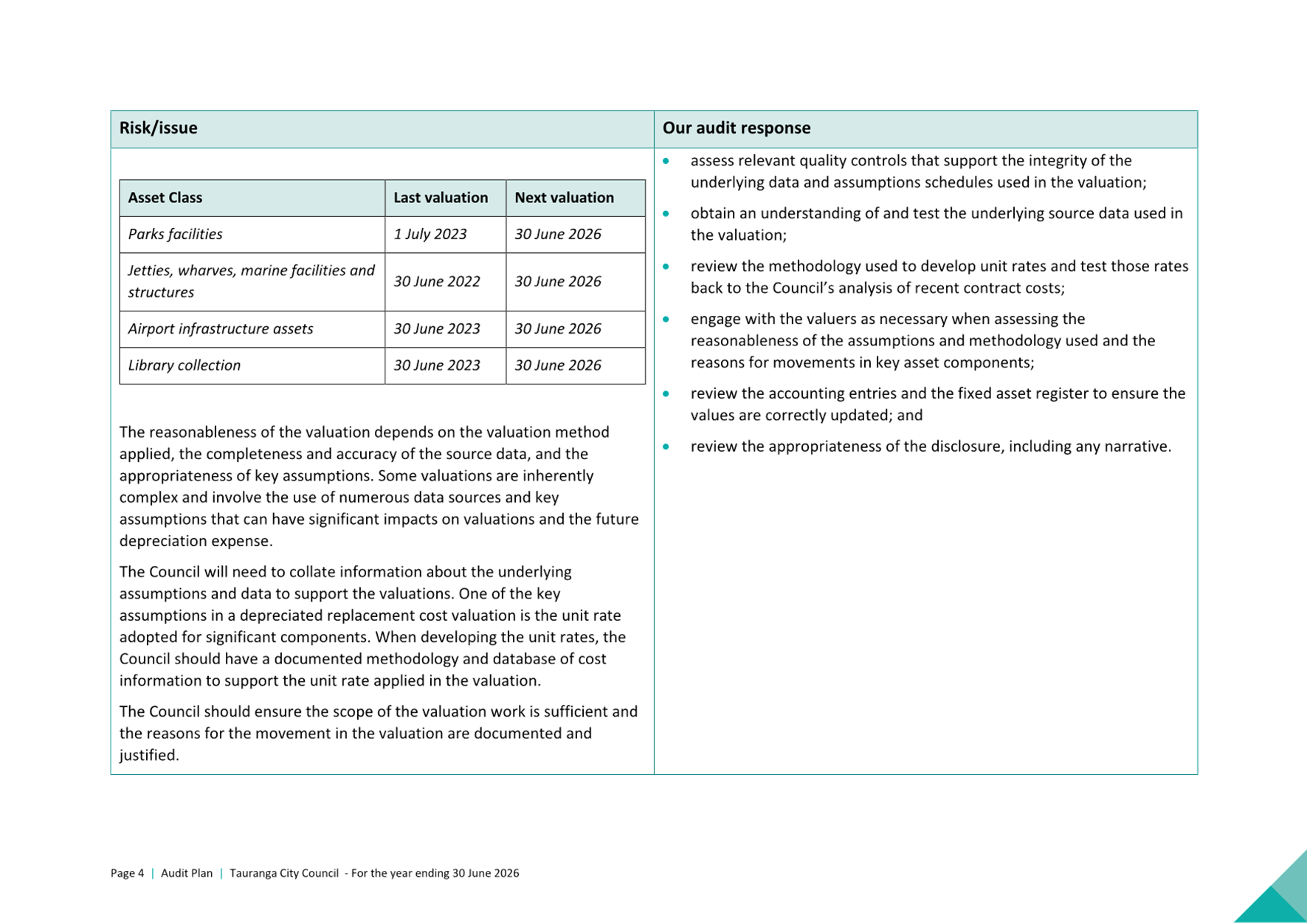

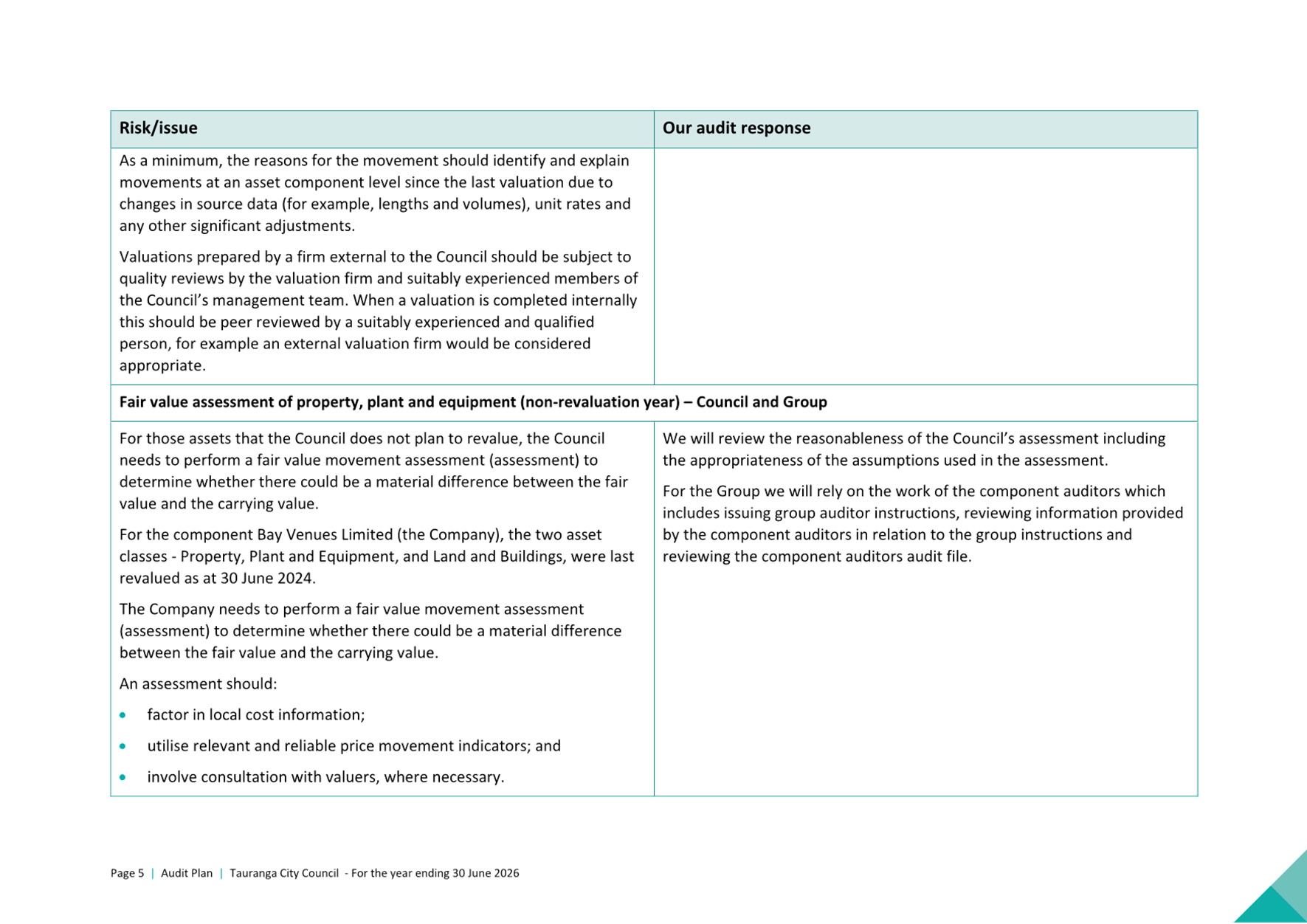

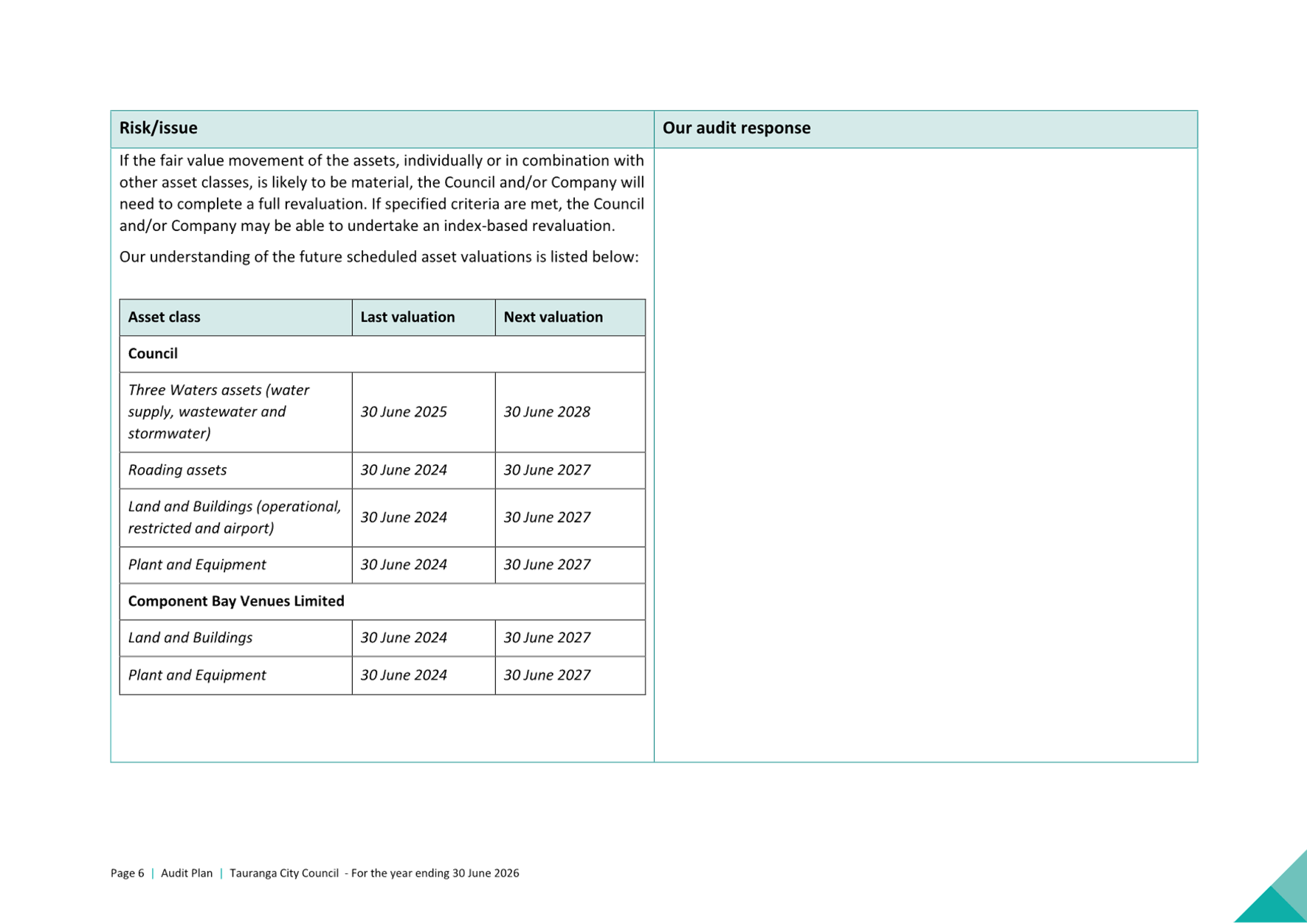

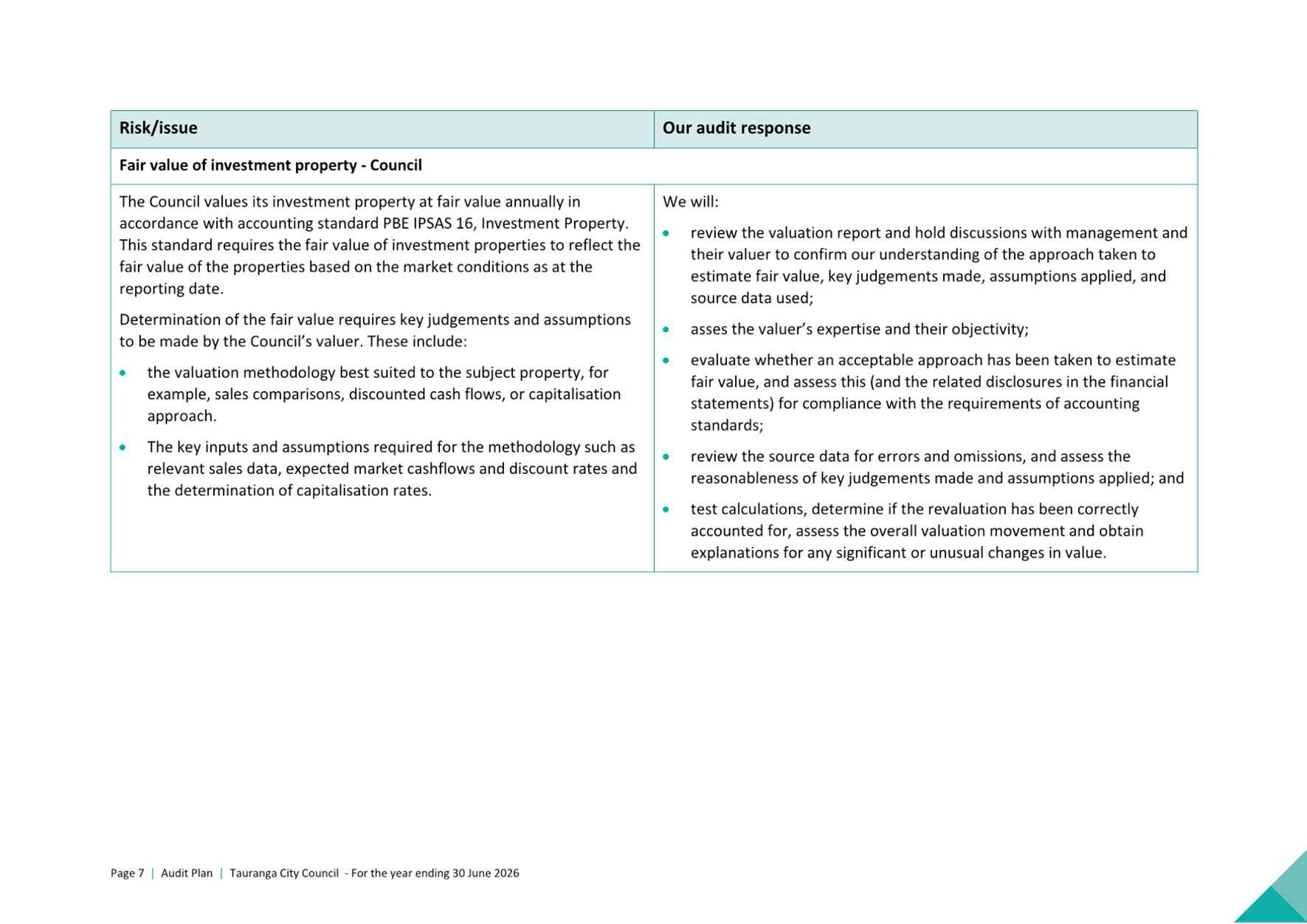

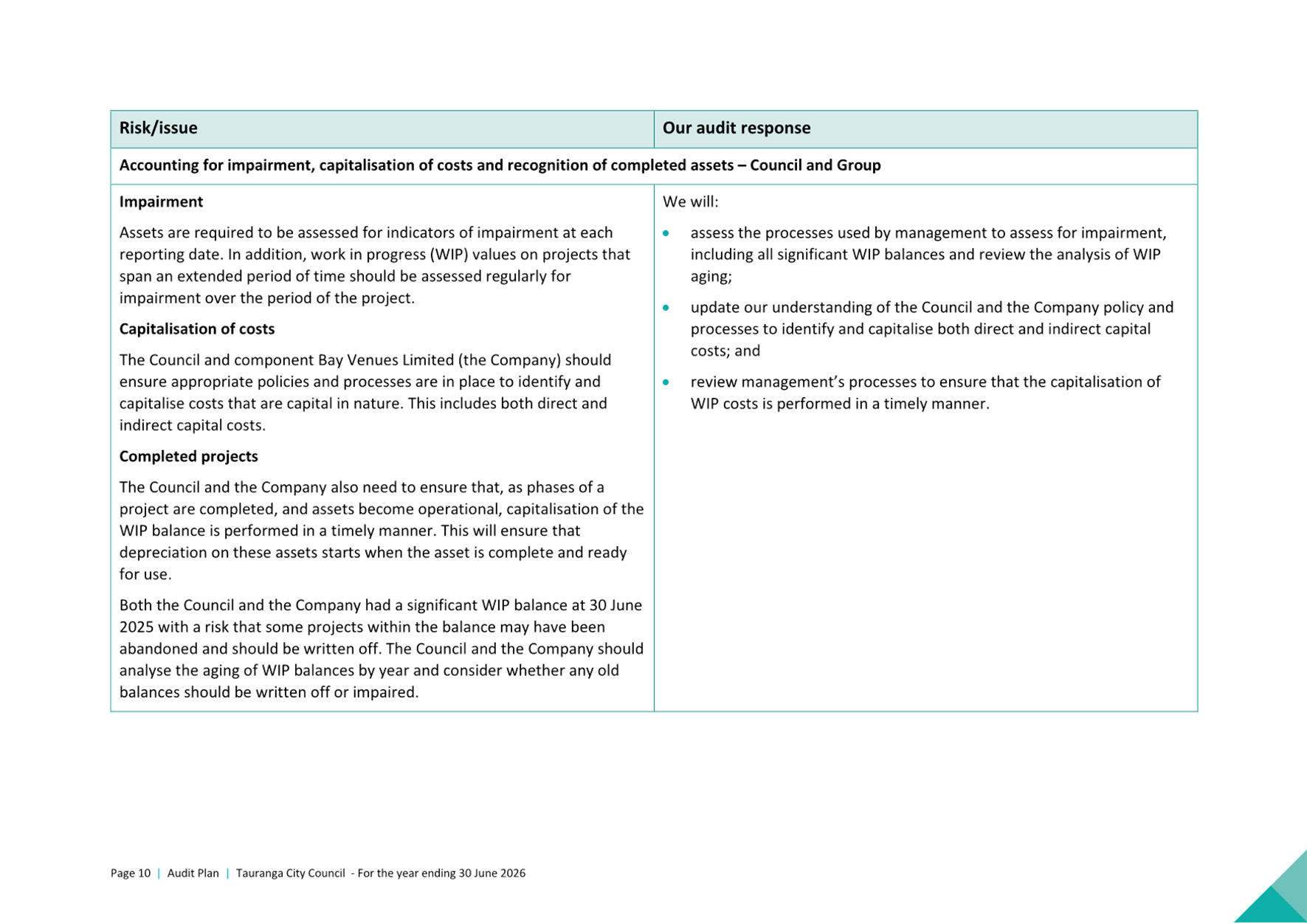

|

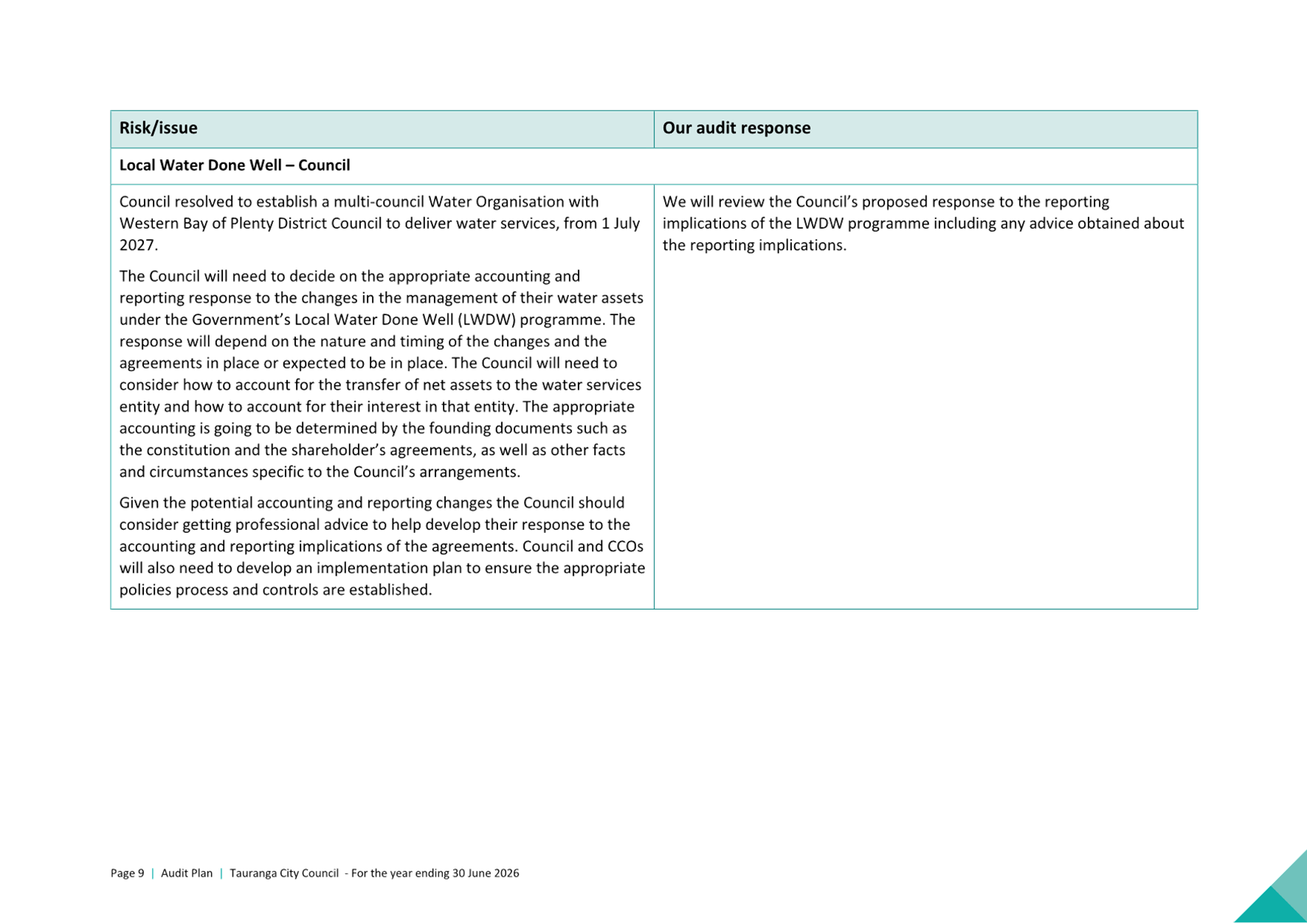

|

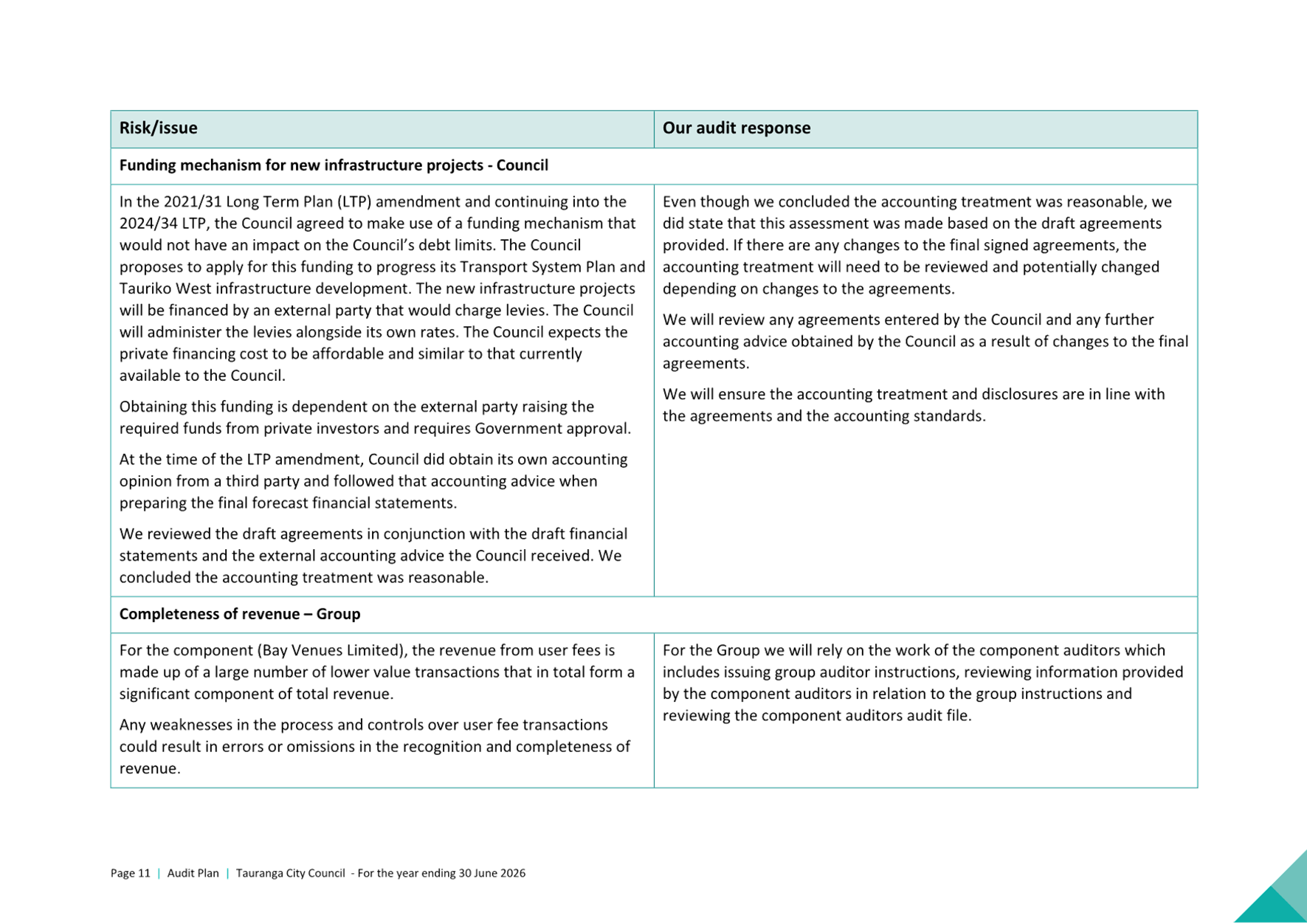

Please note that this

meeting will be livestreamed and the recording will be publicly available on

Tauranga City Council's website: www.tauranga.govt.nz.

|

|

Marty Grenfell

Chief Executive

|

Terms of reference – Audit & Risk Committee

Common

responsibility and delegations

The following common responsibilities and delegations apply

to all standing committees.

Responsibilities of standing committees

· Establish priorities and guidance on programmes relevant to the Role

and Scope of the committee.

· Provide guidance to staff on the development of investment options

to inform the Long Term Plan and Annual Plans.

· Report to Council on matters of strategic importance.

· Recommend to Council investment priorities and lead Council

considerations of relevant strategic and high significance decisions.

· Provide guidance to staff on levels of service relevant to the role

and scope of the committee.

· Establish and participate in relevant task forces and working

groups.

· Engage in dialogue with strategic partners, such as Smart Growth

partners, to ensure alignment of objectives and implementation of agreed

actions.

· Confirmation

of committee minutes.

Delegations to standing committees

· To make recommendations to Council outside of the delegated

responsibility as agreed by Council relevant to the role and scope of the

Committee.

· To make all decisions necessary to fulfil the role and scope of the

Committee subject to the delegations/limitations imposed.

· To develop and consider, receive submissions on and adopt

strategies, policies and plans relevant to the role and scope of the committee,

except where these may only be legally adopted by Council.

· To consider, consult on, hear and make determinations on relevant

strategies, policies and bylaws (including adoption of drafts), making

recommendations to Council on adoption, rescinding and modification, where

these must be legally adopted by Council.

· To approve relevant submissions to central government, its agencies

and other bodies beyond any specific delegation to any particular committee.

· Engage external parties as required.

Terms of reference – Audit & Risk Committee

Membership

|

Chair

|

Dame Kerry Prendergast

|

|

Deputy chair

|

Cr Steve Morris

|

|

Members

|

Deputy Mayor Jen Scoular

Mayor Mahé Drysdale (ex officio)

Rohario Murray - Tangata Whenua Representative

|

|

Non-voting members

|

(if any)

|

|

Quorum

|

Half of the members

present, where the number of members (including vacancies) is even;

and a majority of the members present, where the number of members

(including vacancies) is odd.

|

|

Meeting frequency

|

Quarterly

|

Role

The role of the Audit and Risk Committee is:

· To

assist and advise the Council in discharging its responsibility and ownership

of health and safety, risk management, internal control, and financial

management practices, frameworks and processes to ensure that these are robust

and appropriate to safeguard the Council’s staff and its financial and

non-financial assets.

Scope

· Oversee

Council’s relationship with the external auditor.

· Review

with the external auditor, before the audit commences, the areas of audit focus

and the audit plan.

· Review

with the external auditor, representations required by elected representatives

and senior management for the purposes of the audit.

· Receive

and review the external auditor’s report on the audit and

management’s responses to any issues raised.

· Make

any recommendations necessary to the Office of the Auditor-General regarding

the appointment or re-appointment of an external auditor.

· Review

and approve an annual internal audit plan, including the integration of that

plan with Council’s risk profile, and monitor the implementation of that

plan.

· Review

the reports of the internal audit function, in particular considering findings,

conclusions, and recommendations and management’s response to such.

Make any recommendations to Council on such as the Committee considers

appropriate.

· Review,

approve and monitor the implementation of Council’s Risk Management

Policy, including regular review of the corporate risk register.

· Review

reporting of new or emerging risks as needed.

· Review

the effectiveness of risk management and internal control systems including all

material financial, operational, compliance, and other managerial controls.

· Review

the effectiveness of health and safety policies and processes to ensure a

healthy and safe workplace for representatives, staff, contractors, visitors

and the public.

· Assist

elected representatives and the Chief Executive to discharge their statutory

roles as ‘officers’ in terms of the Health and Safety at Work Act

2015.

· Monitor

compliance with laws and regulations as appropriate.

· Review

and provide advice on policies relevant to the Committee’s role

including, but not limited to, policies addressing fraud, protected

disclosures, and conflicts of interest.

· Review

and monitor policy and processes to manage responsibilities under the Local

Government Official Information and Meetings Act 1987 and the Privacy Act 2020

and any actions from any Office of the Ombudsman's report.

· Review

and monitor current and potential litigation and other legal risks.

Power

to Act

· To

make all decisions necessary to fulfil the role, scope and responsibilities of

the Committee subject to the limitations imposed.

· To

establish sub-committees, working parties and forums as required.

Power

to Recommend

· To

Council and/or any standing committee as it deems appropriate.

|

Audit & Risk Committee meeting Agenda

|

23 February 2026

|

7 Confirmation

of minutes

7.1 Minutes

of the Audit & Risk Committee meeting held on 17 November 2025

File

Number: A19711978

Author: Anahera

Dinsdale, Governance Advisor

Authoriser: Sarah

Holmes, Team Leader: Governance & CCO Support Services

|

Recommendations

That the Minutes of the

Audit & Risk Committee meeting held on 17 November 2025 be confirmed as a

true and correct record.

|

Attachments

1. Minutes

of the Audit & Risk Committee meeting held on 17 November 2025

|

Error! No document variable supplied. minutesError! No document variable supplied. Error! No document variable supplied. minutesError! No document variable supplied.

|

Error! No

document variable supplied.

|

|

|

|

DRAFT MINUTES

Audit & Risk Committee meeting

Monday, 17 November 2025

|

Order of Business

1 Opening

karakia. 3

2 Apologies. 3

3 Public

forum.. 3

4 Acceptance

of late items. 3

5 Confidential

business to be transferred into the open. 3

6 Change

to order of business. 3

7 Confirmation

of minutes. 4

7.1 Minutes

of the Audit & Risk Committee meeting held on 21 July 2025. 4

8 Declaration

of conflicts of interest 4

9 Business. 4

9.1 Status

Update on actions from prior Audit & Risk Committee meetings. 4

9.2 Risk

Appetite Report - November 2025. 5

9.4 Policy

Review - Risk Management Policy. 6

9.3 Policy

Review - Conflicts of Interest Policy. 6

9.5 Policy

Review - Privacy Policy. 7

9.6 LGOIMA

and Privacy Q1 Report for 2025/26. 8

10 Discussion of late

items. 8

11 Public excluded

session. 8

11.1 Public

Excluded Minutes of the Audit & Risk Committee meeting held on 21 July 2025. 8

11.2 Digital/Cyber

Risk Quarterly Report 9

11.3 Risk

Register - Quarterly Update. 9

11.4 Internal

Audit & Assurance - Quarterly Update. 9

11.5 Health,

Safety and Wellbeing Quarterly Report: Q1 July to September 2025. 9

Confidential Attachment 2 9.1 - Status

Update on actions from prior Audit & Risk Committee meetings 9

Confidential Attachment 2 9.2 - Risk

Appetite Report - November 2025 9

Confidential Attachment 3 9.2 - Risk

Appetite Report - November 2025 10

12 Closing karakia. 10

MINUTES

OF Tauranga City Council

Audit & Risk Committee meeting

HELD

AT THE Tauranga City Council Chambers,

L1 Road, Tauranga

ON

Monday, 17 November 2025 AT 9.30am

|

MEMBERS PRESENT:

|

Deputy Mayor Jen Scoular, Cr

Steve Morris, Mayor Mahé Drysdale, Tangata Whenua Representative

Rohario Murray

|

|

ALSO PRESENT

|

Cr Glen Crowther, Cr Marten

Rozeboom, Cr Rod Taylor

|

|

IN ATTENDANCE:

|

Marty Grenfell (Chief

Executive),Kathryn Sharplin (Acting COFO), Anahera Dinsdale (Governance

Advisor), Caroline Irvin (Governance Advisor)

|

Timestamps are

included at the start of each item and signal where the agenda item can be

found in the recording of the meeting held on 17 November 2025 at Tauranga

City Council’s YouTube Channel.

1 Opening

karakia

Tangata Whenua Representative Rohario Murray opened the

meeting with a karakia.

2 Apologies

Nil

3 Public

forum

Nil

4 Acceptance

of late items

Nil

5 Confidential

business to be transferred into the open

Nil

6 Change

to order of business

The Chair advised that item 9.4 – Policy Review

– Risk Management Policy would be addressed before item 9.3 –

Policy Review – Conflicts of Interest Policy.

7 Confirmation

of minutes

Timestamp: 6 minutes

|

7.1 Minutes of

the Audit & Risk Committee meeting held on 21 July 2025

|

|

Committee Resolution AR/25/4/1

Moved: Tangata

Whenua Representative Rohario Murray

Seconded: Deputy Mayor Jen Scoular

That the Minutes

of the Audit & Risk Committee meeting held on 21 July 2025 be confirmed

as a true and correct record subject to the following corrections:

(a)

Members Present section of

minutes – Correct Cr Marten Rozeboom spelling of name.

Carried

|

8 Declaration

of conflicts of interest

Nil

9 Business

Timestamp: 8 minutes

|

9.1 Status

Update on actions from prior Audit & Risk Committee meetings

|

|

Staff Kathryn

Sharplin, Acting COFO

|

|

Committee Resolution AR/25/4/2

Moved: Deputy

Mayor Jen Scoular

Seconded: Tangata Whenua Representative Rohario

Murray

That the Audit & Risk Committee:

(a) Receives the report

"Status Update on actions from prior Audit & Risk Committee

meetings".

(b) Attachment 2 can be

transferred into the open can be released when the full report is reviewed

Carried

|

Timestamp: 13 minutes

|

9.2 Risk

Appetite Report - November 2025

|

|

Staff Chris

Quest, Manager Risk & Assurance

Chris

Smith, Risk and Business Continuity Advisor

Resolution Note:

·

Resolution (b) should reference Attachment 1 not Attachment 2.

This was corrected at the meeting.

|

|

Committee Recommendation

Moved: Mayor

Mahé Drysdale

Seconded: Cr Steve Morris

That the Audit & Risk Committee:

(a) Receives the report

"Risk Appetite Report - November 2025".

(b) Endorses the risk appetite

statements as outlined in Attachment 1 of this report.

(c) Commences a 12-month

reporting cycle of Tauranga City Council’s risk against the preliminary

risk appetite statements to further define tolerance levels and consequences.

(d) Attachment 2 to remain

in public excluded permanently.

(e) Attachment 3 to remain

in public excluded permanently.

An amendment was proposed:

Moved: Tangata

Whenua Representative Ms Rohario Murray

Seconded: Deputy Mayor Jen

Scoular

(f) That

the Environmental risk be moved from moderate to low risk appetite

For: Deputy

Mayor Jen Scoular, Cr Steve Morris and Tangata Whenua Representative Rohario

Murray

Against: Cr

Mahé Drysdale

carried 3/1

|

|

Committee Resolution AR/25/4/3

Moved: Mayor

Mahé Drysdale

Seconded: Cr Steve Morris

That the Audit & Risk Committee:

(a) Receives the report

"Risk Appetite Report - November 2025".

(b) Endorses the risk appetite

statements as outlined in Attachment 1 of this report.

(c) Commences a 12-month

reporting cycle of Tauranga City Council’s risk against the preliminary

risk appetite statements to further define tolerance levels and consequences.

(d) Attachment 2 to remain

in public excluded permanently.

(e) Attachment 3 to remain

in public excluded permanently.

(f) That the Environmental

risk be moved from moderate to low risk appetite

Carried

|

Timestamp: 51 minutes

|

9.4 Policy

Review - Risk Management Policy

|

|

Staff Chris

Quest, Manager Risk & Assurance

Chris

Smith, Risk and Business Continuity Advisor

Sharon

Herbst, Policy Analyst

Actions

·

That staff create a glossary of terms, in particular with how

it refers to all associated with TCC and the groupings there of.

|

|

Committee Resolution AR/25/4/4

Moved: Cr

Steve Morris

Seconded: Deputy Mayor Jen Scoular

That the Audit & Risk Committee:

(a) Receives the report

"Policy Review - Risk Management Policy".

(b) Approves and adopts the

revised Risk Management Policy incorporating changes provided in the report

for the policy to take effect immediately, including:

(i) updating the

definitions of the terms Business Continuity, Council, Tauranga City Council,

the Committee, council staff, risk, Enterprise Risk Management System (ERMS),

group and division

(ii) including Te Ao

Māori principles in the principles section of the policy in alignment

with Tauranga City Council’s Code of Conduct/ Ngā Kawa Arataki

(iii) updating the

responsibilities in the policy for Council, the Committee and the Chief

Executive

(iv) changing the frequency of the

review of risk registers from quarterly by department to regularly by each

division

(v) including a description of

strategic risks and how they are recorded.

(c) Delegates to the Acting Chief

Operating and Financial Officer - Commercial and General Counsel to make any

necessary minor drafting or presentation changes to the Risk Management

Policy prior to it being published.

Carried

|

Timestamp: 1 hour

|

9.3 Policy

Review - Conflicts of Interest Policy

|

|

Staff Chris

Quest, Manager Risk & Assurance

Chris

Smith, Risk and Business Continuity Advisor

Sharon

Herbst, Policy Analyst

|

|

Committee Resolution AR/25/4/5

Moved: Cr

Steve Morris

Seconded: Tangata Whenua Representative Rohario

Murray

That the Audit & Risk Committee:

(a) Receives the report

"Policy Review - Conflicts of Interest Policy".

(b) Endorses the updated policy (Attachment

One).

Carried

|

Timestamp: 1 hour and 12 minutes

|

9.5 Policy

Review - Privacy Policy

|

|

Staff Andrew

Hough, General Counsel

Sharon

Powell, Privacy Officer

Sharon

Herbst, Policy Analyst

|

|

Committee Resolution AR/25/4/6

Moved: Mayor

Mahé Drysdale

Seconded: Deputy Mayor Jen Scoular

That the Audit & Risk Committee:

(a) Receives the report

"Policy Review - Privacy Policy".

(b) Endorses the creation of a

new Privacy Policy (Attachment One) for the Executive to consider and

adopt, which includes:

(i) a scope that includes

all council workers, including the mayor, councillors and persons appointed

to council committees

(ii) applying the Information

Privacy Principles (IPPs) and ensuring appropriate systems are in place to

manage personal information

(iii) a commitment to enhancing

culturally aligned practices

(iv) an annually reviewed privacy

statement on the council website

(v) clear roles and

responsibilities for privacy officers

(vi) annual privacy training for

workers

(vii) effective management of privacy

breaches.

Carried

|

Timestamp: 1 hour 17 minutes

|

9.6 LGOIMA and

Privacy Q1 Report for 2025/26

|

|

Staff Kathryn

Norris, Team Leader: Information Requests

|

|

Committee Resolution AR/25/4/7

Moved: Mayor

Mahé Drysdale

Seconded: Deputy Mayor Jen Scoular

That the Audit & Risk Committee:

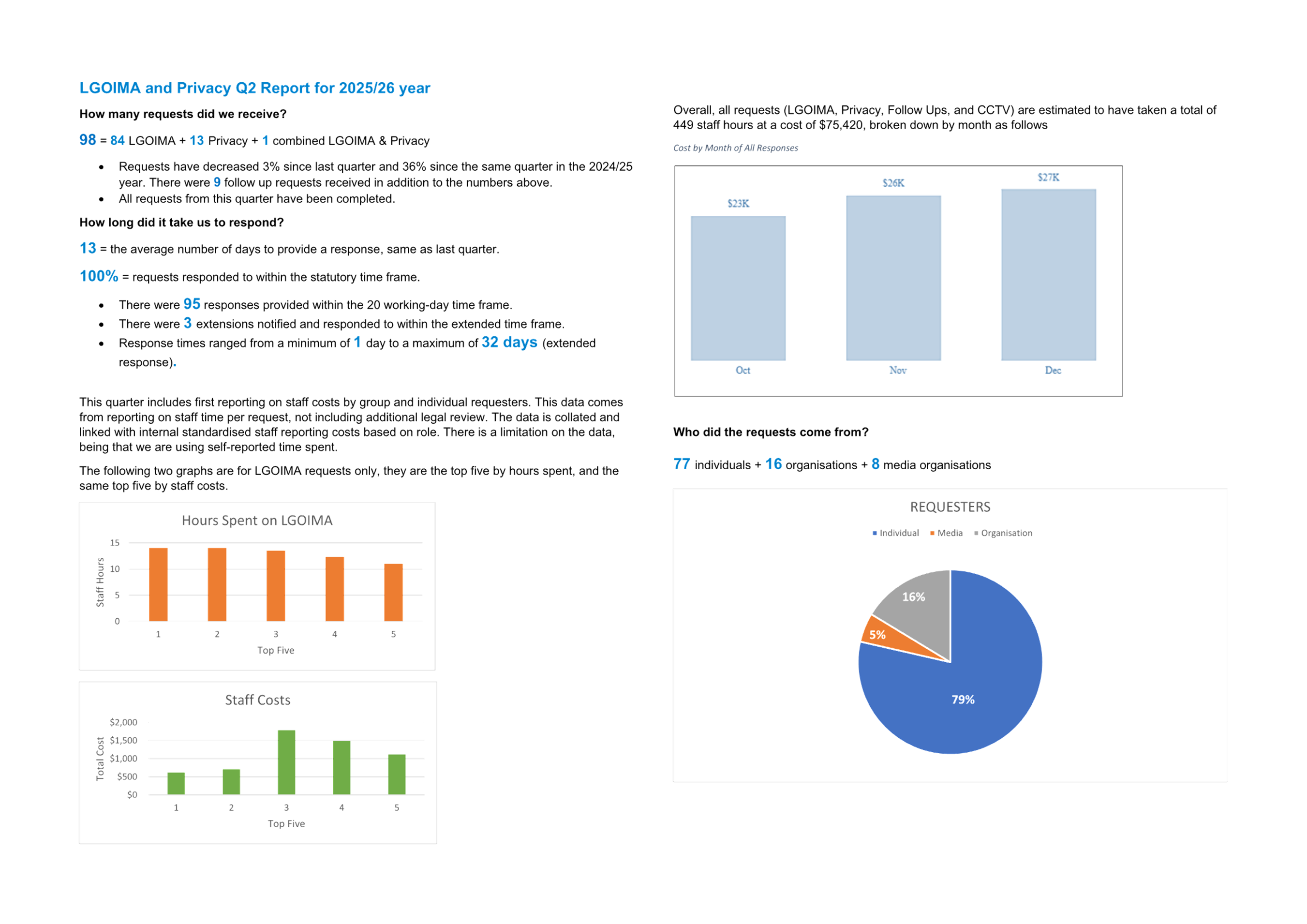

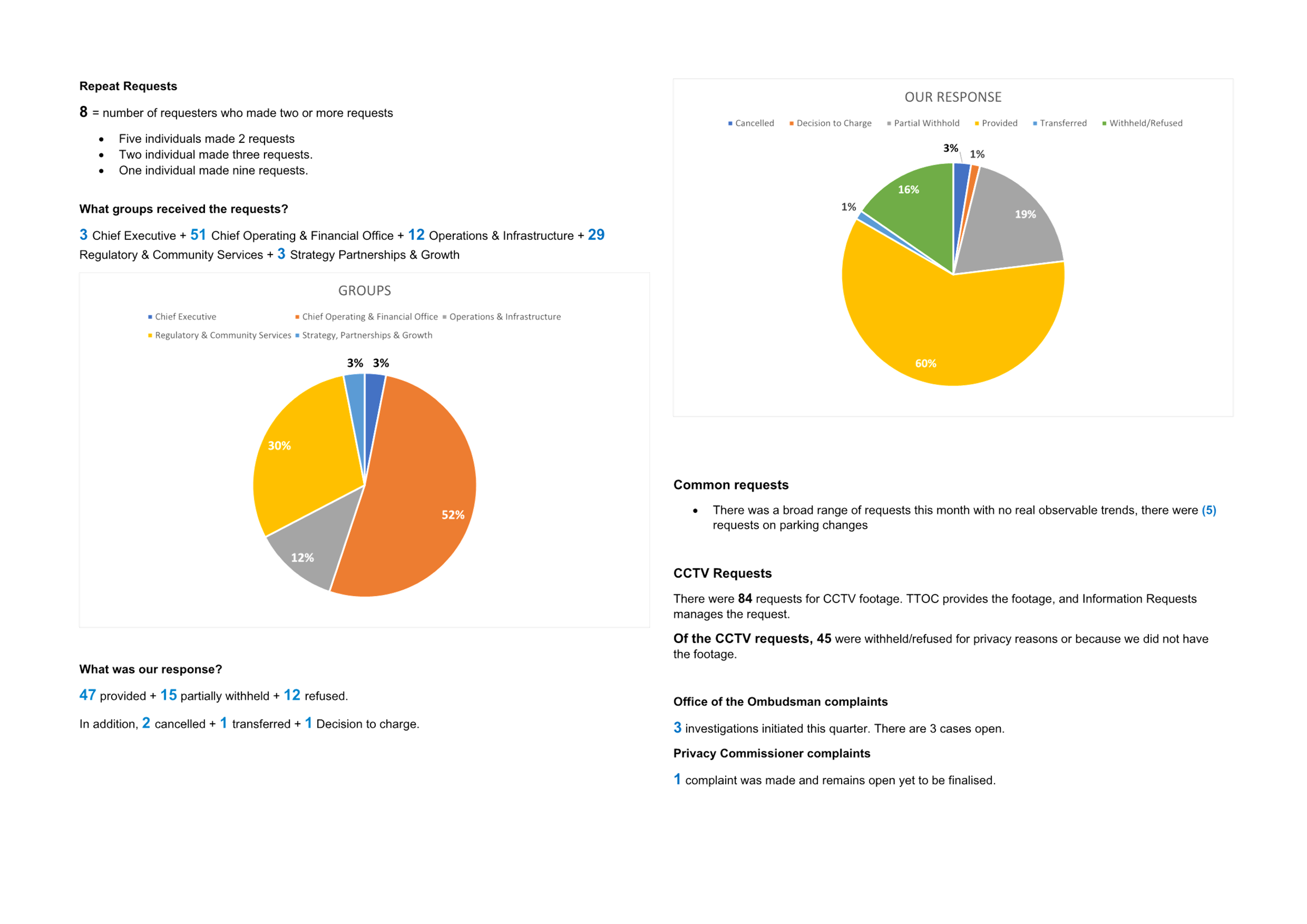

(a) Receives the report " LGOIMA and Privacy Q1 Report for 2025/26".

Carried

|

10 Discussion

of late items

Nil

11 Public

excluded session

Resolution to exclude the public

|

Committee Resolution AR/25/4/8

Moved: Deputy

Mayor Jen Scoular

Seconded: Tangata Whenua Representative Rohario

Murray

That the public be excluded from the following parts of

the proceedings of this meeting.

The general subject matter of each matter to be considered

while the public is excluded, the reason for passing this resolution in

relation to each matter, and the specific grounds under section 48 of the

Local Government Official Information and Meetings Act 1987 for the passing

of this resolution are as follows:

|

General

subject of each matter to be considered

|

Reason for

passing this resolution in relation to each matter

|

Ground(s)

under section 48 for the passing of this resolution

|

|

11.1 -

Public Excluded Minutes of the Audit & Risk Committee meeting held on

21 July 2025

|

s7(2)(a) - The

withholding of the information is necessary to protect the privacy of

natural persons, including that of deceased natural persons

s7(2)(b)(i) - The

withholding of the information is necessary to protect information where

the making available of the information would disclose a trade secret

s7(2)(g) - The

withholding of the information is necessary to maintain legal professional

privilege

s7(2)(h) - The

withholding of the information is necessary to enable Council to carry out,

without prejudice or disadvantage, commercial activities

s7(2)(i) - The

withholding of the information is necessary to enable Council to carry on,

without prejudice or disadvantage, negotiations (including commercial and

industrial negotiations)

s7(2)(j) - The

withholding of the information is necessary to prevent the disclosure or

use of official information for improper gain or improper advantage

|

s48(1)(a) - the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

11.2 -

Digital/Cyber Risk Quarterly Report

|

s7(2)(a) - The

withholding of the information is necessary to protect the privacy of

natural persons, including that of deceased natural persons

s7(2)(b)(i) - The

withholding of the information is necessary to protect information where

the making available of the information would disclose a trade secret

|

s48(1)(a) - the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

11.3 -

Risk Register - Quarterly Update

|

s7(2)(j) - The

withholding of the information is necessary to prevent the disclosure or

use of official information for improper gain or improper advantage

|

s48(1)(a) - the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

11.4 -

Internal Audit & Assurance - Quarterly Update

|

s7(2)(j) - The

withholding of the information is necessary to prevent the disclosure or

use of official information for improper gain or improper advantage

|

s48(1)(a) - the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

11.5 -

Health, Safety and Wellbeing Quarterly Report: Q1 July to September 2025

|

s7(2)(a) - The

withholding of the information is necessary to protect the privacy of

natural persons, including that of deceased natural persons

|

s48(1)(a) - the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

Confidential

Attachment 2 - 9.1 - Status Update on actions from prior Audit & Risk

Committee meetings

|

s7(2)(j) - The

withholding of the information is necessary to prevent the disclosure or

use of official information for improper gain or improper advantage

|

s48(1)(a) the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

Confidential

Attachment 2 - 9.2 - Risk Appetite Report - November 2025

|

s7(2)(j) - The

withholding of the information is necessary to prevent the disclosure or

use of official information for improper gain or improper advantage

|

s48(1)(a) the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

Confidential

Attachment 3 - 9.2 - Risk Appetite Report - November 2025

|

s7(2)(c)(i) - The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information, or information from the same source, and it

is in the public interest that such information should continue to be

supplied

|

s48(1)(a) the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

Carried

|

12 Closing

karakia

Cr Steve Morris closed the meeting with a karakia.

The meeting closed at 11:28am.

The minutes of this meeting were confirmed as a true and

correct record at the Audit & Risk Committee meeting held on 23 February

2026.

|

Audit & Risk Committee meeting Agenda

|

23 February 2026

|

8 Declaration

of conflicts of interest

|

Audit & Risk Committee meeting Agenda

|

23 February 2026

|

9 Business

9.1 Results

of 2024/25 Audit by Audit New Zealand

File

Number: A19471414

Author: Marin

Gabric, Team Leader - Financial Accounting and Compliance

Sheree Covell,

Manager: Treasury & Financial Processes

Authoriser: Craig

Rice, Chief Operating and Financial Officer

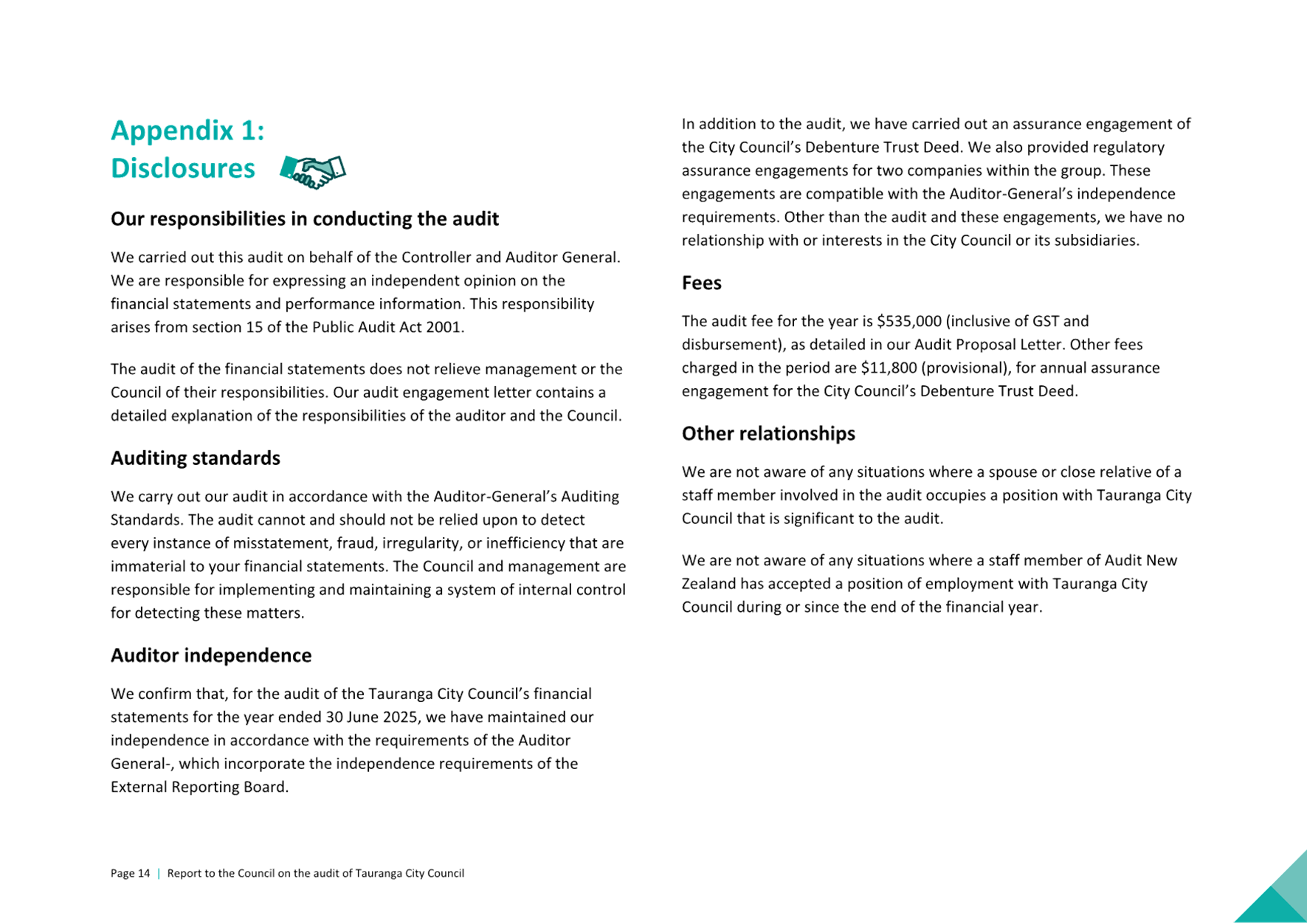

Purpose of the Report

1. The purpose of this report is to present

Audit New Zealand’s (Audit NZ) findings from the audit of Tauranga City

Council for the year ended 30 June 2025. The two Audit NZ reports outline the

results of the annual audit and highlight the areas where Council is performing

well and those where improvements are recommended.

|

Recommendations

That the Audit &

Risk Committee:

(a) Receives the report

"Results of 2024/25 Audit by Audit New Zealand".

(b) Notes

the recommendations from Audit NZ contained within the report to Council.

|

Executive Summary

2. This

report presents Audit New Zealand’s (Audit NZ) findings from the audit on

TCC for the year ended 30 June 2025. The two Audit NZ reports outline the

results of the annual audit, highlighting areas where Council is performing

well and areas where improvements are recommended. While no significant risks

require the Committee’s attention, all new matters identified during the audit are summarised in the

background section of this report.

3. While this is a

report on the Audit of 2024/25 financial year, additional information has been

added for your consideration. The background section of this report highlights

matters that will likely have an impact on the 2025/26 Audit and Annual Report.

The attached 2025/26 Audit NZ audit Plan confirms that these matters that will

require specific audit focus.

Background

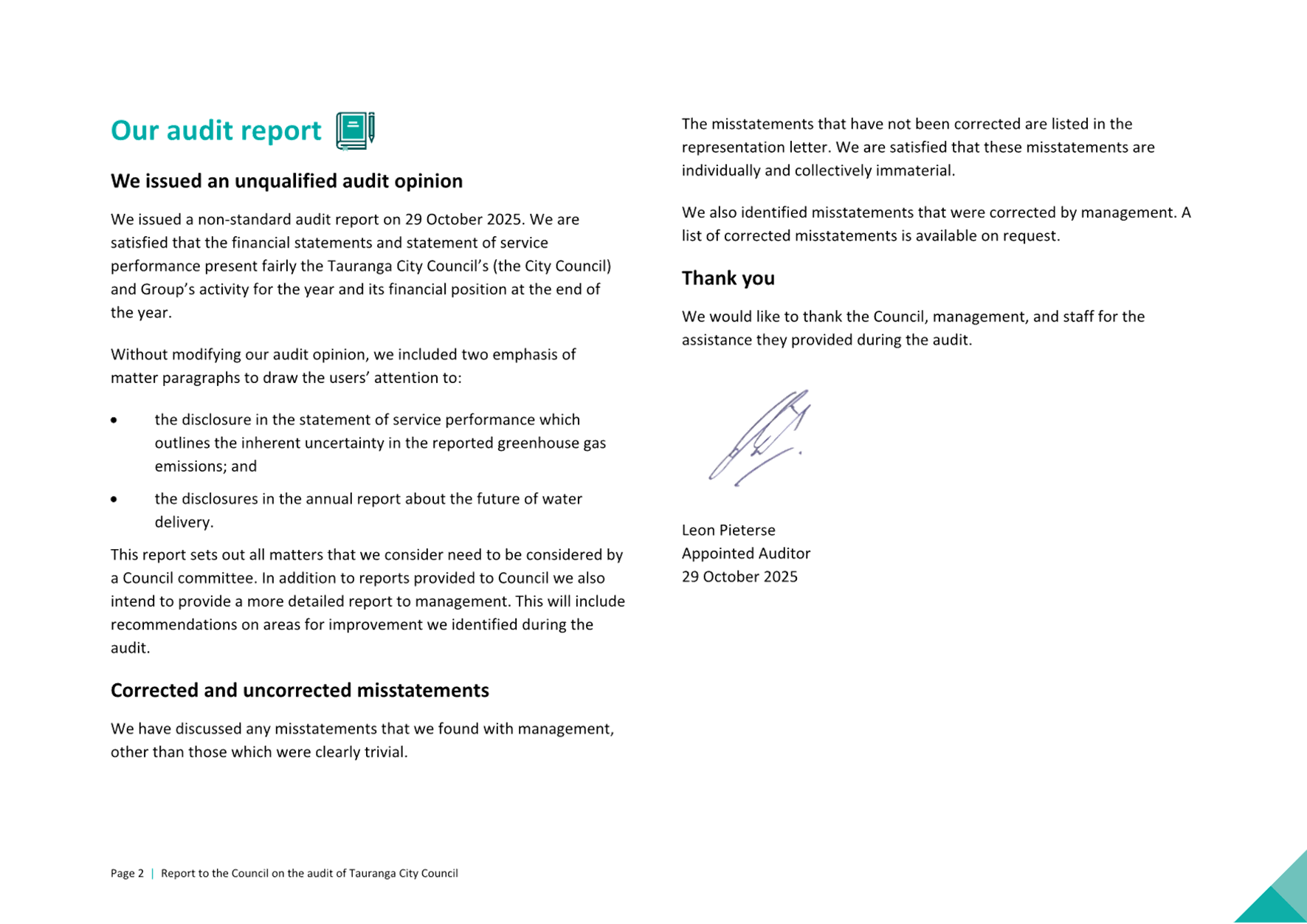

4. Audit New Zealand has completed its audit

of TCC for the year ended 30 June 2025. An unmodified opinion was given for the

adoption of the 2025 Annual Report on 29 October 2025.

5. The audit report outlines matters

identified during the audit, makes recommendations and includes Council

comments on these recommendations. An update on matters identified during the

previous audit is also provided.

6. Audit NZ provides recommendations for

improvement and prioritises these as urgent, necessary, or beneficial. The

report also reviews earlier recommendations and notes whether these have been

addressed by Council.

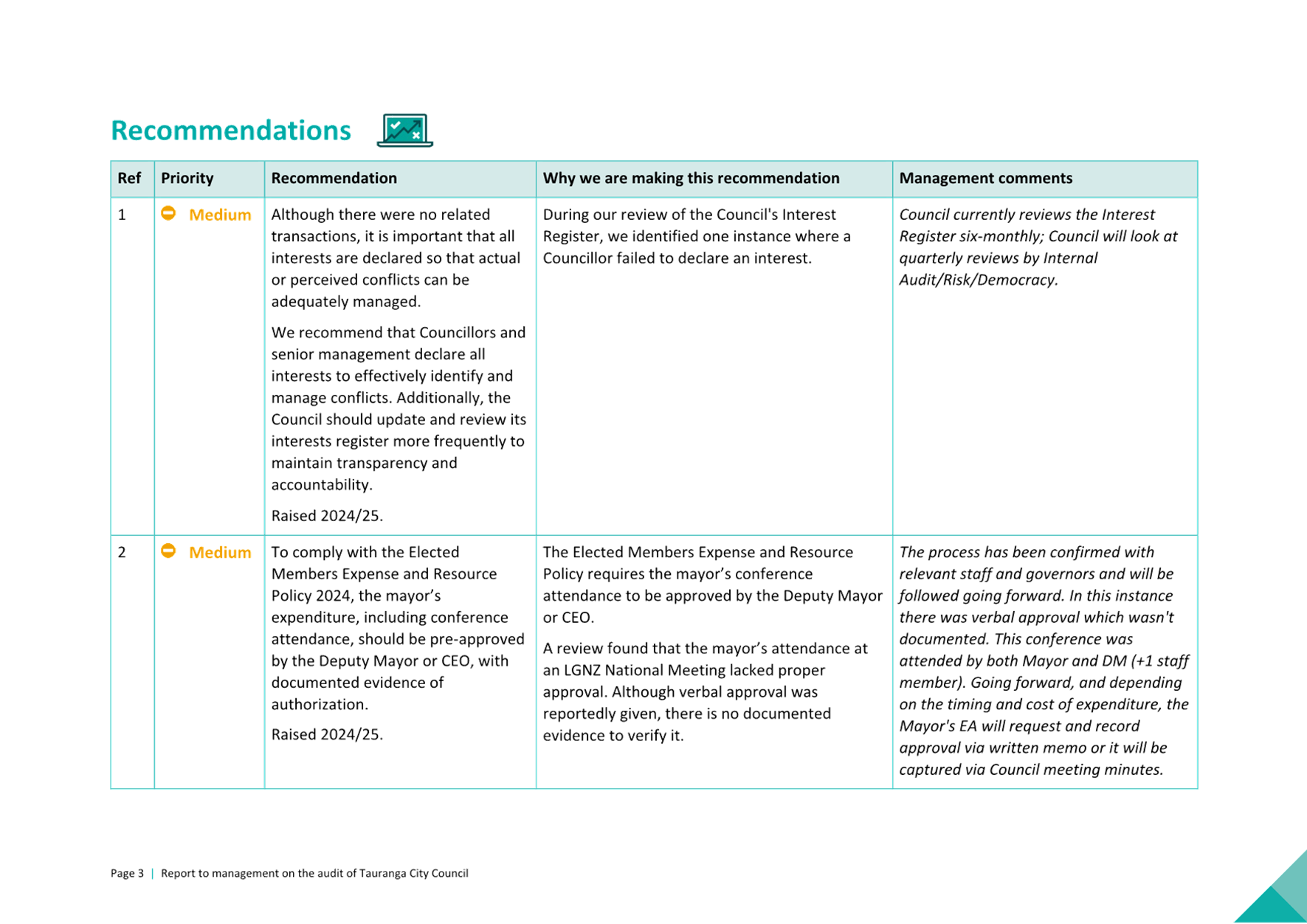

7. There were six new recommendations made by

audit, five of which are deemed medium risk and one low. These recommendations

are detailed below.

8. New Recommendation #1: One

Councillor failed to declare an interest in Council’s Conflict of

Interest Register.

9. During NZ Audit’s review of the

Council's Interest Register, NZ Audit identified one instance where a

Councillor failed to declare an interest. Council currently reviews the

Interest Register six-monthly; Council will now undertake quarterly reviews by

Internal Audit/Risk/Democracy.

10. New Recommendation #2:

The Mayor’s expenditure was not approved in one instance.

11. The Elected Members’ Expense

and Resource Policy require all the Mayor’s expenditure to be approved by

the Deputy Mayor or CEO.

12. The process has been confirmed with

relevant staff and governors and will be followed going forward. In this

instance there was verbal approval, which was not documented.

13. New Recommendation #3: Capitalisation

should occur in the correct accounting period to

support accurate financial reporting and depreciation

calculations.

14. A vehicle asset was recorded

in July 2024, but the documentation was dated June 2024. Value

was $61k. High level checks were done on material WIP balances and

adjusted accordingly. This instance was not considered material by Council

staff.

15. New Recommendation

#4: A Journal for fuel allocation was not authorised.

16. This has been raised with the team

concerned and the process of authorising journals has been noted.

17. New Recommendation #5: Two

of Council CCOs did not meet their statutory deadline to be audited.

18. After multiple requests from Council

staff to the Office of the Auditor General, and the team at Audit NZ, an

auditor was appointed for Te Manawataki o Te Papa Limited and

Te Manawataki o Te Papa Charitable Trust. The statutory accounts were

audited post adoption. Going forward this will not be an issue. The

finance team work closely with the CCOs and note the Annual Reports

are being prepared in a timely manner but the market for auditors

still remains constrained and beyond the control of Council.

19. New Recommendation #6: City

Operations have no Delegated Financial Approval for work conducted by City Care

Ltd.

20. There is an existing agreement in

place between Tauranga City Council and City Care Ltd (CCL) whereby maintenance

requests are issued by Council to CCL. When the work has been completed, CCL

notifies Council and provides a summary of the work performed, together with

costings and photos as evidence of the work performed. The workflow is then

closed off by Council staff (Senior Infrastructure Information Specialist).

Currently the Senior Infrastructure Information Specialist does not have a

Delegated Financial Authority, and no financial approval takes place for City

Operations’ work orders.

21. Prior Year Recommendations

22. There are nine recommendations from

prior years, all of which continue to be monitored and worked on. The

detail and Council staff comments are on pages 6-11 of the Audit Management

Report. Staff continue to work on solutions for these recommendations but

consider them to be of low risk to the organisation.

23. Matters for Considerations for

2025/26 Audit & Annual Report:

24. While the impacts are not fully

known, the following matters will likely be of concern to Audit NZ during the

preparation of the Audit and Annual Report.

25. The recent Mauao weather event will

incur unbudgeted costs, which will go through a cost recovery process and

create potential accounting considerations for Audit NZ to review as part of

the 2025/26 Audit.

26. Mauao landslides will include

significant write downs of the holiday park assets and Mount Hot Pools within

Bay Venues Ltd accounts for the 2025/26 financial year. There will also be

impacts for budgeted revenue and expenses for the remainder of the 2025/26

financial year for both of these venues. The effects of this event have

unidentified costs that will also affect the remainder of Council’s

Annual Financial Statements.

27. Revaluations of major infrastructure

assets occur on a three-year cycle. In the 2025/26 financial year the items to

revalue include Spaces & Places Assets (parks & reserves), Airport

Infrastructure and Marine Assets.

Impacts

of the revaluations will be presented in the first draft of the 2025/26 Annual

Report, which will be presented at the September 2026 City Delivery Committee

meeting.

28. The

Local Water Done Well (LWDW) potential transfer to the new entity in 2027, will

not have a significant impact on Council’s Annual Report for the 2025/26

financial year. The expectation is that for the 2026/27 financial year, there

will be a significant focus and impact on the Annual Report. This is dependent

on decisions regarding structure, ownership and guarantees, which will be decided by Council.

29. The

attached 2025/26 audit plan from Audit NZ confirms that these matters will

require specific focus during the annual audit. Outside of these matters

the focus continues to be the value and capitalisation of assets as well as the

accounting treatment of significant financial transactions.

Statutory Context

30. The audit report is part of the

process of financial accounting and reporting set out under the Local

Government Act 2002.

Options Analysis

31. There are no options presented in this report.

Financial Considerations

32. Audit NZ have indicated there will

be some cost overruns from the Audit. These have not been quantified at the

time of preparing this document.

Legal Implications / Risks

33. There are no specific legal

implications or risks directly as a result of this report.

Consultation / Engagement

34. No further consultation or

engagement is required in relation to this document.

Significance

35. The Local Government Act 2002

requires an assessment of the significance of matters, issues, proposals and

decisions in this report against Council’s Significance and Engagement

Policy. Council acknowledges that in some instances a matter, issue, proposal

or decision may have a high degree of importance to individuals, groups, or

agencies affected by the report.

36. This assessment considers the impact and potential consequences for:

(a) the current

and future social, economic, environmental, or cultural well-being of the

district or region

(b) any persons who are likely to be

particularly affected by, or interested in, the decision.

(c) the capacity of the local authority

to perform its role, and the financial and other costs of doing so.

37. In accordance with the

considerations above, criteria and thresholds in the policy, it is considered that

the matter is of low significance.

ENGAGEMENT

38. Taking into consideration the above

assessment, that the matter is of low significance, staff are of the opinion

that no further engagement is required prior to Council making a decision. Click

here to view the TCC

Significance and Engagement Policy

Next Steps

39. Council will continue to work

through Audit NZ’s recommendations for improvement in our processes and

reporting.

40. The impacts of LWDW and the Mauao

weather event and asset revaluations will be presented in the 2025/26 Annual

Report.

Attachments

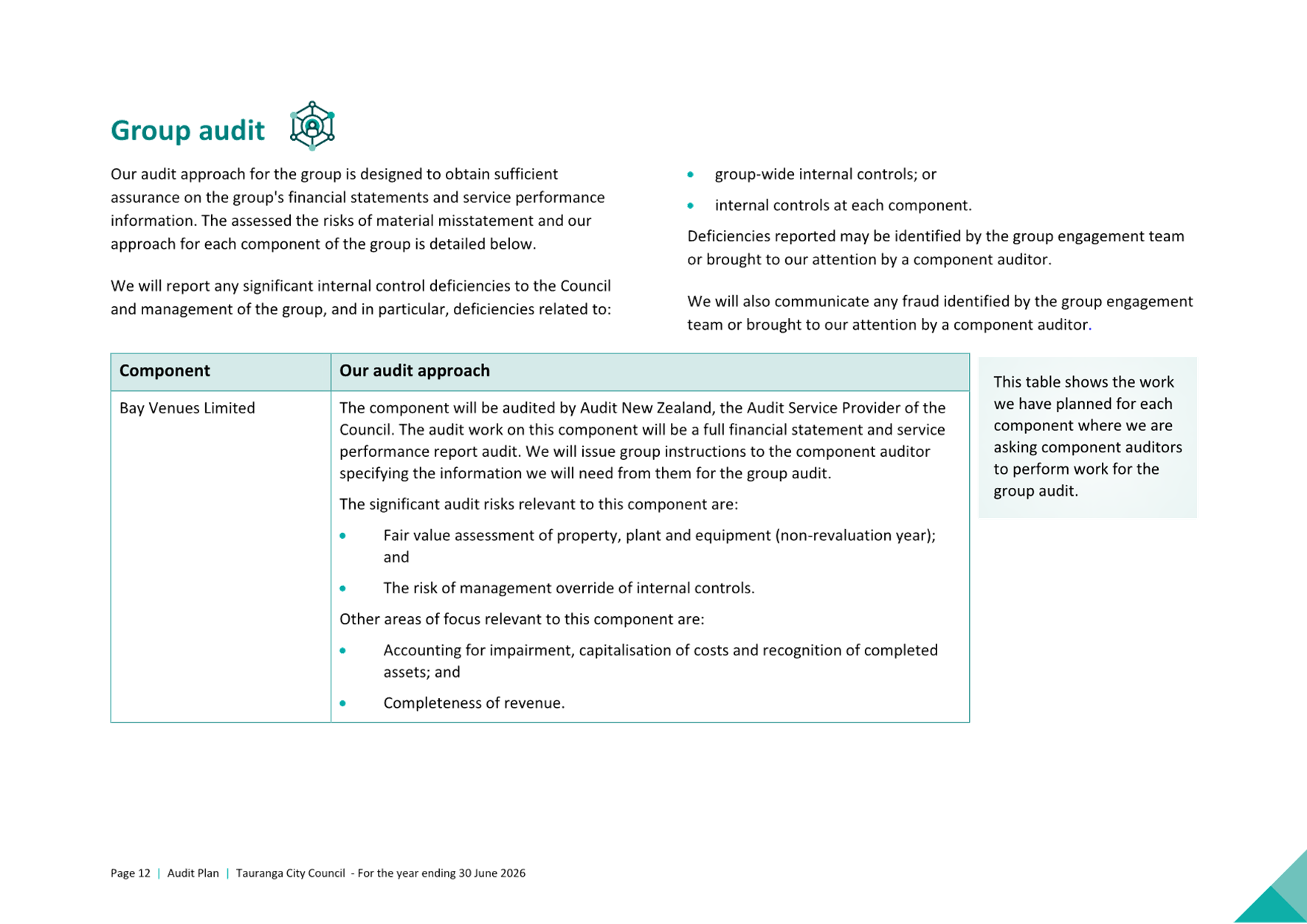

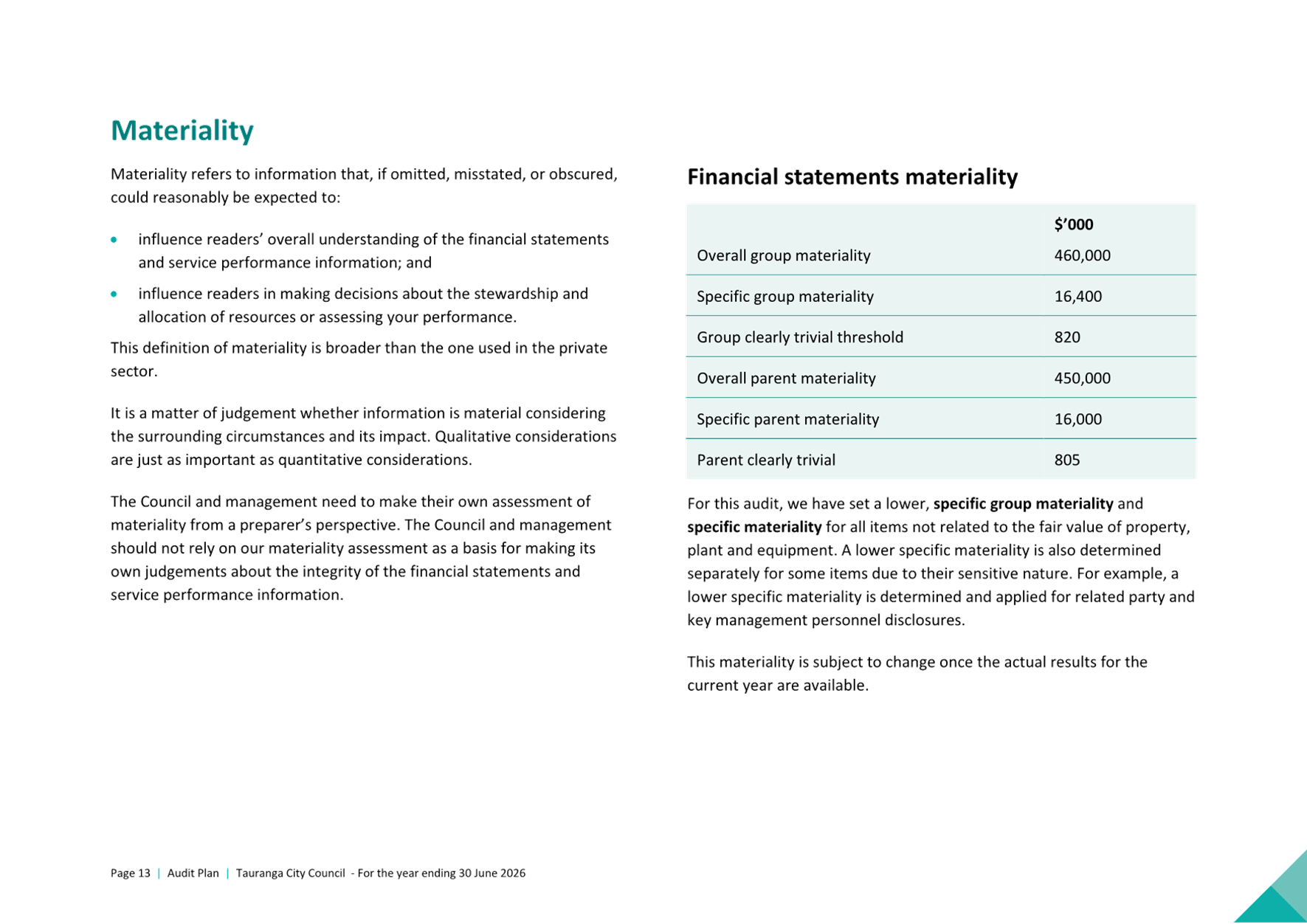

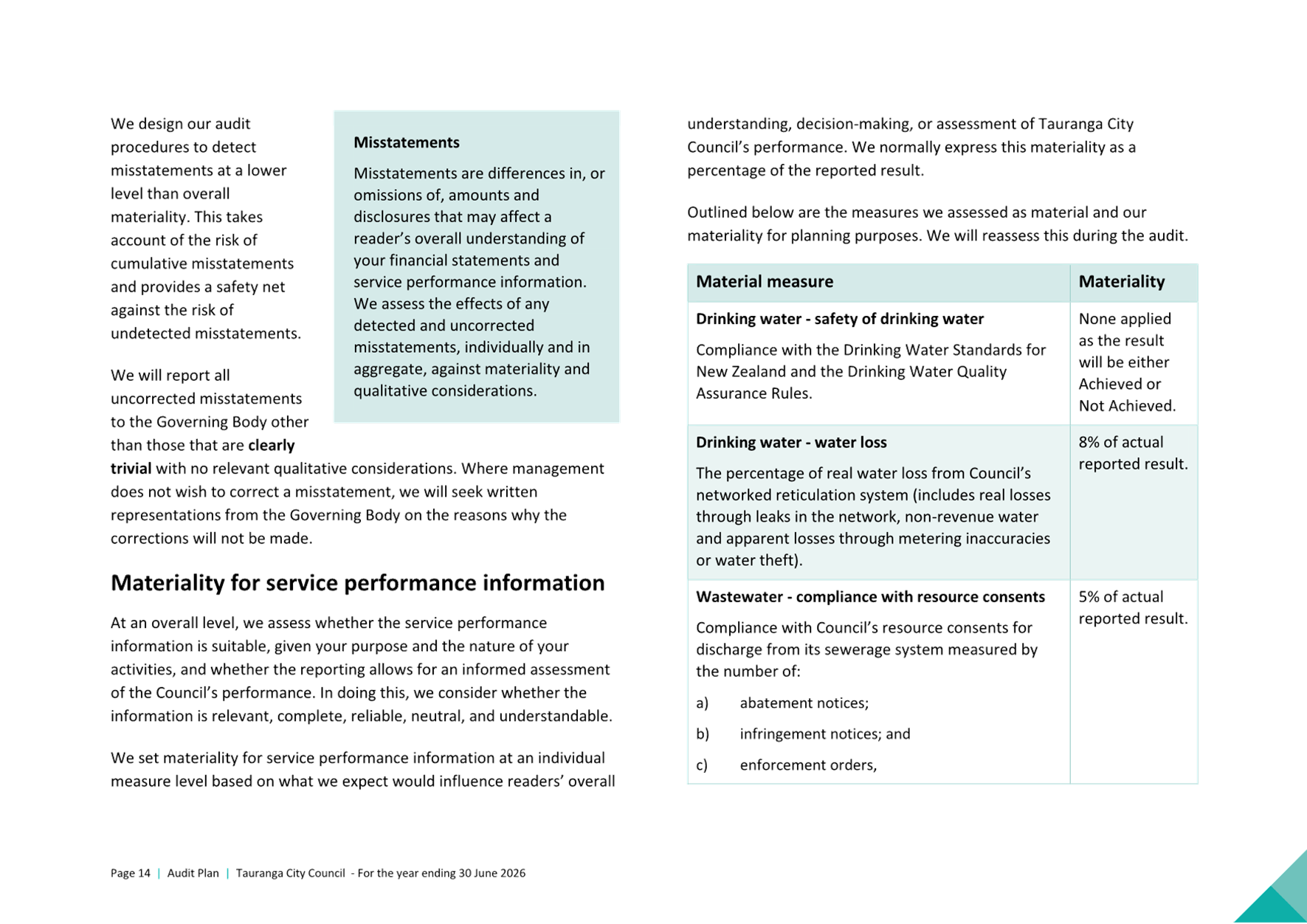

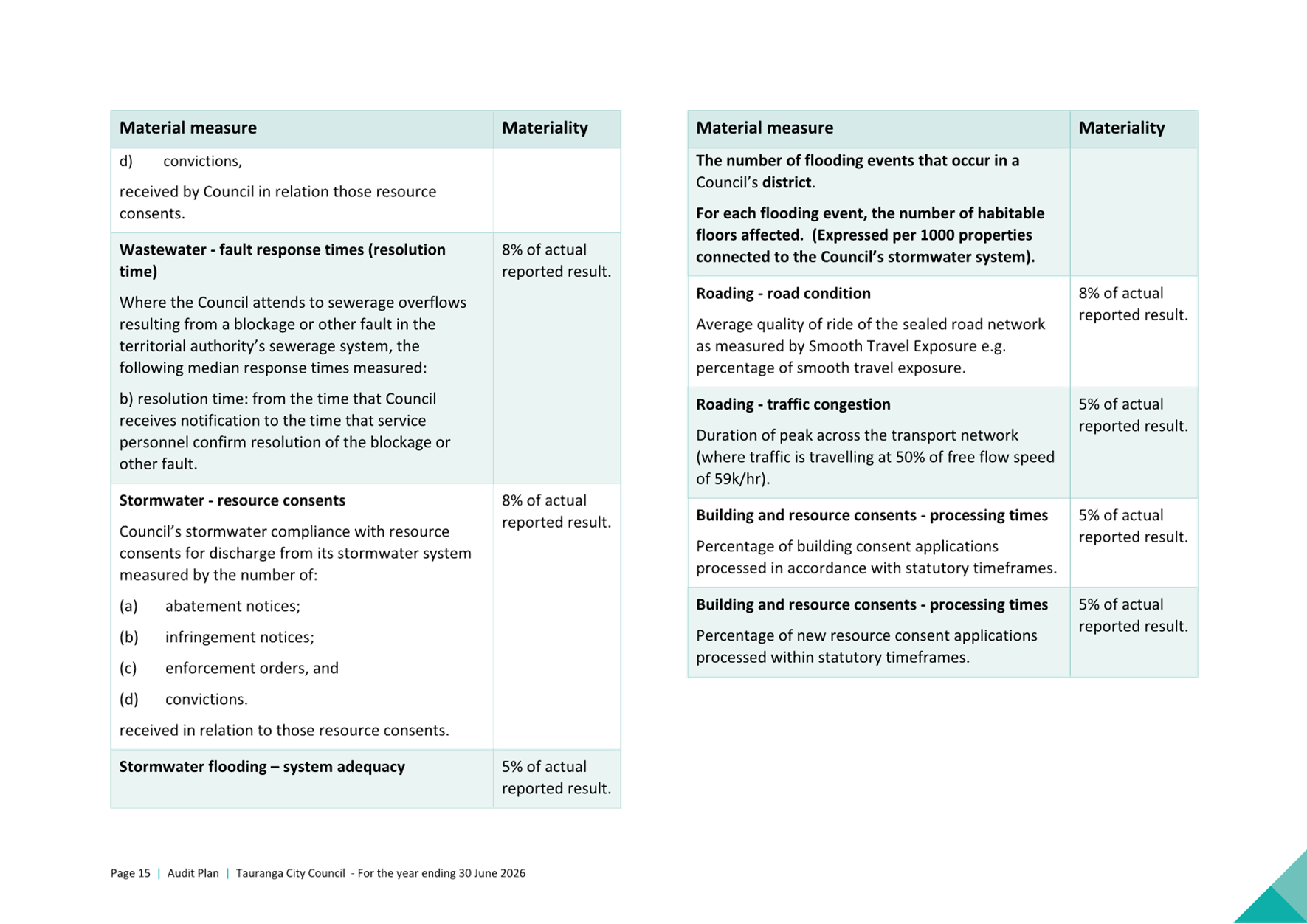

1. 2025

Report to Governors on the audit of TCC (Final) - A19717991 ⇩

2. 2025

Report to Management on the audit of TCC (Final) - A19717993 ⇩

3. TCC Audit Plan

June 2026 (Final) - A19753969 ⇩

|

Audit

& Risk Committee meeting Agenda

|

23

February 2026

|

|

Audit

& Risk Committee meeting Agenda

|

23

February 2026

|

|

Audit

& Risk Committee meeting Agenda

|

23

February 2026

|

|

Audit

& Risk Committee meeting Agenda

|

23

February 2026

|

9.2 Business

Continuity Policy

File

Number: A19580655

Author: Sharon

Herbst, Policy Analyst

Chris Quest,

Manager: Risk & Assurance

Chris Smith, Risk

and Business Continuity Advisor

Authoriser: Craig

Rice, General Manager: Chief Operating and Financial Officer

Purpose of the Report

1. To approve and adopt a

new Business Continuity Policy.

|

Recommendations

That the Audit &

Risk Committee:

(a) Receives the report

"Business Continuity Policy".

(b) Approves and adopts a new

Business Continuity Policy to take effect immediately which includes:

(i) Te Ao Māori

principles and council values

(ii) a commitment to

business continuity and a consistent process for all staff

(iii) governance roles and

responsibilities

(iv) assumptions about continuity and

recovery and council actions to support them

(v) activation criteria and

triggers for Business Continuity Plans

(vi) identification and management of

high-impact events.

(c) Delegates to the Chief

Operating and Financial Officer and General Counsel to make any necessary

minor drafting or presentation changes to the Business Continuity Policy,

prior to it being published.

|

Executive Summary

2. The

Audit & Risk Committee (the Committee) is asked to approve and adopt a new

Business Continuity Policy (the policy) for Tauranga City Council (the

council). This policy strengthens organisational resilience by ensuring

essential services can continue or recover quickly during disruptions through a

structured Business Continuity Management System.

3. When reviewing

policies that have a relevant international standard (such as business

continuity and risk management), the council ensures alignment with that

standard[1].

The Risk Management Policy, which was revised and approved in November 2025,

aligns with the risk standard (ISO 31000). During that review, we identified a

gap in meeting the business continuity standard (ISO 22301).

4. To address this gap,

we recommended developing a new Business Continuity Policy that provides the

necessary depth and operational clarity to make continuity arrangements

actionable, measurable, and embedded across the organisation.

5. On 19 February 2025,

the Committee agreed to include a Business Continuity Policy in its forward

work plan to be presented to the Committee in February 2026. This work aligns

with the Committee’s Terms of Reference, which include overseeing risk management

and the effectiveness of internal control systems[2].

6. The new policy sets

high-level commitments, principles, and governance responsibilities. It is

supported by an operational framework that details processes for business

impact analysis, threat and risk assessment, continuity planning, testing, and

review. Together, these documents embed resilience across the organisation and

reflect our decentralised model, where divisions must engage with continuity

planning.

7. The Executive

considered the draft policy and framework on 4 February 2026 and recommended

the Committee adopt the policy The Committee is asked to confirm the

recommended policy elements and adopt the policy (Attachment One). The

framework has been endorsed by the Executive and will guide implementation; it

does not require Committee approval. Current budgets are sufficient to support

delivery, and any additional resource needs will be addressed through standard

planning processes.

8. There is low to

moderate public interest, so no public consultation is planned.

9. There are no direct

financial implications in adopting this policy.

10. If approved, staff will

finalise the policy, begin implementation of the Business Continuity Management

System, and report progress to the Committee.

Background

11. As a

public organisation, the council must be prepared to respond effectively to

unplanned events that could impact service delivery, community wellbeing, or

organisational viability. During the recent review of the Risk Management

Policy, which now aligns with the ISO 31000 risk standard, we identified a gap

in meeting the ISO 22301 business continuity standard. To address this, a

standalone Business Continuity Policy has been developed to ensure continuity

arrangements are actionable, measurable, and embedded across the organisation.

This supports our commitment to protecting people, assets, and reputation while

maintaining public confidence.

12. The

policy and framework have been developed as complementary documents to guide

the council’s approach to resilience and service continuity.

(a) The policy sets out high-level

commitments to business continuity, principles, governance responsibilities,

and expectations for maintaining essential services.

(b) The framework operationalises

the policy by detailing the structure, processes, and tools of the Business

Continuity Management System. It includes methodologies for business impact

analysis, threat and risk assessment, continuity planning, testing, and review.

13. On 4 February 2026, the

Executive considered the draft policy and framework, endorsed the framework,

and recommended that the Committee adopt the policy.

Statutory Context

14. While

the Local Government Act 2002 does not mandate a standalone business continuity

policy, structured continuity planning supports prudent management and service

resilience, aligning with council’s obligations under the Act. The Civil

Defence Emergency Management Act 2002 requires local authorities to plan for

the continuation of essential services during and after emergencies. It

mandates coordinated emergency management planning, making business continuity

a core responsibility for councils.

15. The

Emergency Management Bill, set to replace the Civil Defence Emergency

Management Act 2002, will strengthen local accountability, raise minimum

standards for emergency planning, and ensure continuity of essential services

through a whole-of-society approach.

STRATEGIC ALIGNMENT

16. This contributes to the

promotion or achievement of the following strategic community outcome(s):

|

Contributes

|

|

We are an inclusive city

|

ü

|

|

We value, protect and enhance the environment

|

ü

|

|

We are a well-planned city that is easy to move

around

|

ü

|

|

We are a city that supports

business and education

|

ü

|

|

We are a vibrant city that embraces

events

|

ü

|

17. Business continuity planning

supports these outcomes by ensuring essential services remain available during

disruptions: protecting vulnerable communities, safeguarding environmental

assets, maintaining transport and infrastructure, enabling business and

education continuity, and preserving the city’s cultural vibrancy through

resilient event planning.

Options Analysis

18. The policy (Attachment One)

and framework have been developed as complementary documents to guide

council’s approach to resilience and service continuity.

19. The documents have been

developed collaboratively by the Risk and Assurance and the Policy team and

reviewed by the Emergency Management team. The Risk and Assurance team will

support implementation of the policy, while the Executive will endorse the policy

and approve the framework. The Committee are asked to confirm their approval of

the creation of a new policy (Issue 1), confirm the policy elements to be

included in the policy (Issue 2) and adopt the proposed policy (Attachment

One).

Issue 1: Adopting a Business Continuity Policy

20. While business continuity is

referenced in the Risk Management Policy, there is currently no standalone

document outlining the council’s overarching approach. A dedicated policy

would elevate visibility, clarify roles, and support compliance with ISO 22301.

Table 1: Options for adopting a Business Continuity

Policy

|

Option

|

Advantages

|

Disadvantages

|

|

1a

|

Create and adopt a new business continuity policy

Recommended

|

· Establishes a formal, consistent approach to continuity

planning.

· Aligns with ISO 22301 and best practice.

· Clarifies roles and responsibilities across the

organisation.

|

· Adds another document to the policy suite.

· Requires ongoing review and maintenance.

|

|

1b

|

Status quo. Do not develop a new policy and only maintain current

references within the risk management policy

|

· Keeps policy landscape simpler.

|

· Increases risk of non-compliance and reduced preparedness

for disruptions.

· Lack of commitment to develop a business continuity policy

which represents best practice.

· May lack operational clarity.

|

Issue 2: Business Continuity Policy elements

21. To ensure the policy is

comprehensive, practical, and aligned with council values and ISO 22301, the

following elements are proposed for inclusion in the policy. The recommended

content is designed to reflect strategic commitments, provide operational clarity,

and ensure cultural responsiveness.

Table 2: Options for defining policy content

|

Option

|

Advantages

|

Disadvantages

|

|

2a

|

Include Te Ao

Māori principles and council values

Recommended

|

· Supports

culturally safe practice.

· Supports

partnership with tangata whenua and inclusive decision-making

· Aligns

with Ngā Kawa Arataki/Code of Conduct.

· Builds

trust with communities.

|

· May

require ongoing training and support.

|

|

2b

|

Include a commitment to

business continuity and a consistent process for all workers

Recommended

|

· Reinforces

organisational resilience.

· Ensures

clarity and consistency across teams.

|

· May

require tailored guidance for different roles.

|

|

2c

|

Include governance

roles and responsibilities

Recommended

|

· Clarifies

accountability.

· Supports

effective implementation and oversight.

|

· Adds

length and complexity to the policy.

|

|

2d

|

Outline assumptions about

continuity and recovery and council actions to support them

Recommended

|

· Sets

realistic expectations for service levels during disruption.

· Supports

planning and resource allocation.

|

· May

require regular review as risks and operations evolve.

|

|

2e

|

Include activation

criteria and triggers for Business Continuity Plans

Recommended

|

· Ensures

clarity during disruptions.

· Supports

timely and structured response.

|

· May

require updates as new risks emerge.

· Relies

on maintenance of Business Continuity Plans

|

|

2f

|

Include identification

and management of high-impact events

Recommended

|

· Strengthens

preparedness for critical (or essential) services.

· Supports

targeted planning and testing.

|

· May

require additional coordination across teams.

|

Financial Considerations

22. Adopting

the new policy does not have any financial implications. Implementation will be

managed within existing budgets; any additional resource needs will be

addressed through standard planning processes.

Legal Implications / Risks

23. There are no significant risks

associated with the recommendations to adopt the new policy. The review

process reflects best practice guidance consistent with AS/NZS ISO 31000 and

AS/NZS ISO 22301, supporting a systematic and integrated approach to managing

risk and organisational resilience. Adoption reduces legal and reputational

risk by aligning with ISO standards and emergency management obligations

TE AO MĀORI APPROACH

24. Application

of Te Ao Māori principles in our business continuity approach has been

considered in consultation with the Takawaenga Unit. The principles section of

the proposed draft policies aligns with the council’s Code of Conduct/

Ngā Kawa Arataki. This includes specific examples of how the values guide

the approach to business continuity through Whanaungatanga and Collaboration;

Manaakitanga and Respect; Whāia te tika and Service; and Pono and

Integrity.

25. These principles guide how we

plan for and respond to disruptions in ways that uphold mana, foster

collaboration, and support inclusive recovery. Embedding these principles

strengthens trust and ensures culturally grounded recovery planning.

CLIMATE IMPACT

26. While there are no direct

impacts resulting from the adoption of this policy, continuity planning

supports resilience to climate-related disruptions.

Consultation / Engagement

27. There

is low to moderate public interest and therefore no public consultation or

engagement has been undertaken. To ensure our policy remains aligned with best

practice, the Risk and Assurance team continues to engage with sector peers,

participate in local government forums and working groups, benchmark against

other councils, review guidance from oversight bodies, incorporate feedback

from internal audits, and monitor legislative and regulatory developments. Internal

engagement included review by the Emergency Management team and endorsement by

the Executive.

Significance

28. The Local Government Act 2002

requires an assessment of the significance of matters, issues, proposals and

decisions in this report against Council’s Significance and Engagement

Policy. Council acknowledges that in some instances a matter, issue,

proposal or decision may have a high degree of importance to individuals,

groups, or agencies affected by the report.

29. In making this assessment,

consideration has been given to the likely impact, and likely consequences for:

(a) the current

and future social, economic, environmental, or cultural well-being of the

district or region

(b) any persons who are likely to be

particularly affected by, or interested in, the decision.

(c) the capacity of the local authority

to perform its role, and the financial and other costs of doing so.

30. In accordance with the

considerations above, criteria and thresholds in the policy, it is considered

that the decision is of low significance.

ENGAGEMENT

31. Taking into consideration the

above assessment, that the decision is of low significance, officers are of the

opinion that no further engagement is required prior to the Committee making a

decision.

Next Steps

32. If the Committee decides to

adopt the new Business Continuity Policy, it will take effect immediately. The

policy will be made available on council’s website, and the framework

will be available to staff internally. Implementation will include staff

training, testing of continuity plans, and regular reporting to the Committee.

Attachments

1. Draft

Business Continuity Policy - A19688013 ⇩

|

Audit

& Risk Committee meeting Agenda

|

23

February 2026

|

|

Audit

& Risk Committee meeting Agenda

|

23

February 2026

|

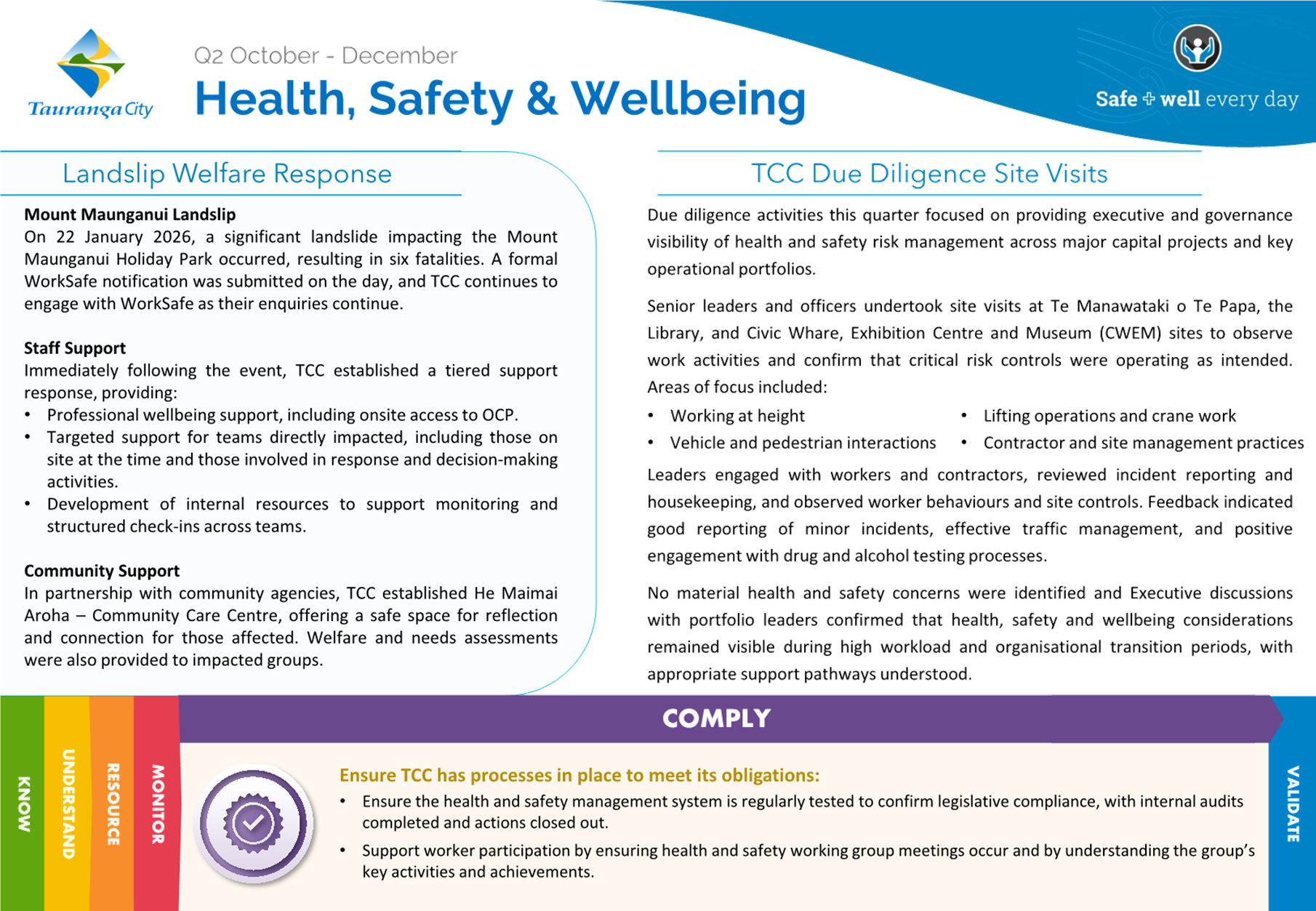

9.3 Health,

Safety and Wellbeing Quarterly Report: Q2 October to December 2025

File

Number: A19727917

Author: Tracy

Benjamin, Health, Safety & Wellness Manager

Authoriser: Craig

Rice, Chief Operating and Financial Officer

Purpose of the Report

1. To

provide an overview of Health, Safety and Wellbeing activities for the 2025

October to December quarter.

|

Recommendations

That the Audit &

Risk Committee:

(a) Receives the report

"Health, Safety and Wellbeing Quarterly Report: Q2 October to December

2025".

|

Executive Summary

2. Health,

Safety and Wellbeing – Q2 2025/26: This report provides a summary of

health, safety and wellbeing activities and outcomes for the quarter, intended

to keep the Audit and Risk Committee informed. Key data for this quarter is to

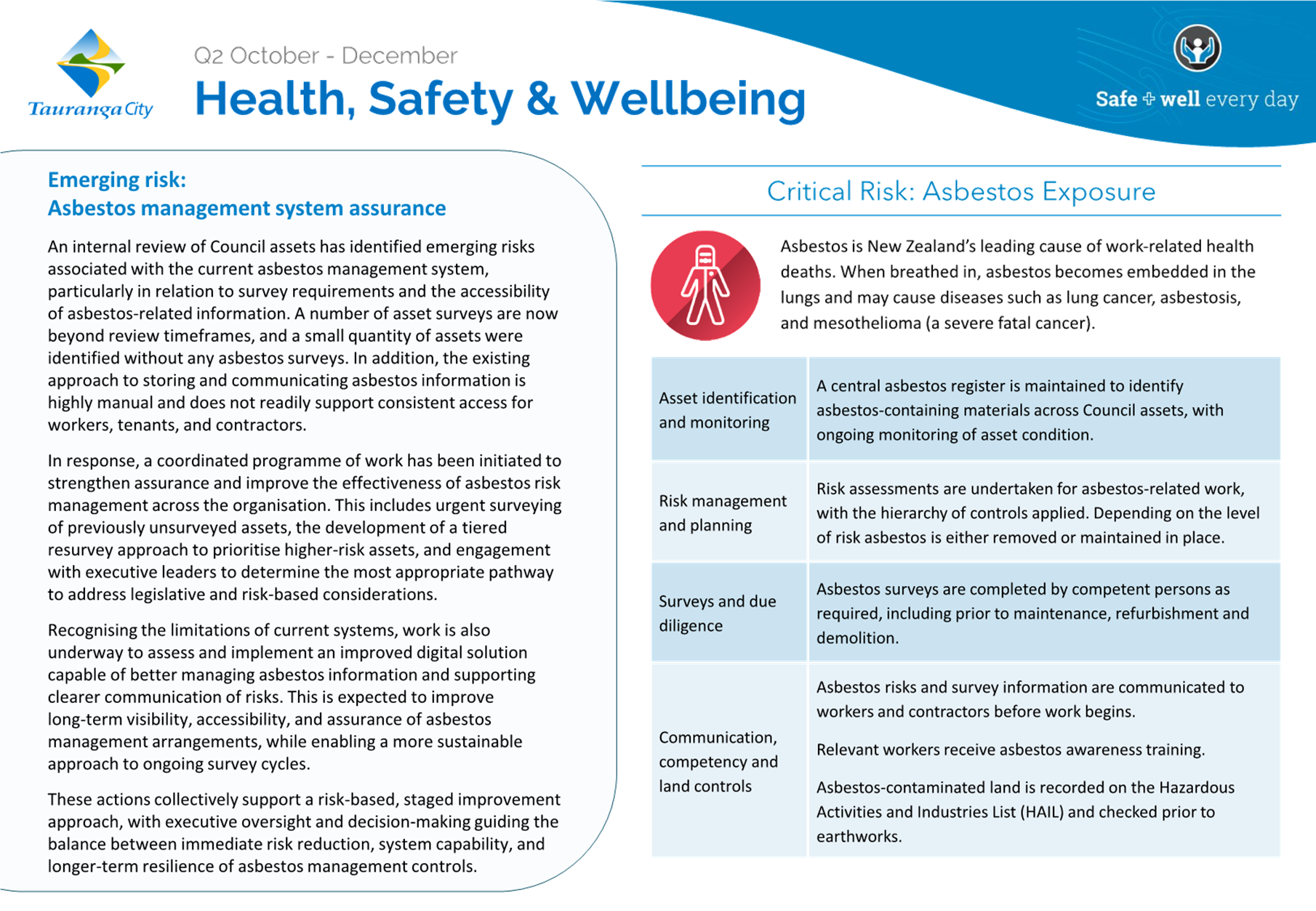

raise awareness on an emerging risk with asbestos and acknowledge the recent

landslip event. Whilst the landslip event did not occur within the reporting

period, the significance warranted entry into this report. Any feedback

regarding content or topics that the Committee would like is welcome.

3. Major

Event – Mount Maunganui Landslip: A significant landslip occurred on

22 January 2026 at the Mount Maunganui Holiday Park, resulting in six

fatalities. Council submitted a WorkSafe notification on the day and continues

to fully engage in enquiries.

4. Emerging

Risk – Asbestos Management: An internal review identified improvement

opportunities within council’s asbestos management system. A structured

programme of work has commenced to strengthen assurance, prioritise high-risk

assets for resurveying, and assess digital solutions to improve visibility,

communication, and long-term management of asbestos-related risk.

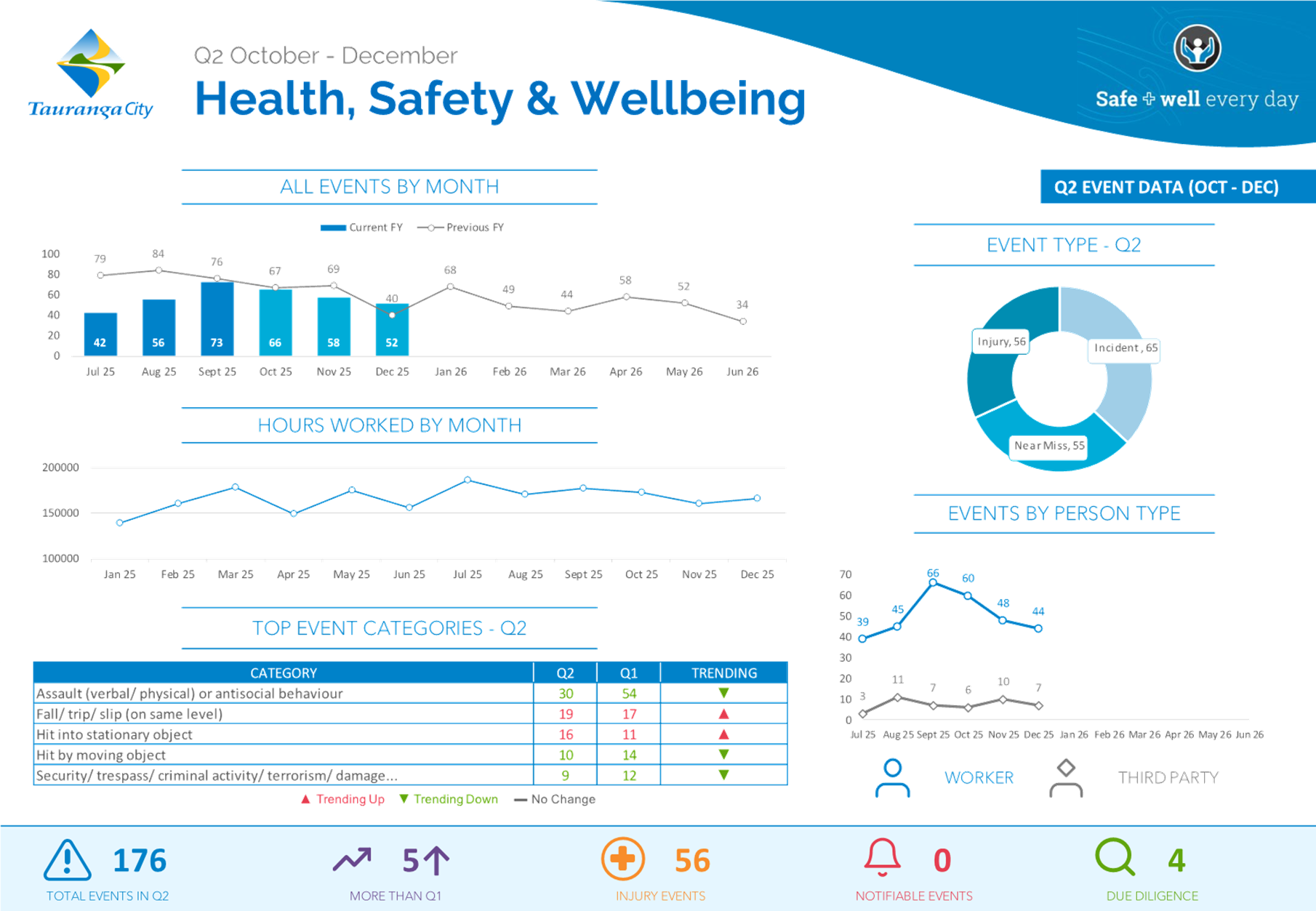

5. Event

Data and Reporting Metrics: Work is nearing completion to refine event

categorisation. This will improve accuracy, enable clearer insights into event

data, and support more targeted interventions.

Attachments

1. 2025_26

Q2_HSW Quarterly Report_PDF - A19712125 ⇩

|

Audit

& Risk Committee meeting Agenda

|

23

February 2026

|

|

Audit

& Risk Committee meeting Agenda

|

23

February 2026

|

|

Audit

& Risk Committee meeting Agenda

|

23

February 2026

|

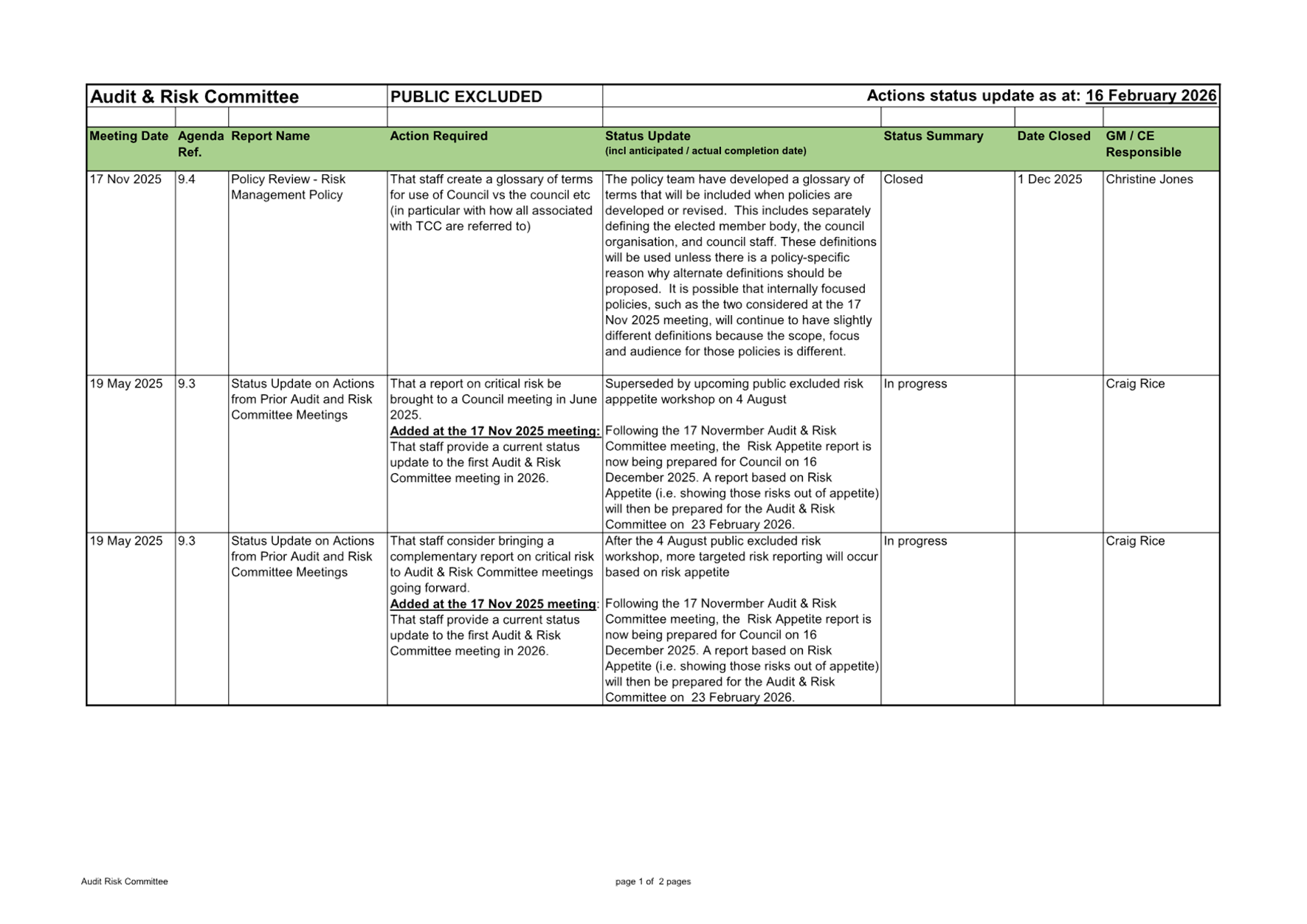

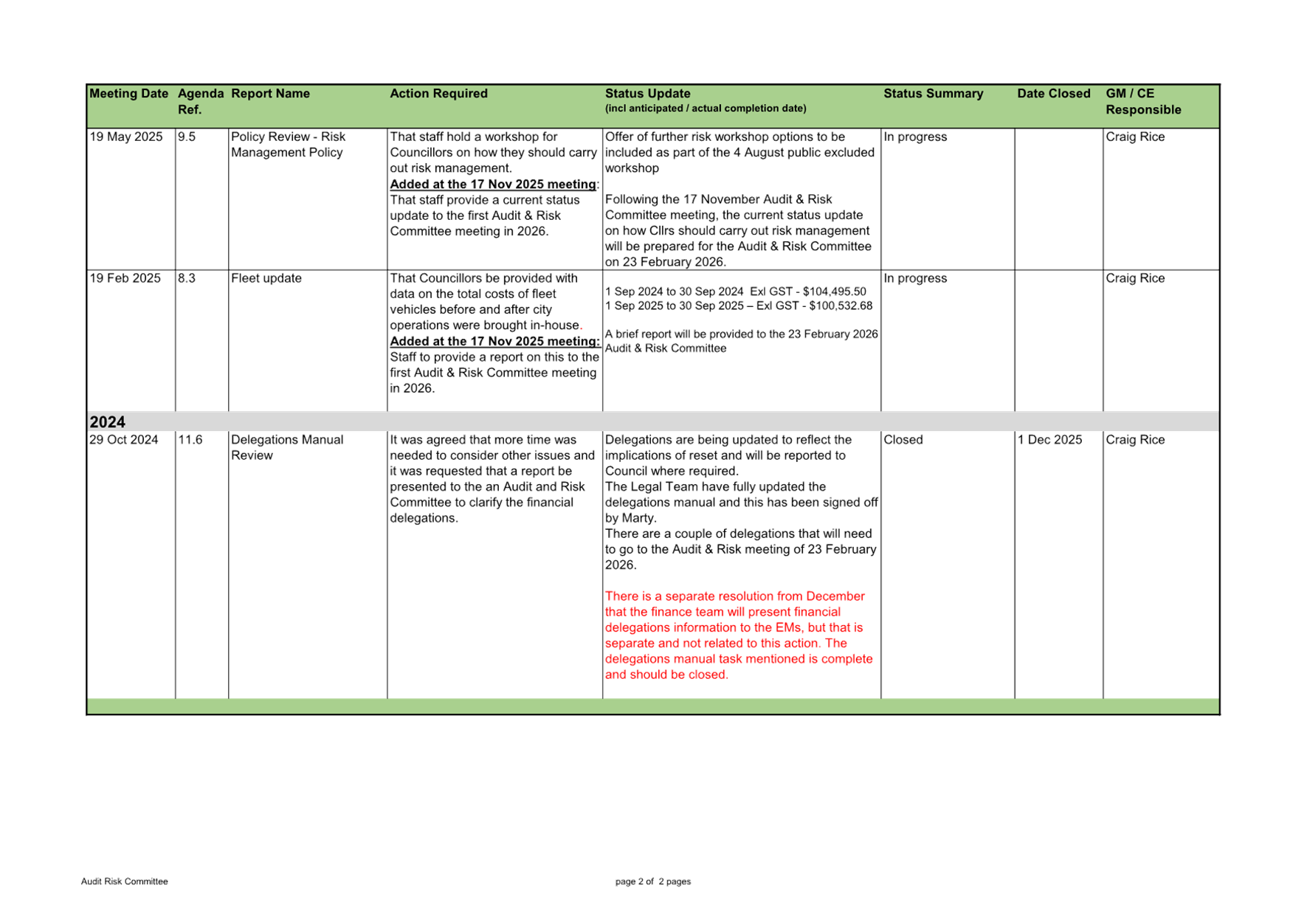

9.5 Status

Update on actions from prior Audit & Risk Committee meetings

File

Number: A19711970

Author: Anahera

Dinsdale, Governance Advisor

Authoriser: Craig

Rice, Chief Operating and Financial Officer

Purpose of the Report

1. This report provides

a status update on actions requested during previous Audit & Risk Committee

meetings.

|

Recommendations

That the Audit &

Risk Committee:

(a) Receives

the report "Status Update on actions from prior Audit & Risk

Committee meetings".

(b) Public

excluded Attachment can be transferred into the open once

the report that generated this action is released from public excluded.

|

Background

2. This is a recurring

report provided to each Audit & Risk Committee meeting. The next report

will be provided to the meeting on 5 May 2026.

3. The attached update

includes all open actions and actions completed since the last report on 17

November 2025. Once reported, completed actions are archived and made available

in the Stellar library[3].

discussion

4. A summary of

outstanding and recently closed actions is provided in the table below:

|

Status of actions

|

No. actions

|

|

Closed (completed

since the last report)

|

4

|

|

In progress

|

7

|

|

Pending (waiting

on something)

|

0

|

|

To be actioned

|

0

|

|

Total actions

included in this report

|

11

|

5. The full status

update information is provided as:

Attachment

1 (5 actions from public agenda items) and

Attachment

2 ( 6 actions from public excluded agenda items).

Attachments

1. Actions

from Audit and Risk Committee Open 23 February 2026 - A19771074 ⇩

|

Audit

& Risk Committee meeting Agenda

|

23

February 2026

|

|

Audit & Risk Committee meeting Agenda

|

23 February 2026

|

10 Discussion

of late items

|

Audit & Risk Committee meeting Agenda

|

23 February 2026

|

11 Public

excluded session

Resolution to exclude

the public

|

Recommendations

That the public be

excluded from the following parts of the proceedings of this meeting.

The general subject

matter of each matter to be considered while the public is excluded, the

reason for passing this resolution in relation to each matter, and the

specific grounds under section 48 of the Local Government Official

Information and Meetings Act 1987 for the passing of this resolution are as

follows:

|

General subject of each matter to be

considered

|

Reason for passing this resolution in

relation to each matter

|

Ground(s) under section 48 for the

passing of this resolution

|

|

11.1 - Public Excluded Minutes of the

Audit & Risk Committee meeting held on 17 November 2025

|

s7(2)(a) - The withholding of the information is

necessary to protect the privacy of natural persons, including that of

deceased natural persons

s7(2)(b)(i) - The withholding of the information

is necessary to protect information where the making available of the

information would disclose a trade secret

s7(2)(j) - The withholding of the information is

necessary to prevent the disclosure or use of official information for

improper gain or improper advantage

|

s48(1)(a) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

11.2 - Internal Audit & Assurance

- Quarterly Update

|

s7(2)(j) - The withholding of the information is

necessary to prevent the disclosure or use of official information for

improper gain or improper advantage

|

s48(1)(a) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

11.3 - Risk Register - Quarterly

Update

|

s7(2)(j) - The withholding of the information is

necessary to prevent the disclosure or use of official information for

improper gain or improper advantage

|

s48(1)(a) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

11.4 - Health, Safety and Wellbeing

Quarterly Report: Q2 October to December 2025

|

s7(2)(a) - The withholding of the information is

necessary to protect the privacy of natural persons, including that of

deceased natural persons

|

s48(1)(a) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

11.5 - Digital/Cyber Risk Quarterly

Report

|

s7(2)(a) - The withholding of the information is

necessary to protect the privacy of natural persons, including that of

deceased natural persons

s7(2)(b)(i) - The withholding of the information

is necessary to protect information where the making available of the

information would disclose a trade secret

|

s48(1)(a) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

11.6 - Public Excluded Attachment to

Item 9.5 - Status Update on actions from prior Audit & Risk Committee

meetings

|

s7(2)(j) - The withholding of the information is

necessary to prevent the disclosure or use of official information for

improper gain or improper advantage

|

s48(1)(a) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

|

Audit & Risk Committee meeting Agenda

|

23 February 2026

|

12 Closing

karakia