|

Ordinary Council meeting Agenda

|

21 April 2026

|

11 Business

11.1 Draft

2026-27 Annual Plan - Update at April 2026

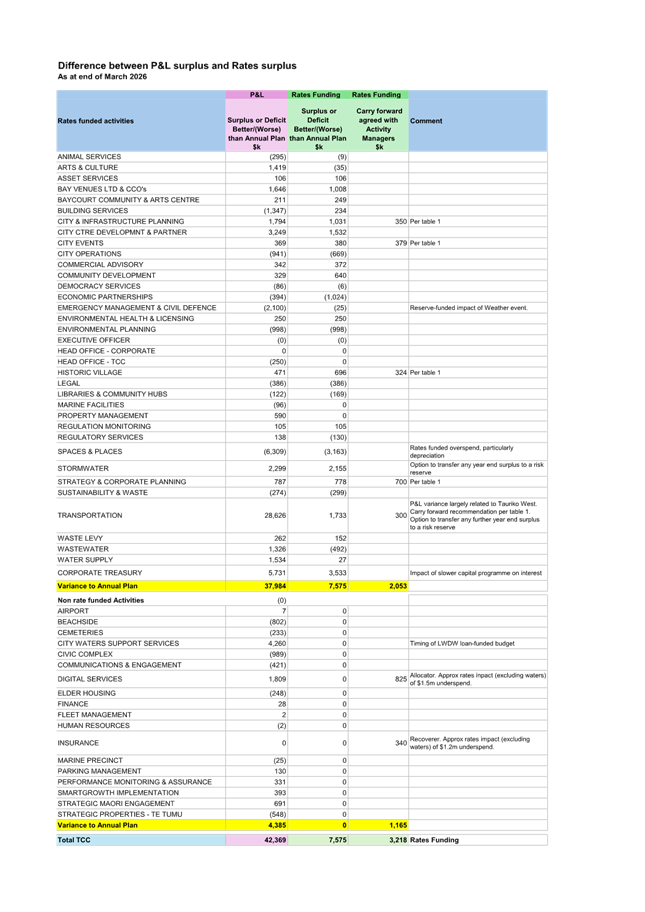

File

Number: A20107632

Author: Kathryn

Sharplin, Head of Finance

Tracey Hughes,

Manager: Organisational Financial Performance and Corporate Planning

Authoriser: Craig

Rice, Chief Operating and Financial Officer

Purpose of the Report

This report provides an

update of the 2026/27 draft annual plan identifying changes proposed to achieve

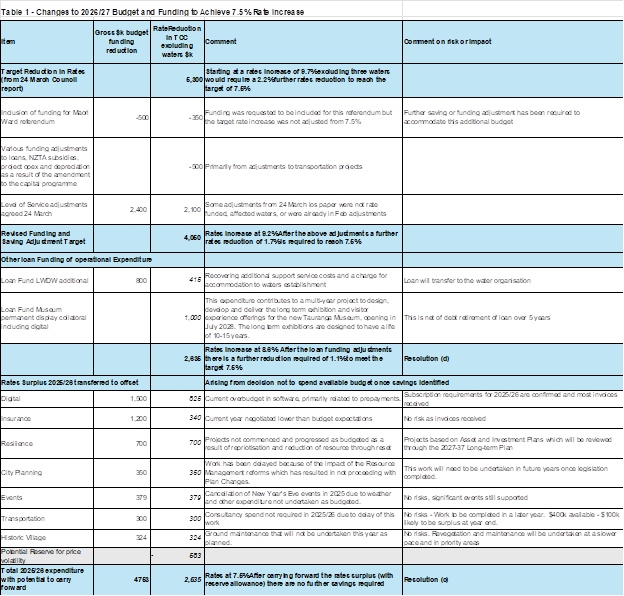

Council’s target 7.5% rate increase.

|

Recommendations

That the Council:

(a) Receives the report

"Draft 2026-27 Annual Plan - Update at April 2026".

(b) Notes that the 2025/26

organisational reset reduced expenditure budgets in the organisation by $39m

with these reductions carried through to the 2026/27 draft Annual Plan.

Development of the 2026/27 Annual Plan since 16 December 2025, has further reduced

expenditure budgets by $21m. This results in a reduction in rates

requirement across Council activities excluding three waters of $12m.

Either

(c) Agrees to funding adjustments

to reach a 7.5% rates requirement for 2026/27 by:

(i) changing the funding of

$800k of support service budgets including accommodation for 2026/27 from

allocator funding to loan-funded budget for water organisation establishment,

which is a rate reduction of $415k.

(ii) amending museum budgets for

one-off display set up costs to be loan funded, reducing rates by $1m.

(iii) carrying forward rate

surplus from the current year of $3.2m and including a reserve to buffer for

price volatility as outlined in Table 1 of this report.

Or

(d) Agrees to the following

adjustments to loan funding which will achieve a rates increase of 8.6% for

the 2026/27 Annual Plan by:

(i) changing the funding of

$800k of finance and executive leadership budget and accommodation for

2026/27 from allocator funding to loan-funded budget for water organisation

establishment, which is a rate reduction of $415k.

(ii) amending museum budgets for

one-off display set up costs to be loan funded, reducing rates by $1m.

|

.

Executive Summary

1. The Chief Executive

has led an organisational reset to support reduction of Council budgets for the

2025/26 Annual Plan. This reset reduced budgets by $39m including the

reduction of 106.7 funded positions. From direction provided as part of the

10 February 2026 and 24 March 2026 Council meetings a further $12m of rates

funding in areas excluding three waters has been removed from draft budgets for

the 2026/27 Annual Plan.

2. On 24 March 2026

Council requested the Chief Executive to consider further savings and options

to achieve a 7.5% rate increase plus any Council approved costs for Mauao

and/or cost increases due to the global situation. The required reduction in

the rates requirement in 2026/27 is $4m.

3. No further reduction

in expenditure has been recommended by the Chief Executive for this year to

reach the draft budget for 2026/27. This is because higher resourcing levels in

the short term are required to meet requirements of central government reform

including establishment of the Water Organisation (WO), the delivery of the LTP

and other efficiency and risk mitigation requirements. The alternative

would be to utilise consultants at a higher cost for these areas of work.

4. The most pressing

reform relates to establishment of the new WO from 1 July 2027. Council

will need to work closely with the new organisation to understand what support

services it requires and for how long. As part of the waters reform some support

staff are expected to transfer to the WO. Alongside transitional support,

Council will also need to consider its own internal and ongoing support

needs. This will inform resource requirements and organisational

structure during the early years of the LTP.

5. Funding adjustments

have been identified to achieve the requested rate increase of 7.5%.

These adjustments will flow through to permanent budget adjustments in

subsequent years once the WO transitional work has been completed, staff

transferred to the WO and the remaining organisation right-sized.

6. The funding changes

proposed in this report include:

(a) Loan funding more of the work

undertaken by TCC staff to support establishment of a WO. This change

will increase the WO establishment budget and therefore debt to transfer to the

WO by $800k. It reduces the allocation of support costs to council

activities by the same amount, with an estimated rates reduction of $415k

excluding waters.

(b) Funding museum set up costs of

$1.5m for long-term exhibition and visitor experience through loans, with rates

funding only of interest and debt retirement over 5-10 years as

appropriate. This change reduces rates requirement by $1m.

(c) Carrying forward to 2026/27 of

current-year rate surpluses as outlined in Table 1 to a total of $3.2m with a

portion carried through to a buffer (reserve) to help manage price volatility

arising from geopolitical uncertainty,

7. The forecast rate

surplus in Table 1 is unusually high and reflects delays and cancellation of

areas of budgeted work during the year for the reasons outlined. There

has been a directive to staff from the Executive not to find alternative use of

these budgets in favour of producing a rate surplus to support a lower rates

requirement next year.

8. A rate surplus is

not the same as a Profit and Loss surplus as shown in the financial accounts.

The profit and loss variance to budget by activity is compared with the rates

variance to budget by activity in Attachment 1.

9. The draft budgets at

this stage do not include additional funding requirement related to costs for

Mauao or cost increases due to the global situation. Further information

on these areas will be included in the final update in May prior to adoption of

the annual plan in June.

Background

10. On 24 March 2026 Council

considered “Report 11.5 Annual Plan 2026-27 Update”. As part of

this report, Council agreed a rate increase of 7.5% for three waters

activities, with total rates requirement of $145m (this includes water by meter

price per cubic metre increasing at 7.5%).

11. The rest of council excluding

three waters had a draft rate requirement of $260m, an increase over the

previous year of 9.7% after assumed growth of 0.5%.

12. Options to reduce the rate

requirement through level of service changes were proposed in a separate report

to the same meeting “Report 11.6 Annual Plan 2026/27 Levels of Service

Options”. Council agreed to total rates reduction through level of

service changes equivalent to approximately $2.1m of rates, which left a draft

rates increase of $258m. Additional costs were added in to fund the

Māori Ward referendum and recognising the operating impacts associated

with the revised capital programme.

13. After decisions from both

reports on 24 March (reports 11.5 and 11.6), Council agreed:

14. (l) to request the CE to

consider further savings and options to achieve 7.5 percent plus any Council

approved costs for Mauao and/or cost increases due to the global situation.

discussion

Expenditure Reductions

Through Resets, Efficiency Savings and LOS reduction

15. Council has already undertaken

a significant reduction in staff and operating expenditure across the

organisation both through the 2025/26 reset and in reaching the April draft

Annual Plan for 2026/27.

16. The Chief Executive has led an

organisational reset to support reduction of Council budgets for the 2025/26

Annual Plan. This reset reduced budgets by $39m including the reduction

of 106.7 funded positions. From direction provided as part of the 10

February 2026 and 24 March 2026 Council meetings a further $12m of rates

funding in areas excluding three waters has been removed from draft budgets for

the 2026/27 Annual Plan.

17. There are several initiatives

requiring significant support staff input over the next 18 months including:

(a) Establishment of the WO.

(b) Development of shared services

to support the WO for a transitional period and the transfer of some support

staff.

(c) Organisational reset post

establishment of the WO once service level agreements are in place and with a

view to future state of core council.

(d) Development of the 2027-37

Long-term Plan

(e) Advice on and then

implementation of proposed Government reform including regional council

governance, planning and regulation, rates capping and changes to reporting

requirements

(f) Efficiency improvements

and risk mitigation including migrating off ozone

18. No further adjustments to

budgets and staffing are recommended by the Chief Executive at this stage

because of the above work programme. The organisation needs to be

sufficiently resourced to meet the additional work required. The

alternative would be to engage more costly consultants to undertake this

work. The proposal to fund the water transition work through loans

reduces the operational funding of support services base budgets from

2026/27. These changes will flow through as part of the organisational

reset post WO transition.

Funding Review to reduce rates requirement to 7.5%

19. Council staff have identified

areas of rate funded expenditure this year that have not been spent to date as

planned. There has been a directive not to find alternative uses of these

budgets in favour of producing a rate surplus to support a lower rates

requirement next year. Key areas of underspend which activity managers have

committed to are identified in Table 1 below. For the 9 months to 31 March

2026, Council activities have underspent on rate-funded expenditure by $7.6m

(Attachment 1). Not all this underspend is expected to translate into a

rate surplus at year end.

20. Table 1 also presents two loan

funding recommendations for next year’s budget.

21. The first is funding $800k of

support service expenditure including accommodation budgets as additional

loan-funded waters transition budget, reflecting the significant amount of work

to be undertaken as part of stage 2 establishment. This change will reduce

overall rates requirement by 415k. It will increase the debt to transfer to the

water organisation by $800k.

22. The second loan funded proposal

is in relation to one-off museum set up costs of exhibition displays and

customer experience expenditure. In the March 2026 draft, all this

one-off expenditure was funded by rates. However, because most of this

expenditure relates to set up costs including interactive digital displays that

will last 5 to 10 years, it is more appropriate to be loan funded with rates

used to retire the debt over an appropriate timeframe.

23. Use of 2025/26 unspent rates to

fund 2026/27 expenditure will impact the rate-funding increase required in

2027/28, unless further expenditure reduction is achieved in that year.

Expenditure Risks

24. Transportation and

stormwater activities are currently significantly underspent on rates

funded expenditure. Transportation is forecasting to be fully spent by

year end other than the consultancy budget identified in Table 1. Stormwater

may not be fully spent in areas related to open drain clearing. There

would be opportunity at year end to consider options for carrying forward

significant unspent maintenance budget in stormwater including to a risk

reserve in response to higher costs associated with fuel prices.

25. Interest rates will also

be affected by any long-term disruption to fuel and oil supplies from the

Middle East conflict. At present the Reserve Bank is looking through

short term price impacts but has signalled inflation will be responded to by a

raising of interest rates. Markets are now forecasting multiple increases

in the OCR from July. No change has yet been made to interest rate assumptions

in the Annual Plan. There is currently a rate surplus relating to

debt levels and interest costs this year. Options for carrying forward a

surplus to a reserve will be considered in June.

Rates surplus compared with Operating Surplus

26. A rate surplus is not the same

as a Profit and Loss surplus as shown in the financial accounts (Statement of

Comprehensive Revenue and Expenses – SOCRE). The profit and loss variance

to budget by activity is compared with the rates variance to budget by activity

in Attachment 1.

27. Rates are not the only funding

source for operating expenditure. Other sources include subsidies and fees and

charges as well as reserves and in some cases loan funding consistent with the

Revenue and Financing Policy.

28. The Statement of Comprehensive

Revenue and Expense (SOCRE) presents all “operational” expenditure

as defined by accounting standards that is recognised in the year, regardless

of whether it is funded from operational revenue (rates and charges), loans,

reserves (which represent funding from previous years) or is simply a non-cash

accounting entry. Mark to market adjustments for interest rate swaps are

an example of gains or losses recorded against the surplus that are not

realised losses. Expenditure that has occurred in the past that cannot be

capitalised is required to be written back in the SOCRE against operating costs

even though no expenditure has occurred in the year and the work has been loan

funded in the past. Both these items will impact recorded expenditure and

operating surplus but not rates funding.

29. Therefore, it is possible to

have a rate surplus while recording an operating deficit in the SOCRE.

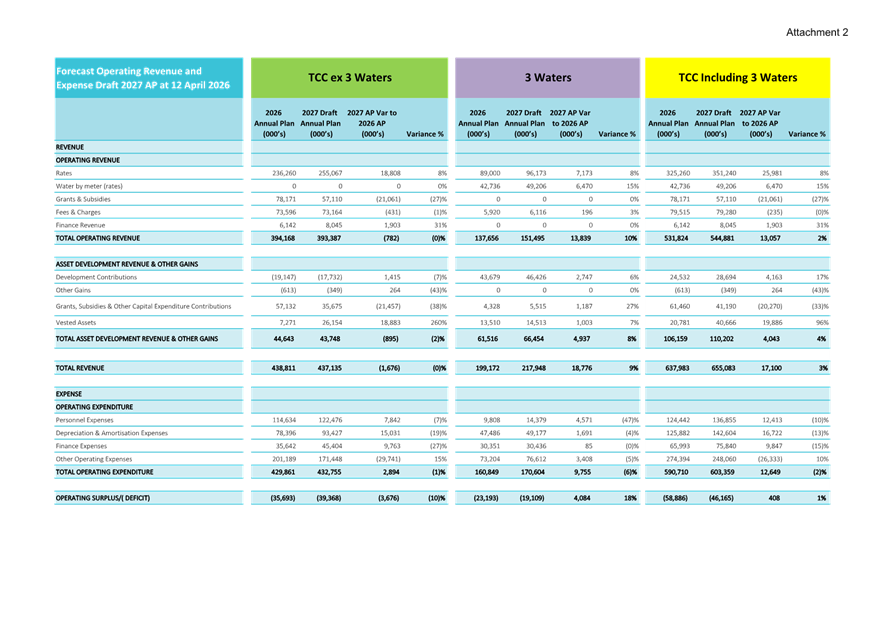

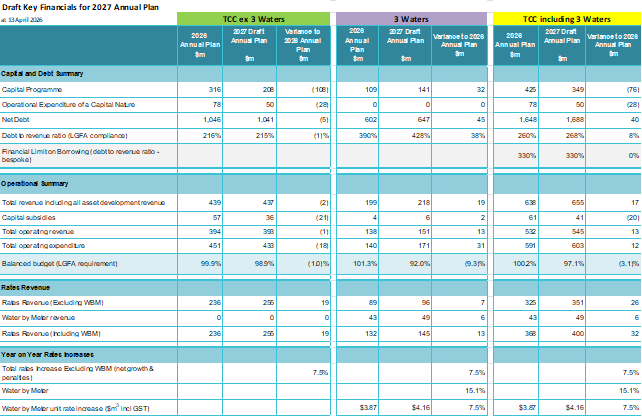

Key Financials

The following table of

key financials for TCC excluding three waters, three waters and whole of

council shows the 7.5% rate increase achieved as requested by Council.

The higher unbalanced budget shown reflects the reliance on current year

surpluses and loans to fund expenditure. The complete Statement of

Comprehensive Revenue and Expense along with graphs of operational and capital

expenditure are included as Attachment 2.

Table 2 – Key

Financials

Statutory Context

30. The Local Government Act 2002

requires Council to produce an Annual Plan. The plan is required to be

financially prudent and prepared in accordance with requirements of the Act.

STRATEGIC ALIGNMENT

31. This contributes to the

promotion or achievement of the following strategic community outcome(s):

|

Contributes

|

|

We are an inclusive city

|

ü

|

|

We value, protect and enhance the environment

|

ü

|

|

We are a well-planned city that is easy to move

around

|

ü

|

|

We are a city that supports

business and education

|

ü

|

|

We are a vibrant city that embraces

events

|

ü

|

32. The Annual Plan aligns with all

community outcomes as it represents the resources Council commits to run the

organisation and deliver services grants to other organisations and capital

investments to achieve these outcomes

Options Analysis

33. The options to be considered in

this report are either to accept all of the funding adjustments proposed to

reach a target rate increase of 7.5% or to accept only the loan funded

adjustments to achieve a rate increase for TCC excluding three waters of up to

8.6%.

Option 1 - Accept all the proposed funding adjustments to

achieve a rate increase of 7.5%

|

Summary

|

Advantages

|

Disadvantages/Risks

|

|

Agree to

Loan funding of LWDW

additional establishment expenditure,

Loan funding of museum

display set up costs, and

Carry forward of rate

surpluses as outlined in Table 1.

|

Enables a lower rates

increase of 7.5%.

Carry forward of rates

surplus ensures rates collected for an activity are spent on that activity.

Loan funding of support

service and accommodation costs in the establishment of the new water

organisation reflects the true costs of waters transition.

Loan funding of the

museum display set up reflects that this expenditure will provide benefit

over 5 to 10 years not just the year it occurs.

|

Funding 2026/27-year

expenditure from carry forward of rate surplus means 2027/28 budgets would

require larger rate increase to achieve the same level of expenditure in

future and will encourage further efficiency savings.

There is a risk that

over expenditure elsewhere may reduce the rates surplus although this is

being carefully monitored

Loan funding of

expenditure and use of previous years funding will bring the balanced budget

measure further below 100%

Not meeting the

prudence benchmark would need to be explained to the Board of Local

Government Funding Agency (LGFA) and could put at risk the bespoke borrowing

covenant. Current debt levels are within standard LGFA borrowing limits

so TCC does not require the bespoke covenant in 2026/27.

|

Option 2 – Agree to the amendment to loan funding but

not the carry forward of current year rates surplus to achieve a rate increase

of 8.6%.

|

Summary

|

Advantages

|

Disadvantages/Risks

|

|

|

|

|

Agree to

Loan funding of LWDW

additional establishment expenditure, and

Loan funding of museum

display set up costs

|

The balanced budget

metric is still less than 100% but more favourable than in option 1. Advice

to LGFA would still be required.

The rate base would be

higher going forward if a rate cap were to be applied for the following year.

Any rate surplus could

be used to retire debt or fund reserves for the purpose of managing future

rate requirements.

|

The rate increase would

be higher at 8.6%, which increases the cost to ratepayers over option 1.

The unmet balanced

budget benchmark would still require explanation to the Board of LGFA as

required under the conditions of the bespoke covenant and could risk the

bespoke covenant being withdrawn. Current debt levels are within

standard LGFA borrowing limits so TCC does not require the bespoke covenant

in 2026/27.

|

|

|

|

Financial Considerations

34. Carry forward of rates surplus

from areas underspent this year enables the budgeted level of expenditure for

next year to be funded at a lower rate increase than otherwise. It uses

the rates collected for the purpose intended in the 2025/26 Annual Plan when

the rates were struck. Loan funding of one-off expenditure that provides

benefit over a number of years is appropriate funding for this type of

expenditure under the Council’s Revenue and Financing Policy. The true

costs of setting up a water organisation include the additional costs to be

funded through increased loan funded budget proposed.

35. However, use of debt to fund

expenditure creates an unbalanced budget under the balanced Budget measure as

set out in the Financial Regulations 2014. It also requires that Council

explain to the Board of LGFA why the budget is unbalanced. It is noted

that Council’s debt to revenue ratio does not utilise the additional

borrowing capacity of the bespoke covenant as total debt to revenue remains

within the ratios under the standard LGFA covenants.

Legal Implications / Risks

36. There are no specific legal

implications associated with the update on the annual plan. However,

decisions on resourcing, which are actioned through the Annual Plan, may have

an impact on the level of risk associated with the organisation’s operations

and delivery.

37. The Middle East conflict is

having an immediate impact on fuel and interest costs which have not been

incorporated in interest and opex and capex costs in this Annual Plan

update. The update in May prior to adoption of the Annual Plan will

incorporate the latest assumptions at that time.

38. There is a risk that the LGFA

Board may require Council to increase its revenue to ensure a balanced budget

measure above 100% to retain the bespoke covenant.

TE AO MĀORI APPROACH

39. The Annual Plan represents

resourcing to include the outcomes agreed by Council. The outcomes are

addressed through decisions on activities, capital expenditure and

services. These should align with Council’s Te Ao Māori

approach. The level of resourcing for the Annual Plan should have regard

to the agreed outcomes and deliverables the expenditure aims to achieve.

CLIMATE IMPACT

40. The Annual Plan includes both

operating and capital expenditure to adapt to a changing climate, reduce

emissions and enhance nature and biodiversity. These initiatives are

included in the Groups of Activity information

Consultation / Engagement

41. Council has resolved not to

consult on the 2026/27 Annual Plan, but that it would like material to be

available related to this draft to support a survey to be undertaken in April

2026, commencing 14 April. The material associated with this report will

be available on the agenda to the 21 April Council meeting from 15 April 2026.

Significance

42. The Local Government Act 2002

requires an assessment of the significance of matters, issues, proposals and

decisions in this report against Council’s Significance and Engagement

Policy. Council acknowledges that in some instances a matter, issue,

proposal or decision may have a high degree of importance to individuals,

groups, or agencies affected by the report.

43. In making this assessment,

consideration has been given to the likely impact, and likely consequences for:

(a) the current

and future social, economic, environmental, or cultural well-being of the

district or region

(b) any persons who are likely to be

particularly affected by, or interested in, the matter.

(c) the capacity of the local authority

to perform its role, and the financial and other costs of doing so.

44. In accordance with the

considerations above, criteria and thresholds in the policy, it is considered

that the matter is of medium significance.

ENGAGEMENT

45. Taking into consideration the

above assessment, that the matter is of medium significance, officers are of

the opinion that no further engagement is required prior to Council making a

decision.

Next Steps

46. Council will receive a further

update on financials at the 25 May Council meeting. It is required to

adopt the Annual Plan 2026/27 in June 2026, noting the draft is expected to be

updated for:

(a) changes to the delivered

capital programme and proposed carry forward and 2026/27 capital budgets

(b) changes to proposed opex

budgets as a result of Council decisions or other significant events

(c) changes to costs of capital or

operational budgets as a result of costs for Mauao or cost increases due to the

global situation.

Attachments

1. Difference

between P&L Surplus and Rates Surplus - A20123725 ⇩

2. Updated Operating

Revenue and Expense - A20123767 ⇩