|

|

|

AGENDA

Ordinary Council meeting

Tuesday, 24 March 2026

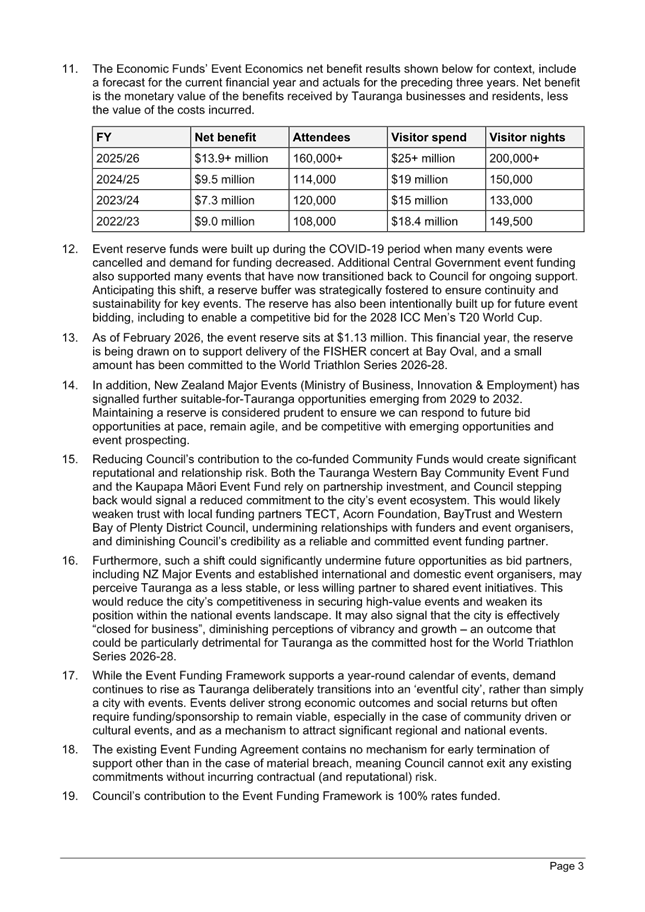

|

|

I hereby give notice that an Ordinary meeting of

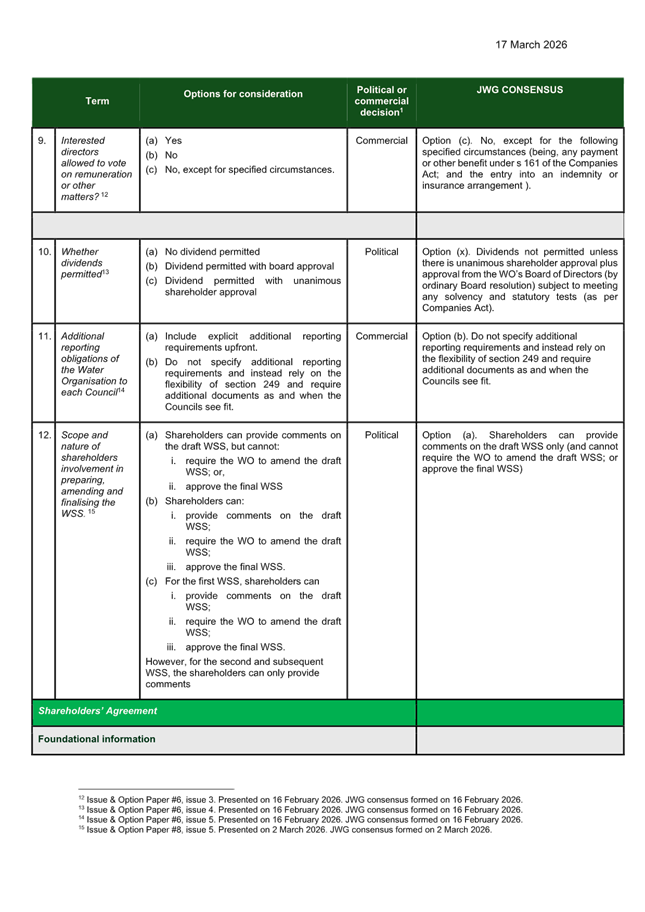

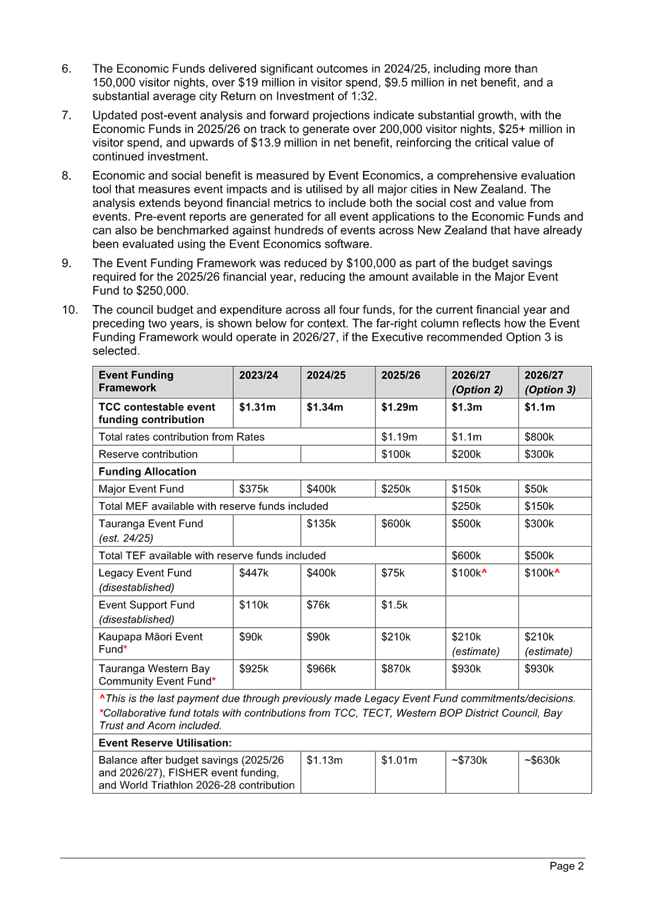

Council will be held on:

|

|

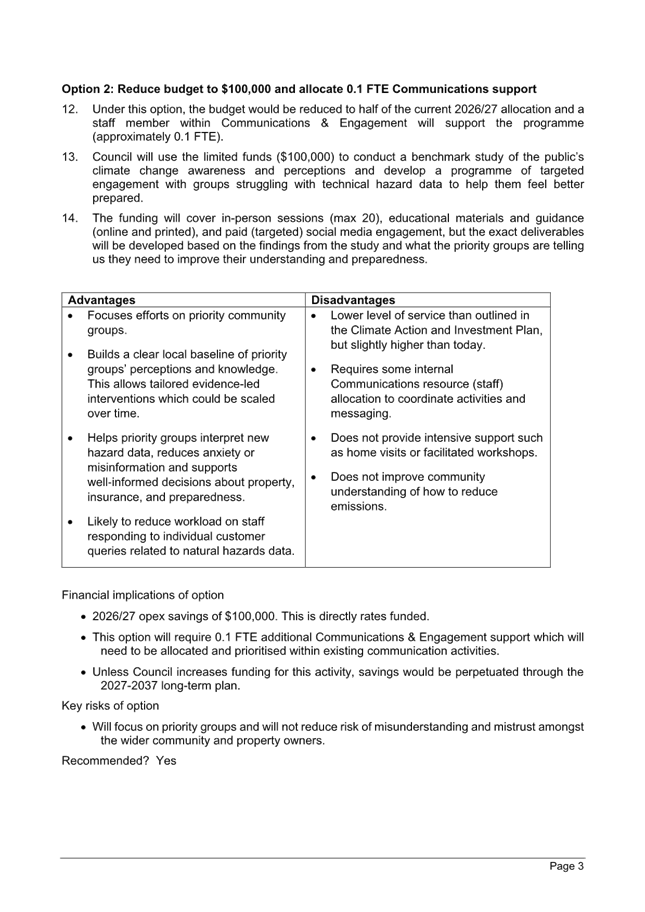

Date:

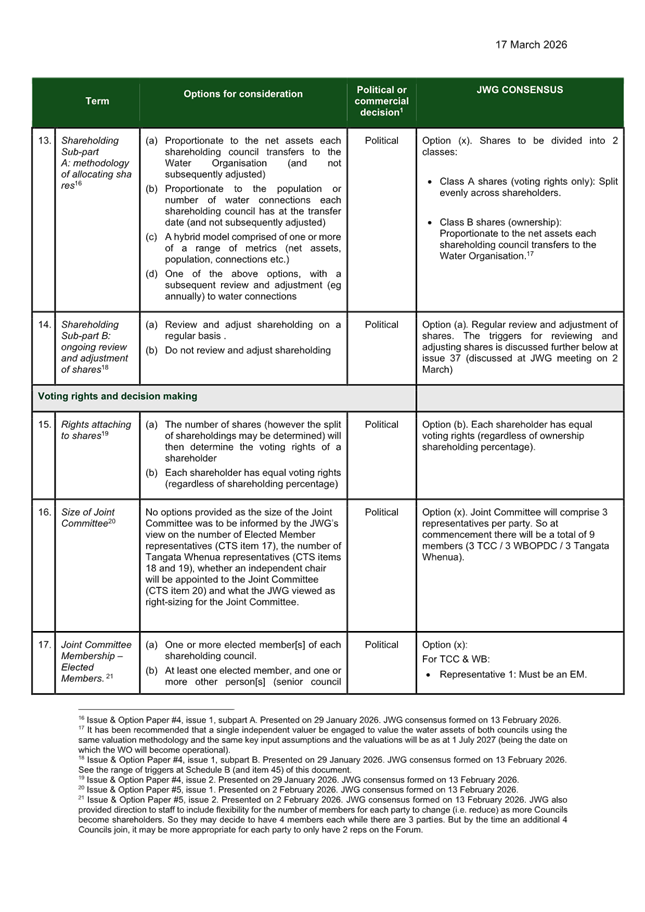

|

Tuesday, 24 March 2026

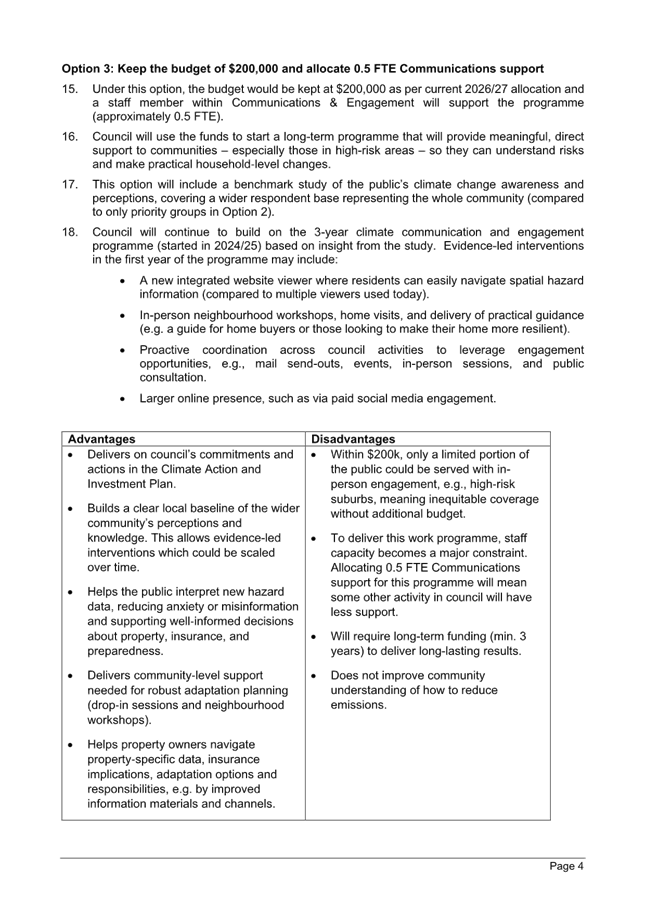

|

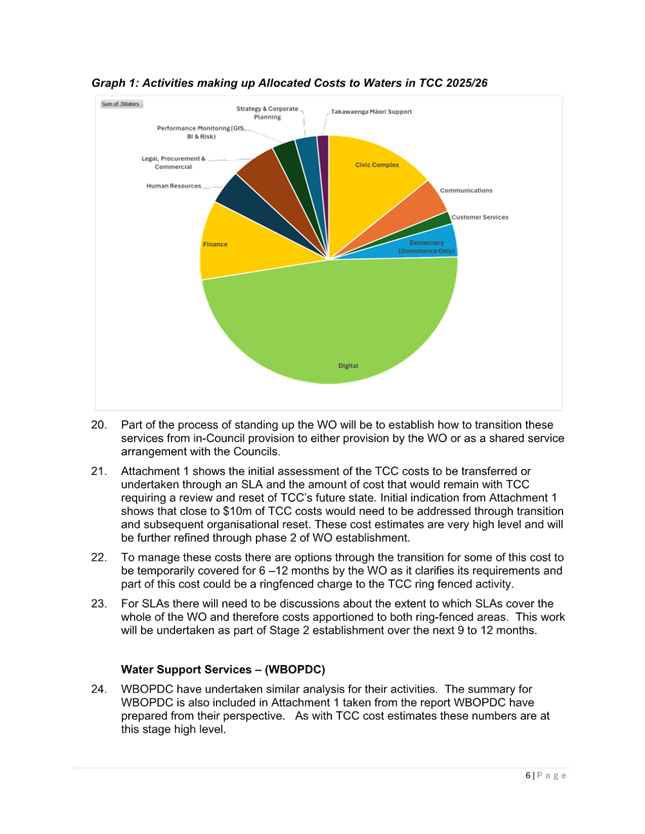

|

Time:

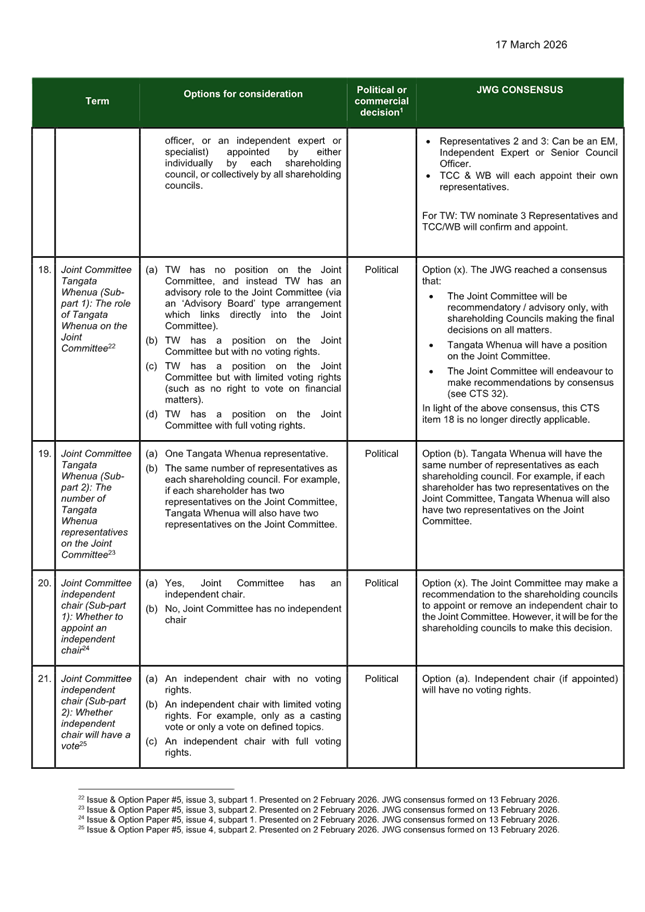

|

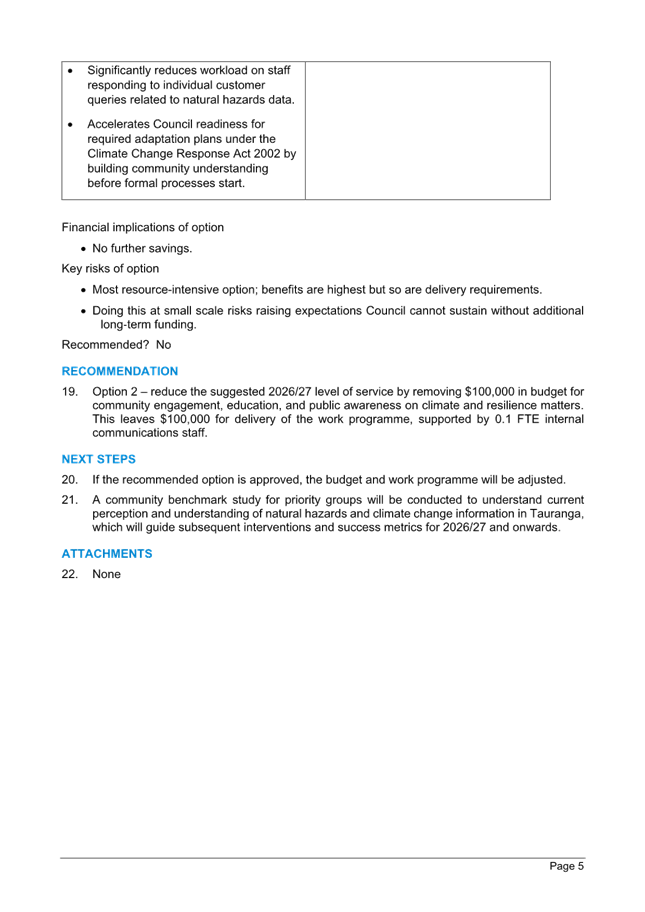

9:30 am

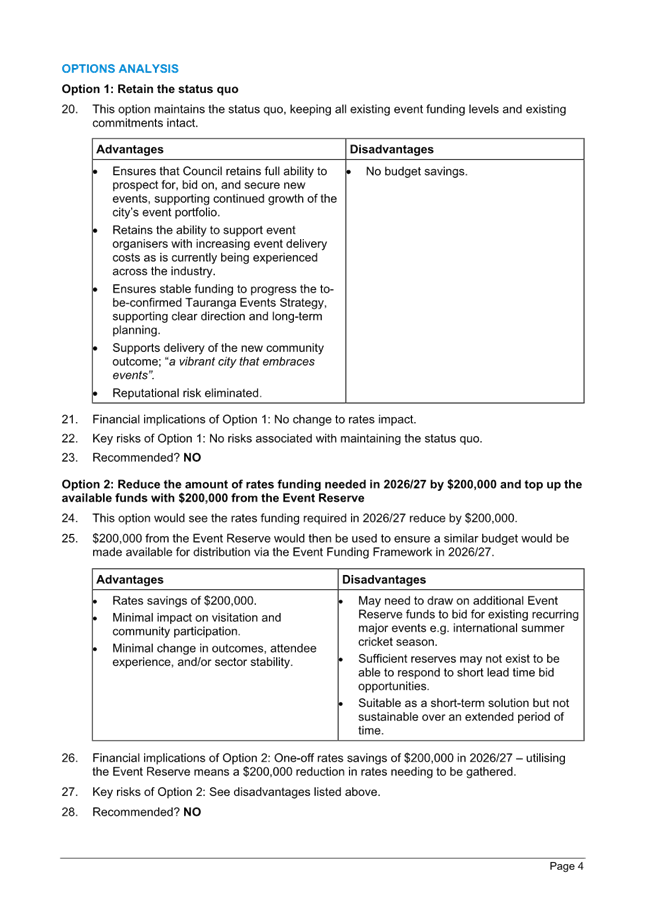

|

|

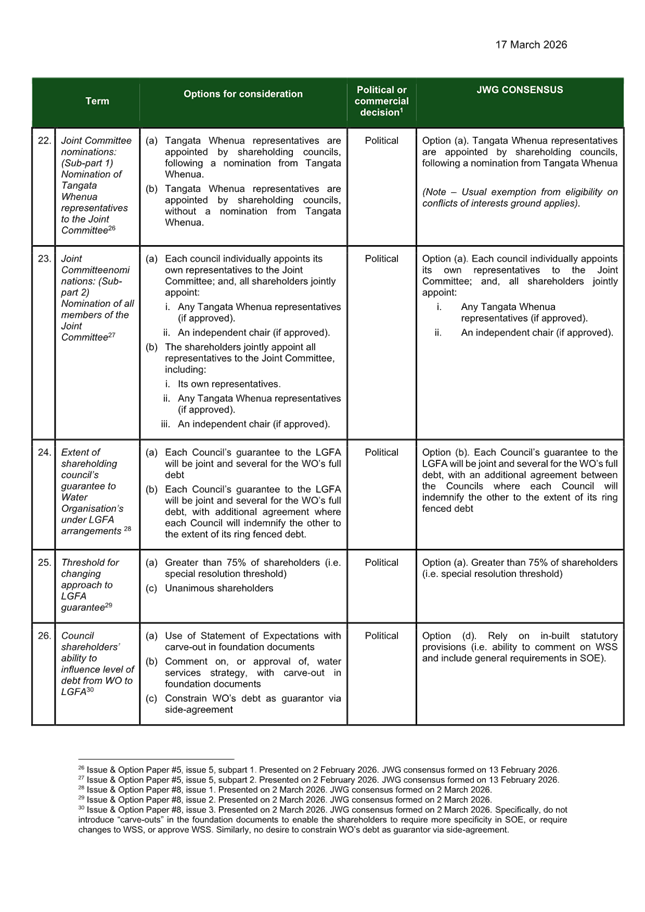

Location:

|

Tauranga City Council Chambers, Mareanui

L1, 90 Devonport Road

Tauranga

|

|

Please note that this

meeting will be livestreamed and the recording will be publicly available on

Tauranga City Council's website: www.tauranga.govt.nz.

|

|

Marty Grenfell

Chief Executive

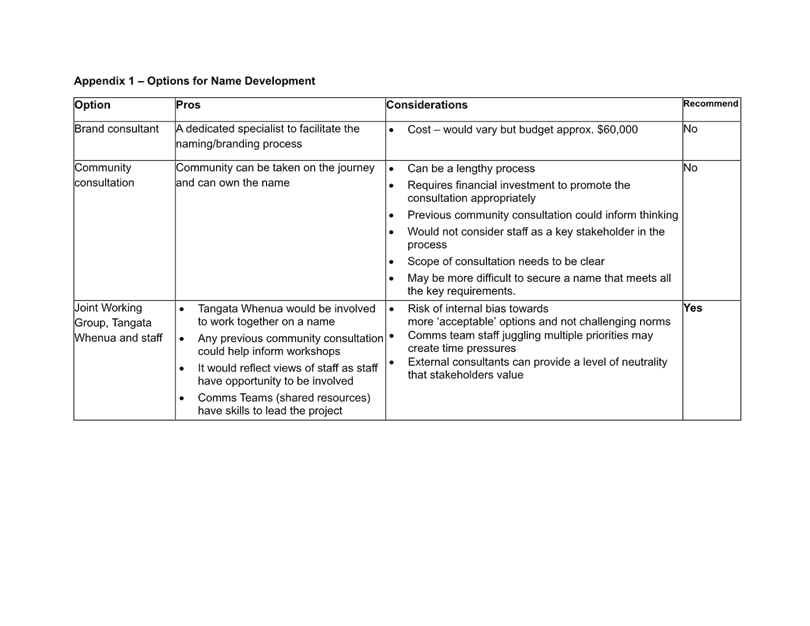

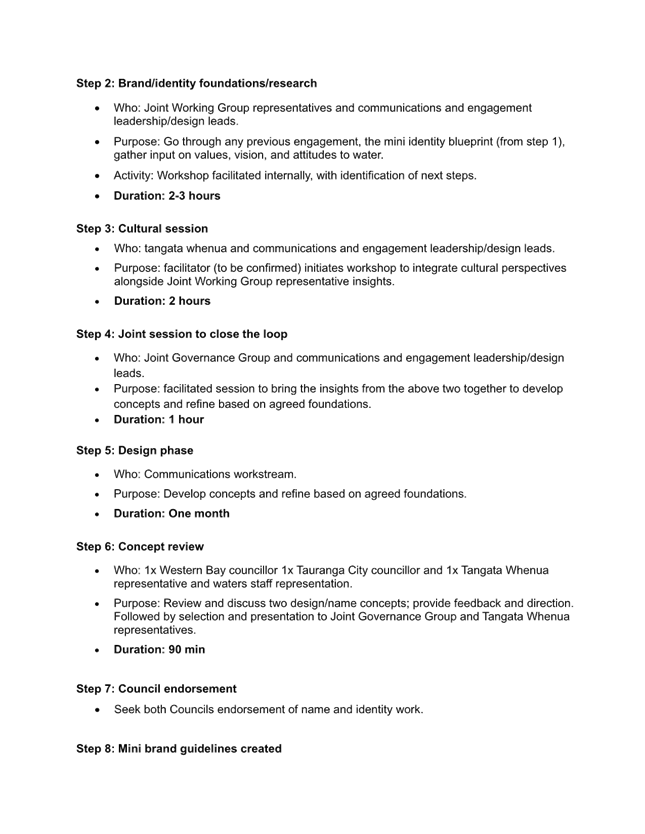

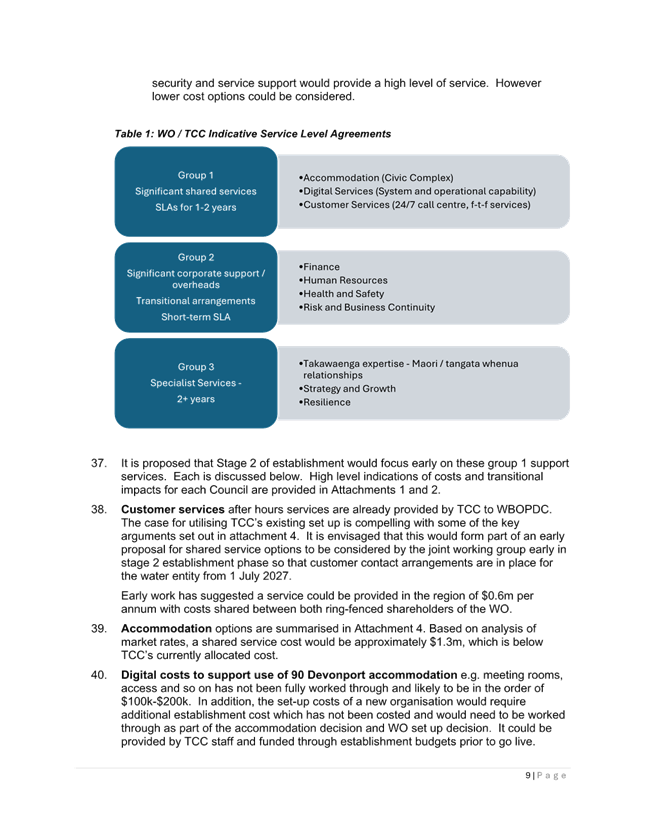

|

Terms of reference – Council

Membership

|

Chair

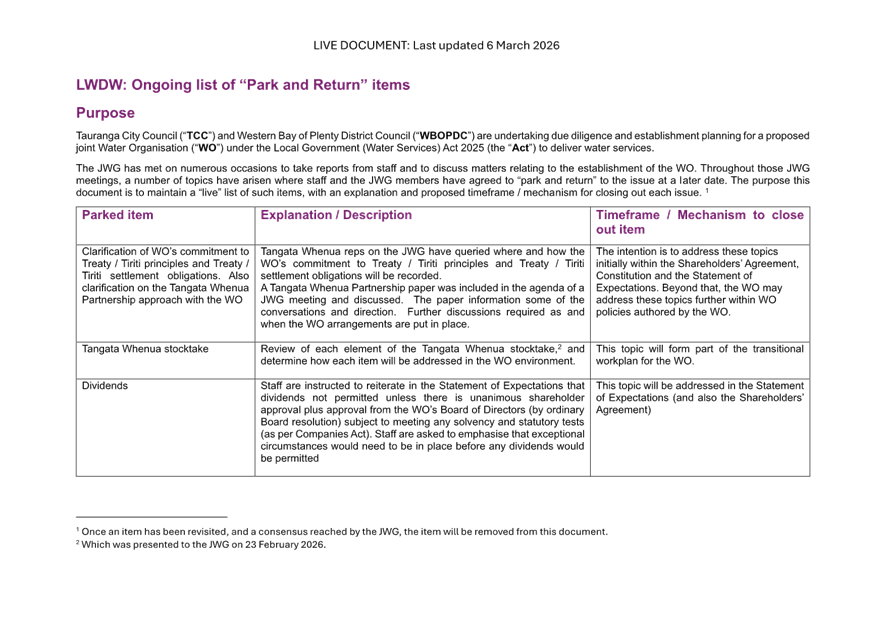

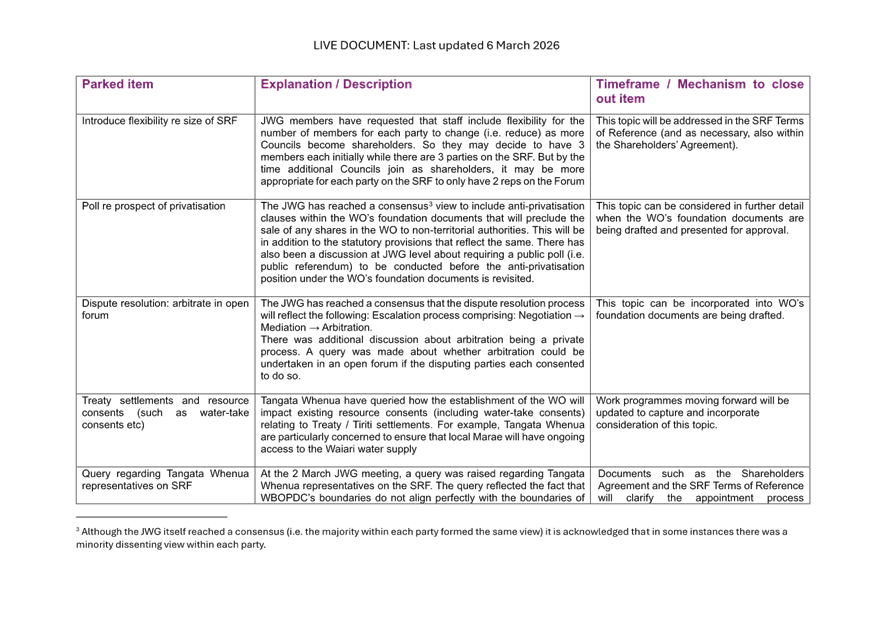

|

Mayor

Mahé Drysdale

|

|

Deputy Chair

|

|

|

Members

|

|

|

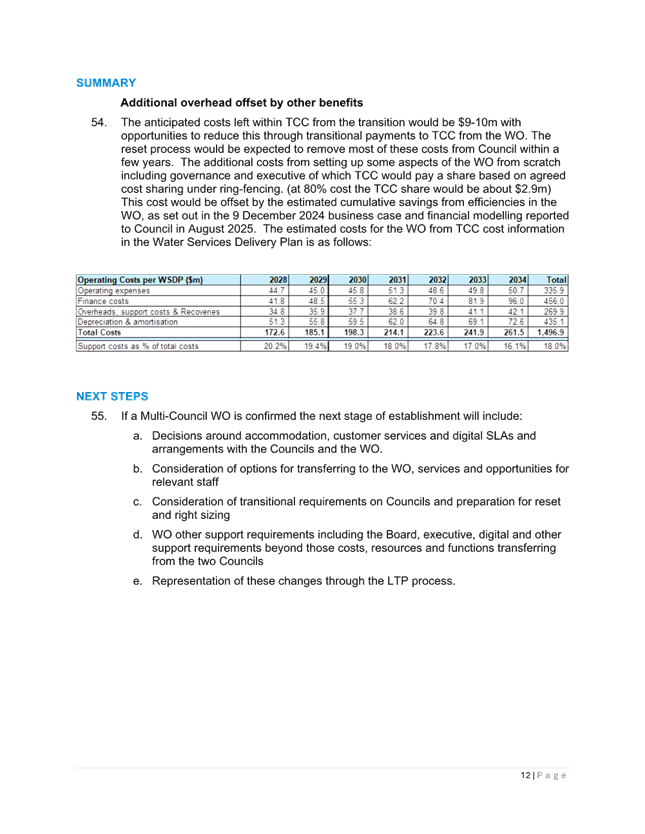

Quorum

|

Half of the members

present, where the number of members (including vacancies) is even;

and a majority of the members present, where the number of members

(including vacancies) is odd.

|

|

Meeting frequency

|

Three weekly or as required

|

Role

·

To ensure the effective and efficient governance

of the City.

·

To enable leadership of the City including

advocacy and facilitation on behalf of the community.

·

To review and monitor the performance of the

Chief Executive.

Scope

·

Oversee the work of all committees and

subcommittees.

·

Exercise all non-delegable and non-delegated

functions and powers of the Council.

·

The powers Council is legally prohibited from

delegating include:

○

Power to make a rate.

○

Power to make a bylaw.

○

Power to borrow money, or purchase or dispose of

assets, other than in accordance with the long-term plan.

○

Power to adopt a long-term plan, annual plan, or

annual report

○

Power to appoint a chief executive.

○

Power to adopt policies required to be adopted

and consulted on under the Local Government Act 2002 in association with the

long-term plan or developed for the purpose of the local governance statement.

○

All final decisions required to be made by

resolution of the territorial authority/Council pursuant to relevant

legislation (for example: the approval of the City Plan or City Plan changes as

per section 34A Resource Management Act 1991).

·

Council has chosen not to delegate the

following:

○

Power to compulsorily acquire land under the

Public Works Act 1981.

·

Make those decisions which are required by

legislation to be made by resolution of the local authority.

·

Authorise all expenditure not delegated to

officers, Committees or other subordinate decision‑making bodies of

Council.

·

Make appointments of members to the council-controlled

organisation Boards of Directors/Trustees and representatives of Council to

external organisations.

·

Undertake statutory duties in regard to

Council-controlled organisations, including reviewing statements of intent,

with the exception of the Local Government Funding Agency where such roles are

delegated to the City Delivery Committee. (Note that monitoring of all

Council-controlled organisations’ performance is undertaken by the City

Delivery Committee. This also includes Priority One reporting.)

·

Consider all matters related to Local Water Done

Well.

·

Consider any matters referred from any of the

Standing or Special Committees, Joint Committees, Chief Executive or General

Managers.

·

Review and monitor the Chief Executive’s

performance.

·

Develop Long Term Plans and Annual Plans

including hearings, deliberations and adoption.

Procedural matters

·

Delegation of Council powers to Council’s

committees and other subordinate decision-making bodies.

·

Adoption of Standing Orders.

·

Receipt of Joint Committee minutes.

·

Approval of Special Orders.

·

Employment of Chief Executive.

·

Other Delegations of Council’s powers,

duties and responsibilities.

Regulatory matters

Administration, monitoring and

enforcement of all regulatory matters that have not otherwise been delegated or

that are referred to Council for determination (by a committee, subordinate

decision‑making body, Chief Executive or relevant General Manager).

1 Opening

karakia

2 Apologies

|

Ordinary Council meeting Agenda

|

24 March 2026

|

3 Public

forum

3.1 Matt

Cowley - Tauranga Business Awards

Attachments

Nil

3.2 Shad

Rolleston on behalf of the Tangata Whenua Working Group Members

Attachments

Nil

3.3 Sam

Allen

Attachments

Nil

|

Ordinary Council meeting Agenda

|

24 March 2026

|

7 Confirmation

of minutes

7.1 Minutes

of the Council meeting held on 10 February 2026

File

Number: A19859702

Author: Clare

Sullivan, Senior Governance Advisor

Authoriser: Sarah

Holmes, Team Leader: Governance & CCO Support Services

|

Recommendations

That the Minutes of the

Council meeting held on 10 February 2026 be confirmed as a true and correct

record.

|

Attachments

1. Minutes

of the Council meeting held on 10 February 2026

|

Ordinary

Council meeting minutes

|

10 February 2026

|

|

|

|

DRAFT MINUTES

Ordinary Council meeting

Tuesday, 10 February 2026

|

Order of Business

1 Opening

karakia. 3

2 Apologies. 4

3 Public

forum.. 4

3.1 Richard

Longley - Miro St Parking. 4

4 Acceptance

of late items. 4

5 Confidential

business to be transferred into the open. 4

6 Change to

the order of business. 4

7 Confirmation

of minutes. 4

7.1 Minutes

of the Council meeting held on 16 December 2025. 4

7.2 Minutes

of the Council meeting held on 2 February 2026. 5

8 Declaration

of conflicts of interest 5

9 Deputations,

presentations, petitions. 5

10 Recommendations from

other committees. 5

11 Business. 5

11.1 Local

Water Done Well - Options for Stormwater 5

11.2 Submission

on Planning Bill and Natural Environment Bill 8

11.3 Draft

Submission on Simplifying Local Government proposal 8

11.4 Rates

Capping Submission. 9

11.9 Draft

Annual Plan 2026/27. 9

11.5 User

Fees and Charges Review - Issues and Options. 12

11.6 Transport

Resolutions Report No.59. 13

11.7 Bay

of Plenty Mayoral Forum Triennial Agreement 2025-2028. 13

11.8 Miro

Street Parking Improvements. 14

12 Discussion of late

items. 15

13 Public excluded

session. 15

13.1 Public

Excluded Minutes of the Council meeting held on 26 August 2025. 15

13.2 Public

Excluded Minutes of the Council meeting held on 16 September 2025. 16

13.3 Public

Excluded Minutes of the Council meeting held on 29 October 2025. 16

13.4 Public

Excluded Minutes of the Council meeting held on 16 December 2025. 16

13.5 Council-Controlled

Organisations - Board Appointments beyond 30 June 2026. 17

Confidential Attachment 2 11.1 - Draft Annual

Plan 2026/27. 17

Confidential Attachment 3 11.1 - Draft Annual

Plan 2026/27. 17

14 Closing karakia. 17

MINUTES

OF Tauranga City Council

Ordinary Council meeting

HELD

AT THE Tauranga City Council Chambers,

L1, 90 Devonport Road, Tauranga

ON

Tuesday, 10 February 2026 AT 9:30 am

|

MEMBERS PRESENT:

|

Mayor Mahé Drysdale,

Deputy Mayor Jen Scoular, Cr Hautapu Baker, Cr Glen Crowther, Cr Rick Curach,

Cr Steve Morris, Cr Marten Rozeboom, Cr Kevin Schuler, Cr Rod Taylor, Cr

Hēmi Rolleston

|

|

IN ATTENDANCE:

|

Marty Grenfell (Chief Executive),

Christine Jones (General Manager: Strategy, Partnerships & Growth), Craig

Rice (Chief Operating & Financial Officer), Sarah Omundsen (General

Manager: Regulatory & Community), Reneke van Soest (Operations &

Infrastructure), Charles Lane (Team Leader: Commercial Legal), Stephen Burton

(Transformation Lead – Water Services), Frazer Smith (Manager:

Strategic Finance & Growth), Cathy Davidson (Water Organisation

Establishment Lead), Wally Potts (Head of City Waters), Jeremy Boase,

(Head of Strategy, Governance & Climate Resilience), Tracey Hughes

(Manager: Organisational Financial Performance & Corporate Planning),

Susan Braid (Finance Lead Capital Performance & Community Investment),

Andrew Mead, (Head of City Planning & Growth), Janine Speedy (Team

Leader: City Planning), Carl Lucca (Team Leader: Structure Planning),

Mike Seabourne (Head of Transport), Shawn Geard (Manager: Transport System),

Caroline Lim (CCO Specialist), Clare Sullivan (Senior Governance

Advisor), Caroline Irvin (Governance Advisor),

|

Timestamps are included beside each of the items and relate

to the recording of the meeting held on 10 February 2026 on the Council's YouTube channel

1 Opening

karakia

Cr Hēmi Rolleston opened the meeting with a karakia.

Reflection and moment of

silence

The Mayor paid tribute to Sir Tim Shabolt, former Mayor of

Waitakere City and Invercargill City who died on 8 January, and Jules Radich,

former Mayor and Councillor of Dunedin City who died on 4 January. He

acknowledged the service they provided and paid respect to their

families. Council marked their passing with a moment of silence.

Achievement of Sam Ruthe

The Mayor noted the recent achievement of Sam Ruthe who on 1

February broke the NZ mile record – a record that had stood for 44 years

– and a world under-18 best record in Boston. The Mayor extended the

Council’s best wishes to Sam for his continued success.

2 Apologies

Nil

3 Public

forum

|

3.1 Richard Longley - Miro St

Parking

|

|

|

|

·

Mr Longley spoke to the Miro Street Parking Improvements

report. In his opinion, the proposal of a one-way system was a major

drawback and a significant inconvenience that would affect a number of

people.

·

He estimated that there were 128 mailboxes/dwellings on the

particular section of Miro Street.

·

He noted that only a small percentage of people had gone to the

consultation meeting.

·

He wanted the street to be kept two way. He also asked

that a 30km speed limit be installed or speed humps introduced on the street.

He had spoken to about 12 residents on Miro Street.

·

He asked that Council not accept the recommendation in the

report.

|

4 Acceptance

of late items

Nil

5 Confidential

business to be transferred into the open

Nil

6 Change

to the order of business

The Chair advised that supplementary agenda item 11.1: Draft

Annual Plan would be addressed before item 11.5: User Fees and Charges report.

7 Confirmation

of minutes

|

7.1 Minutes of

the Council meeting held on 16 December 2025

|

|

Resolution CO/26/2/1

Moved: Cr

Hēmi Rolleston

Seconded: Cr Glen

Crowther

That the Minutes

of the Council meeting held on 16 December 2025 be confirmed as a true and

correct record subject to a correction to item 11.9, Regulatory Hearings

Panel Term and Appointment Process, to amend the date in resolutions b)

and c) to 24 March, not 3 April as previously resolved.

Carried

|

8 Declaration

of conflicts of interest

Nil

9 Deputations,

presentations, petitions

Nil

10 Recommendations

from other committees

Nil

11 Business

Timestamp: 35 minutes

|

11.1 Local Water Done Well -

Options for Stormwater

|

|

Staff Christine

Jones, General Manager Strategy, Partnerships & Growth

Charles

Lane, Team Leader: Commercial Legal

Stephen

Burton, Transformation Lead – Water Services

Frazer

Smith, Manager: Strategic Finance & Growth

Cathy

Davidson, Water Organisation Establishment Lead

Wally

Potts, Head of City Waters

At 11.11am the meeting adjourned.

At 11.22am the meeting resumed in open.

|

|

motion

Moved: Cr

Marten Rozeboom

Seconded: Cr Kevin Schuler

That the Council:

(a) Receives

the report "Local Water Done Well - Options for Stormwater".

(b) Approves maintaining an

integrated approach for the responsibility and delivery of stormwater, water

supply and wastewater, i.e. a single organisation will both hold

responsibility and provide service delivery for all three water functions.

(c) Notes that if, following

consideration of due diligence matters, Council continues to establish a

multi-council Water Organisation with Western Bay of Plenty District Council,

this will result in the responsibility for, and delivery of, stormwater

services transferring to the Water Organisation along with water supply and

wastewater.

(d) Approves that Council’s

general approach will be for Tauranga City Council to retain ownership of

land used for stormwater purposes, regardless of whether this land is subject

to the Reserves Act 1977 and regardless of whether a Water Organisation is

established.

(e) Notes that if a Water

Organisation is established, exceptions to retention of land ownership can be

considered by Council on a case-by-case basis.

(f) Approves that

Council’s general approach is that the Water Service Provider for

stormwater shall own stormwater ‘hard’ infrastructure assets,

such as all pipes, pumps, dams, inlets and outlets etc.

(g) Notes that Council may choose

to influence stormwater charging by a Water Organisation via foundation

documents (the Constitution and Shareholders Agreement).

AN AMENDMENT WAS

PROPOSED:

Moved: Cr

Hautapu Baker

Seconded: Cr

Steve Morris

That the Council:

Replace

recommendation (g) with the following:

(g) Supports the inclusion of a

‘carve out’ in the founding documents and that Council discusses

with the other partners the ability for Tauranga City Council elected members

to directly set stormwater charges for its residents.

|

|

For: Mayor

Mahé Drysdale, Deputy Mayor Jen Scoular, Cr Hautapu Baker, Cr Glen Crowther,

Cr Rick Curach, Cr Steve Morris, Cr Hēmi Rolleston, Cr Kevin Schuler and

Cr Rod Taylor

Against: Cr

Marten Rozeboom

cARRIED 9/1

|

|

At 12.38pm the meeting adjourned.

At 1.49pm the meeting resumed in open.

A FURTHER AMENDMENT WAS PROPOSED

|

|

Moved: Cr

Steve Morris

Seconded: Cr Hautapu

Baker

That the Council:

(h)

Notes that Council may consider a pass‑through model

whereby the Water Organisation

invoices Tauranga City Council for stormwater services and Council recovers

those costs via targeted rates. Requests the Chief Executive to report back with

issues and options, including compliance with the Local Government (Water Services)

Act 2025, affordability and equity impacts, and mechanisms to avoid double‑charging.

For: Mayor

Mahé Drysdale, Deputy Mayor Jen Scoular, Cr Hautapu Baker, Cr Glen Crowther,

Cr Rick Curach, Cr Steve Morris, Cr Kevin Schuler and Cr Rod Taylor

Against: Cr Hēmi Rolleston

and Cr Marten Rozeboom

CARRIED 8/2

The substantive motion was taken in parts.

|

|

Resolution CO/26/2/3

Moved: Cr

Marten Rozeboom

Seconded: Cr Kevin Schuler

Part 1

That the Council:

(a) Receives the report

"Local Water Done Well - Options for Stormwater".

(d) Approves that Council’s

general approach will be for Tauranga City Council to retain ownership of

land used for stormwater purposes, regardless of whether this land is subject

to the Reserves Act 1977 and regardless of whether a Water Organisation is

established.

(e) Notes that if a Water

Organisation is established, exceptions to retention of land ownership can be

considered by Council on a case-by-case basis.

(g) Supports the inclusion of a

‘carve out’ in the founding documents and that Council discusses

with the other partners the ability for TCC elected members to directly

set stormwater charges for its residents.

(h)

Notes that Council may consider a pass‑through model

whereby the Water Organisation

invoices Tauranga City Council for stormwater services and Council recovers

those costs via targeted rates. Requests the Chief Executive to report back with

issues and options, including compliance with the Local Government (Water Services)

Act 2025, affordability and equity impacts, and mechanisms to avoid double‑charging.

For: Mayor

Mahé Drysdale, Deputy Mayor Jen Scoular, Cr Hautapu Baker, Cr Rick

Curach, Cr Steve Morris, Cr Marten Rozeboom, Cr Kevin Schuler and Cr Rod

Taylor

Against: Cr

Glen Crowther, Cr Hēmi Rolleston

CARRIED 8/2

Part 2

That the Council:

(b) Approves maintaining an

integrated approach for the responsibility and delivery of stormwater, water

supply and wastewater, i.e. a single organisation will both hold

responsibility and provide service delivery for all three water functions.

(c) Notes that if, following

consideration of due diligence matters, Council continues to establish a

multi-council Water Organisation with Western Bay of Plenty District Council,

this will result in the responsibility for, and delivery of, stormwater

services transferring to the Water Organisation along with water supply and

wastewater.

For: Mayor

Mahé Drysdale, Cr Hautapu Baker,Cr Steve Morris, Cr Marten Rozeboom,

Cr Kevin Schuler and Cr Rod Taylor

Against: Deputy

Mayor Jen Scoular, Cr Glen Crowther, Cr Rick Curach and Cr Hēmi

Rolleston

CARRIED 6/4

Part 3

That the Council

(f) Approves that

Council’s general approach is that the Water Service Provider for

stormwater shall own stormwater ‘hard’ infrastructure assets,

such as all pipes, pumps, dams, inlets and outlets etc.

For: Mayor

Mahé Drysdale, Cr Hautapu Baker, Cr Glen Crowther,Cr Steve Morris, Cr

Hēmi Rolleston,

Cr Marten Rozeboom, Cr Kevin Schuler and Cr Rod Taylor

Against: Deputy

Mayor Jen Scoular, Cr Rick Curach

Carried 8/2

|

Timestamp: 4 hours and 44

minutes

|

11.2 Submission on Planning

Bill and Natural Environment Bill

|

|

Staff Andrew

Mead, Head of City Planning & Growth

Janine

Speedy, Team Leader: City Planning

Carl

Lucca, Team Leader, Structure Planning

At 2.15pm, Cr Hautapu Baker withdrew from the meeting.

Action requested

·

That staff receive feedback from Te Rangapū on their views

on the submission.

|

|

Resolution CO/26/2/4

Moved: Cr

Steve Morris

Seconded: Cr Marten Rozeboom

That the Council:

(a) Receives the report

"Submission on Planning Bill and Natural Environment Bill".

(b) Endorse the key submission

points included as Attachment 1 on the Planning Bill and Natural Environment

Bill to be included in a detailed submission to the Select Committee.

(c) Delegates to the Chief

Executive to approve the submission on the Planning Bill and Natural

Environment Bill to the Select Committee.

Carried

Cr Hautapu Baker was not present

for the vote on this item.

|

Timestamp 4 hours and 58 minutes

|

11.3 Draft Submission on

Simplifying Local Government proposal

|

|

Staff Jeremy

Boase, Head of Strategy, Governance & Climate Resilience

Action requested:

·

That staff engage with Te Rangapū and iwi chairs on the

submission on Simplifying Local Government.

At 2.41pm, Cr Hautapu Baker re-entered the meeting.

|

|

Resolution CO/26/2/5

Moved: Cr

Rod Taylor

Seconded: Cr Marten Rozeboom

That the Council:

(a) Receives the report

"Draft submission on Simplifying Local Government proposal".

(b) Approves the draft submission

“Tauranga City Council Submission – Simplifying Local Government

draft proposal” included as Attachment 1 to this report.

(c) Delegates authority to the

General Manager: Strategy, Partnerships & Growth to make minor drafting,

typographical, and presentation amendments as required prior to formally

lodging the submission ahead of the 20 February 2026 deadline.

(d) Delegates authority to the City

Future committee to approve the submission, if following discussion,

changes are more than minor.

Carried

|

Timestamp 5 hours and 19 minutes

|

11.4 Rates Capping Submission

|

|

Staff Jeremy

Boase, Head of Strategy, Governance & Climate Resilience

|

|

Resolution CO/26/2/6

Moved: Mayor

Mahé Drysdale

Seconded: Cr Kevin Schuler

That the Council:

(a) Receives the report

"Rates Capping Submission".

(b) Retrospectively endorses

Council’s submission to the Department of Internal Affairs on the

government’s rate capping proposal, included as Attachment 1.

Carried

|

Timestamp: 5 hours and 21 minutes

|

11.9 Draft Annual Plan

2026/27

|

|

Staff Craig

Rice, Chief Operating & Financial Officer

Christine

Jones, General Manager, Strategy, Partnerships & Growth

Tracey

Hughes, Manager: Organisational Financial Performance & Corporate

Planning

Susan

Braid, Finance Lead Capital Performance & Community Investment

Jeremy

Boase, Head of Strategy, Governance & Climate Resilience

Action requested:

·

That staff look at opex savings before any levels of service

changes.

|

|

The motions were taken in parts.

Part 1

|

|

Resolution CO/26/2/7

Moved: Mayor

Mahé Drysdale

Seconded: Deputy Mayor Jen Scoular

That the Council:

(a) Receives the report "Draft

Annual Plan 2026/27".

(b) Notes the maximum limit on

rates increase for Year 3 of the 2024-34 Long Term Plan (LTP) was 12% net of

growth and the rates increase net of growth for 2027 was 10.4%.

(c) Asks for a draft budget with

options of 7.5% rates increase net of growth, after separating three waters

rates and charges:

(i) Set the capital

programme, of $450m including carry forwards and contingency. The projects

and contingency to be reported separately.

Carried

Extension of Meeting Time

|

|

Resolution CO/26/2/8

Moved: Cr

Marten Rozeboom

Seconded: Cr Kevin Schuler

That the Council meeting extends beyond six hours.

Carried

Part 2

|

|

Resolution CO/26/2/9

Moved: Mayor

Mahé Drysdale

Seconded: Cr Kevin Schuler

That the Council:

(c) Asks for a draft budget with

options of 7.5% rates increase net of growth, after separating three waters

rates and charges:

(ii) A reduction in operational

expenditure from Attachment 1 and Confidential Attachment 2

of $2.7M.

(iii) Additional savings target

across the organisation of $1.6M, noting the details of this are to be found

by the executive prior to the final budget.

(iv) Reductions

in charges under the waste collection rate of $1.3M of revenue to reflect

budgeted costs of delivering this service.

Carried

Part 3

|

|

Resolution CO/26/2/10

Moved: Mayor

Mahé Drysdale

Seconded: Cr Rod Taylor

That

the Council:

(c) Asks for a draft budget with

options of 7.5% rates increase net of growth, after separating three waters

rates and charges:

(v) Increase

in user fee revenue by $0.3M from applying 3% inflation rather than 2.3%

annual inflation that was assumed in the draft budget.

Carried

|

|

Part 4

|

|

Resolution CO/26/2/11

Moved: Mayor

Mahé Drysdale

Seconded: Deputy Mayor Jen Scoular

That the Council:

(d) Notes there are potential

additional savings for next year’s rates as a result of lower capital

delivery in 2025/26 leading to lower debt. This depends on the level of

carry forward budget approved with potential savings of $1 to $2m in interest

costs for 2026/27. Provide a clear calculation of interest and

depreciation for both years.

Carried

Part 5

|

|

Resolution CO/26/2/12

Moved: Mayor

Mahé Drysdale

Seconded: Cr Kevin Schuler

That the Council:

(e) Agrees the service provision

that council would consider for expenditure reduction to achieve rates

saving, noting an overall reduction in rates funded expenditure of $4.5 to

$5.3m would be required to achieve a rates increase of 7.5%, from the options

provided in Confidential Attachment 3 (with the three waters

activities separately disclosed).

Carried

Part 6

|

|

Resolution CO/26/2/13

Moved: Mayor

Mahé Drysdale

Seconded: Deputy Mayor Jen Scoular

That the Council:

(f) Requests details of the

budget adjustments required by resolution in all of the above be provided at

the April Council meeting for final decision-making.

Carried

Part 7

|

|

Resolution CO/26/2/14

Moved: Cr

Steve Morris

Seconded: Deputy Mayor Jen Scoular

That the Council:

(g) Provides all reporting in

three columns, excluding waters, waters and total at a detailed level.

Carried

Part 8

|

|

Resolution CO/26/2/15

Moved: Cr

Rick Curach

Seconded: Cr Rod Taylor

That the Council:

(h) Adopts

“option 1: do not consult” approach to consultation for the

annual plan 2026/27, assuming level of service

changes contemplated by resolution (e) are not significant in

terms of the Local Government Act 2002.

For: Mayor

Mahé Drysdale, Deputy Mayor Jen Scoular, Cr Hautapu Baker, Cr Rick

Curach, Cr Steve Morris, Cr Hēmi Rolleston, Cr Marten Rozeboom, Cr

Kevin Schuler and Cr Rod Taylor

Against: Cr Glen Crowther

CARRIED

9/1

(i) Undertakes

community engagement on the draft annual plan, and in anticipation of

the long-term plan,

include a demographically-sound and independent survey, by direct appointment

of the same supplier as the annual plan 2025/26, with 1000 respondents

(j) Attachments

2 and 3 can be transferred into the open once the annual plan has been adopted.

CARRIED

|

At 4.19pm the meeting adjourned.

At 4.30pm the meeting resumed in open.

Timestamp: 7 hours and 14 minutes

|

11.5 User Fees and Charges

Review - Issues and Options

|

|

Staff Christine

Jones, General Manager, Strategy, Partnerships & Growth

Actions requested

That staff:

·

Provide options regarding the crematorium fees for the 24 March

Council meeting.

·

For future reports leave the Te Ao section in the report and

add a statement.

|

|

Resolution CO/26/2/16

Moved: Mayor

Mahé Drysdale

Seconded: Cr Marten Rozeboom

That the Council:

(a) Receives the report "User

Fees and Charges Review - Issues and Options".

(b) Notes the work done to date

on the user fees and charges review by staff and elected members and agrees

to defer further progress on all aspects of the review until the long-term

plan process which will be progressed during 2026.

Carried

|

Timestamp: 7 hours and 24 minutes

|

11.6 Transport Resolutions

Report No.59

|

|

Staff Mike

Seabourne, Head of Transport

Shawn

Geard, Manager: Transport System

|

|

Resolution CO/26/2/17

Moved: Cr

Rod Taylor

Seconded: Cr Marten Rozeboom

That the Council:

(a) Receives the report

"Transport Resolutions Report No.59".

(b) Resolves

to implement the proposed traffic and parking controls for general safety,

operational, or amenity purposes as detailed in Attachment A -

including Attachment 7.1, 7.2, 7.7, 7.8,7.9,7.16, 7.21, 7.25

(c) That

these changes take effect on or after 11 February 2026, subject to the

installation of appropriate signs and road markings where necessary.

Carried

|

Timestamp: 7 hours and 32 minutes

|

11.7 Bay of Plenty Mayoral

Forum Triennial Agreement 2025-2028

|

|

Staff Jeremy

Boase, Head of Strategy, Governance & Climate Resiliance

|

|

Resolution CO/26/2/18

Moved: Mayor

Mahé Drysdale

Seconded: Cr Glen Crowther

That the

Council:

(a) Receives the report "Bay

of Plenty Mayoral Forum Triennial Agreement 2025-2028".

(b) Endorses the draft Bay of

Plenty Mayoral Forum Triennial Agreement 2025-2028, included as Attachment 1.

(c) Endorses the draft Bay of

Plenty Mayoral Forum Terms of Reference, included as Attachment 2.

(d) Authorises the Mayor to sign

the Triennial Agreement on behalf of Tauranga City Council.

(e) Supports a review of the

Triennial Agreement commencing no later than six months after it is signed to

ensure that it remains relevant given ongoing government reforms of the local

government sector, and requests that the Mayor formally communicate this to

the other signatories.

Carried

|

Timestamp: 7 hours and 41 minutes

|

11.8 Miro Street Parking

Improvements

|

|

Staff Mike

Seabourne, Head of Transport

Shawn

Geard, Manager: Transport System

Action requested

·

That staff provide a regular report on which transport projects

might be uplifted for additional savings.

The motion was taken in parts.

|

|

Resolution CO/26/2/19

Moved: Deputy

Mayor Jen Scoular

Seconded: Cr Kevin Schuler

Part 1

That the Council:

(a) Receives the report

"Miro Street Parking Improvements".

(b) Endorses converting Miro

Street (between Matai Street and Hinau Street) to a One-Way-Street with

angled parking to improve parking for residents of Miro Street at the cost of

up to $315,000.

(d) That the potential expansion

of the one-way system to northern section of Miro Street and Tawa Street is

planned as a future stage in the next LTP.

(e) That

the estimated saving against budget of $735,000, is re-prioritised to deliver

rapidly deployable projects, in accordance with City Delivery Committee

Resolution CDC/25/0/7 (recommendation (e) of the report “Transport

Minor Safety and Accessibility Prioritisation and Programme Status”

from 15 December 2025).

CARRIED

Part 2

That the Council:

(c) Constructs a footpath on the

eastern side of Miro Street between Matai Street and Hinau Street to both

improve accessibility for the angled carparking and also to mitigate any

continued berm parking issues – without formally banning berm parking

at this time at the cost of up to $150,000.

For: Mayor

Mahé Drysdale, Deputy Mayor Jen Scoular, Cr Hautapu Baker, Cr Marten Rozeboom,

Cr Kevin Schuler and Cr Rod Taylor

Against: Cr

Glen Crowther, Cr Rick Curach, Cr Steve Morris and Cr Hēmi Rolleston

CARRIED 6/4

|

12 Discussion

of late items

Nil

13 Public

excluded session

Resolution to exclude the public

|

Resolution CO/26/2/20

Moved: Deputy

Mayor Jen Scoular

Seconded: Cr Marten Rozeboom

That the public be excluded from the following parts of

the proceedings of this meeting at 5.24pm.

The general subject matter of each matter to be considered

while the public is excluded, the reason for passing this resolution in

relation to each matter, and the specific grounds under section 48 of the

Local Government Official Information and Meetings Act 1987 for the passing

of this resolution are as follows:

|

General

subject of each matter to be considered

|

Reason for

passing this resolution in relation to each matter

|

Ground(s)

under section 48 for the passing of this resolution

|

|

13.1 -

Public Excluded Minutes of the Council meeting held on 26 August 2025

|

s6(b) - The making

available of the information would be likely to endanger the safety of any

person

s7(2)(a) - The

withholding of the information is necessary to protect the privacy of

natural persons, including that of deceased natural persons

s7(2)(b)(ii) - The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information

s7(2)(g) - The

withholding of the information is necessary to maintain legal professional

privilege

s7(2)(h) - The

withholding of the information is necessary to enable Council to carry out,

without prejudice or disadvantage, commercial activities

s7(2)(i) - The

withholding of the information is necessary to enable Council to carry on,

without prejudice or disadvantage, negotiations (including commercial and

industrial negotiations)

|

s48(1)(a) - the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

13.2 -

Public Excluded Minutes of the Council meeting held on 16 September 2025

|

s7(2)(h) - The

withholding of the information is necessary to enable Council to carry out,

without prejudice or disadvantage, commercial activities

s7(2)(i) - The

withholding of the information is necessary to enable Council to carry on,

without prejudice or disadvantage, negotiations (including commercial and

industrial negotiations)

|

s48(1)(a) - the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

13.3 -

Public Excluded Minutes of the Council meeting held on 29 October 2025

|

s7(2)(b)(ii) - The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information

s7(2)(h) - The

withholding of the information is necessary to enable Council to carry out,

without prejudice or disadvantage, commercial activities

s7(2)(i) - The

withholding of the information is necessary to enable Council to carry on,

without prejudice or disadvantage, negotiations (including commercial and

industrial negotiations)

|

s48(1)(a) - the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

13.4 -

Public Excluded Minutes of the Council meeting held on 16 December 2025

|

s6(b) - The making

available of the information would be likely to endanger the safety of any

person

s7(2)(a) - The

withholding of the information is necessary to protect the privacy of

natural persons, including that of deceased natural persons

s7(2)(b)(ii) - The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information

s7(2)(d) - The

withholding of the information is necessary to avoid prejudice to measures

protecting the health or safety of members of the public

s7(2)(g) - The

withholding of the information is necessary to maintain legal professional

privilege

s7(2)(h) - The

withholding of the information is necessary to enable Council to carry out,

without prejudice or disadvantage, commercial activities

s7(2)(i) - The

withholding of the information is necessary to enable Council to carry on,

without prejudice or disadvantage, negotiations (including commercial and

industrial negotiations)

|

s48(1)(a) - the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

13.5 -

Council-Controlled Organisations - Board Appointments beyond 30 June 2026

|

s7(2)(a) - The

withholding of the information is necessary to protect the privacy of

natural persons, including that of deceased natural persons

|

s48(1)(a) - the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

Confidential

Attachment 2 - 11.1 - Draft Annual Plan 2026/27

|

s7(2)(a) - The

withholding of the information is necessary to protect the privacy of

natural persons, including that of deceased natural persons

s7(2)(b)(ii) - The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information

|

s48(1)(a) the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

|

Confidential

Attachment 3 - 11.1 - Draft Annual Plan 2026/27

|

s7(2)(a) - The

withholding of the information is necessary to protect the privacy of

natural persons, including that of deceased natural persons

s7(2)(b)(ii) - The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information

|

s48(1)(a) the public

conduct of the relevant part of the proceedings of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding would exist under section 6 or section 7

|

Carried

|

The meeting resumed in open at 6.13pm.

14 Closing

karakia

Cr Rolleston closed the meeting with a karakia.

The meeting closed at 6.13 pm

The minutes of this meeting were confirmed as a true and

correct record at the Ordinary Council meeting held on 24 March 2026.

|

Ordinary Council meeting Agenda

|

24 March 2026

|

11 Business

11.1 Local

Water Done Well - Project Update

File

Number: A19779936

Author: Cathy

Davidson, Manager: Directorate Services

Fiona Nalder,

Principal Strategic Advisor

Authoriser: Christine

Jones, General Manager: Strategy, Partnerships & Growth

Please

note that this report contains confidential attachments.

|

Public Excluded Attachment

|

Reason why Public Excluded

|

|

Item 11.1 - Local Water

Done Well - Project Update - Attachment 1 - Detailed Budget Information

|

s7(2)(a) - The

withholding of the information is necessary to protect the privacy of natural

persons, including that of deceased natural persons.

s7(2)(i) - The

withholding of the information is necessary to enable Council to carry on,

without prejudice or disadvantage, negotiations (including commercial and

industrial negotiations).

|

Purpose of the Report

1. To provide an update of

the following project matters – the establishment budget (the budget up

until 1 July 2027), digital programme, recruitment of a Chief Executive, name

and identity development, and key milestones for the project post-April 2026,

and to seek approval for the overarching principle of maintaining or bettering

current Tangata Whenua arrangements.

|

Recommendations

That the Council:

(a) Receives the report

"Local Water Done Well - Project Update".

(b) Notes that future project

updates will be provided via the quarterly reporting against the Water

Services Delivery Plan (beginning April 2026) to the Department of Internal

Affairs.

(c) Adopts the principle of

maintaining Tangata Whenua participation, engagement and arrangements, with

existing commitments and practices either retained or bettered during, and

following, the transition to a Water Organisation.

(d) Notes the future key

milestones in this report, and the list of topics scheduled for consideration

and further work post-April 2026 as provided by Attachment 3.

(e) Attachment 1 can be

transferred into the open following negotiations with suppliers.

|

Executive Summary

2. Tauranga

City Council (Council), in partnership with Western Bay of Plenty District

Council (WBOPDC), is progressing the establishment of a multi‑council

Water Organisation (WO) as part of the Government’s Local Water Done Well

(LWDW) reform programme.

3. The

WO is scheduled to ‘go live’ on 1 July 2027, and this report

provides an update on key components required to support that transition. These

include the establishment budget, progress of the digital programme,

recruitment of the Establishment Chief Executive and Board, development of the

organisation’s name and identity, key project milestones following April

2026, and the Te Ao Māori approach underpinning the work.

4. This

report is one of four reports being presented to Council on 24 March 2026

addressing Local Water Done Well matters, and should be considered alongside

the three companion reports addressing commercial terms, due diligence and the

financial implications of establishing a WO.

Establishment budget

5. Council’s

share of the combined establishment and digital budget for the WO (leading up

until July 2027) is provided in Table 1 below. Further details are provided by

confidential Attachment 1.

Table

1: Original approved budget versus revised budget projection

|

|

Original Budget

|

TCC Current Budget

|

TCC Updated Projection

|

|

TOTAL

|

$9,464,000

|

$8,638,776

|

$8,527,945

|

|

Projected Saving

|

$110,831

|

Digital programme

6. The

digital programme, a partnership with IAWAI and WBOPDC, has two major phases.

7. Phase

1, approved in December 2025, focuses on achieving exit from Watercare by

October 2026 and establishing standalone asset, work order, and GIS systems for

all three partner organisations. Infor is the lead technology provider and key

contractual arrangements are in place.

8. Phase

2, commencing following Council’s decision on 2 April 2026, will

establish the full suite of organisational systems for the future WO. This will

include consideration of billing, finance, customer, regulatory, and HR/payroll

functions. An estimated amount for Council’s share of the proposed

investment for Phase 2 is included in the draft Annual Plan. A business case

and commercial proposal will be presented to Council in June 2026, and this

will also seek approval of Phase 2 budget requirements.

9. No

financial details are provided within this open report due to commercial

sensitivity (Phase 1) and to protect Council’s negotiation position

(Phase 2).

Recruitment

10. Recruitment

for the Establishment Chief Executive is well advanced, with interviews

underway and a preferred candidate expected to be appointed in April 2026,

should Council confirm establishment of the WO. Recruitment of the Chair and

Board will follow shortly thereafter.

Name and identity for the WO

11. Work

is also underway to develop a proposed name and identity for the WO. This will

be undertaken collaboratively with the Joint Working Group, comprising elected

members and Tangata Whenua representatives (with wider Tangata Whenua

involvement), to ensure cultural integrity, clarity of purpose, legal

suitability, and long‑term applicability.

Work post-April 2026

12. Key

milestones after April 2026 include recruitment, development of the Transfer

Agreement, development of the Statement of Expectations, progression of

organisational policies and strategies, and ongoing reporting to the Department

of Internal Affairs, together with list of topics for further consideration and

work as identified by the Joint Working Group.

13. Following

the 2 April decision, it is intended to move from the current Joint Working

Group to a Joint Committee, and a new terms of reference will be developed for

the Committee and brought to Council.

Te Ao Māori

14. A

strong Te Ao Māori approach remains central to the project. Tangata Whenua

representatives sit alongside Councillors on the Joint Working Group, guiding

the development of recommendations. This report seeks Council endorsement of

the principle that existing Tangata Whenua engagement arrangements will be

maintained or bettered through, and after, the transition to a WO. Further

work, such as developing engagement and remuneration policies, will occur after

April 2026. It is proposed that Tangata Whenua will sit on the future Joint

Committee, together with Councillors.

Background

15. Tauranga

City Council (Council), in partnership with Western Bay of Plenty District

Council (WBOPDC, is progressing the establishment of a Multi-Council Water

Organisation (WO) in response to the Government’s Local Water Done Well

(LWDW) reform programme. The WO has a ‘go live’ date of 1 July

2027.

16. On

15 August 2026 Council passed resolutions (CO/25/0/22) requesting:

· a

project plan for the establishment of the proposed water organisation.

· quarterly

reports to Council on engagement, progress against the project plan, work

completed in the previous quarter and work proposed for the upcoming quarter,

including budget tracking and risks.

17. Council

endorsed the Multi-Council Water Organisation Summary Plan (including Due

Diligence) on 29 October 2025. This plan sets out the approved approach to

complete the necessary steps to establish the WO. It was prepared based on the

Commitment Agreement between the two councils and the approved Water Service

Delivery Plans (WSDP).

18. Since

October Council has received the following reports progressing the

establishment of the proposed WO

· 16

December 2025 – Project Update and Recruitment

· 16

December 2025 – Digital Programme

· 10

February 2026 – Options for Stormwater

19. This

project update is being presented to Council on 24 March 2026 alongside three

additional Local Water Done Well reports covering the proposed commercial

terms, the financial implications of establishing a WO, and the due diligence

findings. These four reports, when considered holistically, progress

establishment work and provide a comprehensive project update on the work

completed to establish the WO.

20. The

matters covered by this report are:

· Establishment

budget (the budget up until 1 July 2027)

· Digital

programme

· Recruitment

of a Chief Executive

· Name

and identity development

· Key

milestones for the project post-April 2026

· Te

Ao Māori approach

Establishment budget

21. Council’s

share of the combined establishment and digital budget for the WO (leading up

until July 2027) is provided in Table 1 below. Further details are provided by

Confidential Attachment 1.

Table

1: Original approved budget versus revised budget projection

|

|

Original Budget

|

TCC Current Budget

|

TCC Updated Projection

|

|

TOTAL

|

$9,464,000*

|

$8,638,776

|

$8,527,945

|

|

Projected Saving

|

$110,831

|

* Establishment plus Phase 1

Digital

22. Budget

sharing arrangements between Council and WBOPDC are set out by the Commitment

Agreement.

23. People

and workforce considerations are discussed in more detail in the companion

Local Water Done Well – Due Diligence report. The two councils (TCC and

WBOPDC) will work together with the WO to transfer staff to suitably similar

roles in the WO and, where necessary, will look to minimise redundancy costs

through a sinking lid approach. Overall, it will be important to the success of

the WO to retain skilled staff and existing organisational knowledge.

24. All

budgets, establishment and digital, are debt funded opex and will be

transferred to the proposed WO.

Digital programme

25. Note:

no financial detail (approved budgets or future estimated funding requirements)

is included in this section due to commercial sensitivity and to protect

Council’s negotiation position.

26. The

Local Water Done Well Digital programme has two phases:

· Phase

1 - exit from Watercare by October 2026

· Phase

2 – establish digital services for the proposed WO by on 1 July 2027

Phase 1

– exit from Watercare

27. Phase

1 was approved by Council in December 2026 and is being delivered in

partnership with WBOPDC and IAWAI, delivering significant cost savings for all

three parties. Infor has been selected as the technology provider and costs are

being shared by the three parties (IAWAI 50%, Council/TCC 35%, WBOPDC 15%). A

Joint Project Agreement governs cost sharing, procurement and management of

Phase 1.

28. Phase

1 will deliver standalone Asset and Work Order Management capabilities for all

three organisations, alongside integration with Council’s existing GIS

capabilities. A new GIS capability will also be established for IAWAI as part

of the programme.

29. Phase

1 is on track for completion by the end of October 2026. Contractual agreements

with all key providers have been signed or are close to execution, including

Infor, Ernst & Young (data migration), Watercare, and Downer.

Phase 2 – standing up of WO capabilities

30. Delivery

of Phase 2 will commence following Council’s decision whether to continue

with the establishment of a WO (due 2 April 2026). The scope of Phase 2 will

consider billing, finance, customer, regulatory, and HR & payroll systems

and processes and full IT architecture requirements will be considered against

what services will continue to be provided by Council in the short term.

31. If

Council decides to proceed with establishment of a WO, commercial negotiations

with delivery vendors will commence in April, and a business case will be

presented for Council consideration in June 2026. The current partnership

approach with WBOPDC and IAWAI is proposed to continue for Phase 2. An estimate

of Council’s share for the proposed investment in Phase 2 is included in

the draft Annual Plan, and this will be brought to Council for approval in June

2026 along with the business case.

Recruitment of an Establishment Chief Executive and Board

of Directors

32. On 16 December 2025 Council

approved the recruitment and appointment of a WO Establishment Chief Executive

(CO/25/0/6).

33. Several strong applicants

applied for the position. Shortlisting has been completed and the interview

process began on 13 March 2026. If Council decides to proceed with

establishment of the WO on 2 April 2026, an accompanying 2 April Council report

will seek approval to make a formal offer to the preferred candidate. This will

initially be on a 2-year fixed term basis, with the potential for the

appointment to become an ongoing arrangement.

34. The appointed Chief Executive

will commence in the role depending on availability (mid-2026 at the latest).

35. Following the 2 April decision,

it is recommended that recruitment commence for the Board of Directors of the

WO. Recruitment will initially focus on appointing a Chair and two Board

members, with the remainder of the Board to be appointed in advance of the 1

July 2027 ‘go live’ date. A Council paper seeking approval to

recruit the Board is scheduled for 21 April 2026.

Developing the name and identity for the proposed Water

Organisation

36. A high-level project outlining

the process for development a name and identity for the proposed WO is provided

as Attachment 2. The objective is to develop and adopt a name for the proposed

WO ahead of incorporation, so that the chosen name is used in legal

documentation establishing the WO.

37. The proposed name will be

brought to Council for approval.

38. The recommended approach is to

work with the members of the Joint Working Group (includes elected members from

Council and WBOPDC, and Tangata Whenua representatives) to develop a proposed

name. Council staff and wider Tangata Whenua involvement is also

proposed. A full brand development process is not proposed, as this is

intended to occur later to enable the participation of the WO Chair and Board,

and the WO Chief Executive.

39. The following key requirements

have been identified.

· Clear

connection to purpose – the name should make it apparent that the

organisation is focussed on the delivery of water services and values

environmental stewardship.

· Geographic

relevance and identity, whilst also future-proofed so that other councils can

join later.

· Memorable,

simple and easy to use.

· Offer

longevity, flexibility and legal practicality.

· Be

culturally appropriate and recognise partnership (potentially bilingual).

· Differentiation

from competitors.

· Trademarked,

the identity/name/brand is owned by the WO.

Key milestones - post-April 2026

40. Work has commenced on

developing a project plan for post-April, based on the assumption that Council

will continue towards establishment of a multi-council WO. The following are

high-level milestones.

· First

report on implementation of the Water Services Delivery Plan due to the

Department of Internal Affairs in April 2026

· Appoint

Chief Executive in April 2026 (subject to Council decision, 2 April 2026),

commence recruitment of executive management roles from May 2026.

· Commence

recruitment of a Chair and partial Board in April 2026

· Commence

development of a Transfer Agreement in April 2026 (must be in place for

‘go live’ date of 2 July 2027).

· Develop

a Statement of Expectations, April to December 2026

· Establish

staff pathways for transition to the WO, commencing April 2026

· Develop

an operations focussed transition plan, commencing April 2026

· Return

to Council with a Phase 2 digital business case in June 2026

· Commence

development of a Water Services Strategy in July 2026

· ‘Go

live’ date for multi-council WO is 1 July 2027.

41. In addition to the high-level

milestones above, the Joint Working Group (a group consisting of elected

members from Council and WBOPDC, and Tangata Whenua representatives) has

identified issues and work to be progressed post-April 2026. These are provided

in Attachment 3 and will be considered and incorporated into future work

programmes as appropriate.

TE AO MĀORI APPROACH

42. Council

is working in partnership with Tangata Whenua on the establishment of the

proposed WO, ensuring that Council’s Te Ao Māori principles are

considered and integrated into project work. Tangata Whenua were invited to

select representatives to work alongside elected members to represent the

interests of all Iwi, Hapū, Māori entities, tāngata whenua

forums and whenua Māori trusts.

43. Tangata

Whenua appointed the following representatives:

· Hakopa

Tapiata

· Kiritapu

Allan

· Kylie

Smallman

· Roana

Bennett

· Rohario

Murray

· Shadrach

Rolleston

44. These

representatives are members of the Joint Working Group, along with elected

members from Council and WBOPDC. The Joint Working Group has been considering a

range of work related to the establishment of the proposed WO and making

recommendations for decision-making by Council and WBOPDC.

45. A

stocktake of existing Tangata Whenua arrangements in place at Council and

WBOPDC was presented to the Joint Working Group on 23 February 2026 alongside a

suggested approach for transitioning existing arrangements to the WO. In

response, the Joint Working Group agreed to recommend to both Councils that

they:

· Adopt

the principle of maintaining Tangata Whenua participation, engagement and

arrangements, with existing commitments and practices either retained or

bettered during, and following, the transition to a Water Organisation.

· Agree

that developing a Tangata Whenua Engagement Policy and a Tangata Whenua

Remuneration Policy is to be a priority for the Water Organisation, and note

that this will be considered for inclusion in the Statement of Expectations.

· Agree

that the Water Organisation is to consider each existing arrangement (as

identified in each Council’s Tangata Whenua stocktake) and assess and

identify how they will be transferred across to Water Organisation, and note

that this will be considered for inclusion in the Statement of Expectations.

· Explore

the development of an overarching Tangata Whenua Framework, including strategic

guidance and input.

46. This

report presents the first recommendation above for Council consideration. The

remaining recommendations relate to work intended to occur post-April, once

Council has decided whether to proceed with establishment of a WO. These will

be addressed by future project plans and work programmes (refer also to

Attachment 2).

47. The

Council paper ‘Local Water Done Well – Commercial Terms’, a

companion paper to this report, presents a suite of Commercial Terms for

Council decision. In addition to various matters relating to the Shareholders,

Shareholding and the Board, it also recommends forming a Joint Committee which

includes Tangata Whenua, alongside elected members from Council and WBOPDC.

48. The

proposed Joint Committee will replace the Joint Working Group. Including

Tangata Whenua representatives enables their continued involvement in

governance discussions.

Statutory Context

49. The matters in this report form

part of Council’s overall response to the government’s Local Water

Done Well reform programme and associated legislation. There are no specific

statutory compliance matters to be considered in respect of this report.

STRATEGIC ALIGNMENT

50. Council’s overall

response to the Local Water Done Well reforms supports delivery of the

following community outcomes.

|

Contributes

|

|

We are an inclusive city

|

☐

|

|

We value, protect and enhance the environment

|

ü

|

|

We are a well-planned city that is easy to move

around

|

ü

|

|

We are a city that supports

business and education

|

☐

|

|

We are a vibrant city that embraces

events

|

☐

|

51. This report, and the wider

water reform programme, are part of ensuring Tauranga has water services that

are sustainable, affordable, well-planned and maintained, and of high quality.

Options Analysis

52. This

report seeks approval of the overarching principle of maintaining

Tangata Whenua participation, engagement and arrangements, with existing

commitments and practices either retained or bettered during, and following,

the transition to a WO, as recommended by the Joint Working Group

Option one: approve the overarching principle that

Tangata Whenua participation, engagement and arrangements will be maintained or

bettered during, and following, transition to a WO. (RECOMMEDED)

|

Advantages

|

Disadvantages

|

|

Supports the agreed

upon recommendation of the Joint Working Group.

Provides clarity for

Tangata Whenua regarding continuation of existing arrangements (with

opportunity to improve upon these over time).

Sets the WO up for

organisational success by setting a baseline for Tangata Whenua which follows

existing practices and arrangements.

Demonstrates Council

compliance with s81 of the Local Government Act 2002 (Contributions to

decision-making processes by Māori).

|

Sets the direction for

the WO ahead of appointing a Chief Executive, Chair and Board.

|

Option one: do not approve the overarching principle that

Tangata Whenua participation, engagement and arrangements will be maintained or

bettered during, and following, transition to a WO. (NOT RECOMMEDED)

|

Advantages

|

Disadvantages

|

|

Does not set direction

for the WO ahead of appointing a Chief Executive, Chair and Board, retaining

flexibility.

|

Does not support the

agreed upon recommendation of the Joint Working Group.

Prolongs uncertainty

for Tangata Whenua regarding the position of the WO.

May cause operational

difficulties for the WO, if key practices, arrangements, agreements and

policy positions are not maintained.

Requires alternative

arrangements to ensure compliance with s81 of the Local Government Act 2002

(Contributions to decision-making processes by Māori).

|

Financial Considerations

53. The financial implications of

establishing a WO are discussed in the accompanying 24 March 2026 Council

report ‘Local Water Done Well – Financial Implications’.

54. An update on establishment

costs is provided earlier in the report.

Legal Implications / Risks

55. The legal considerations

related to establishing a WO with WBOPDC are discussing in the accompanying 24

March 2026 Council report ‘Local Water Done Well – Commercial

Terms’. This paper presents recommended commercial terms for Council approval.

Once approved, and subject to Council’s final decision to proceed with

establishing a WO on 2 April 2026, these will inform the drafting of foundation

documents for the WO (e.g. the Constitution).

CLIMATE IMPACT

56. This report has no direct

climate impacts, however the proposed WO will enable an integrated sub-regional

approach to the management and delivery of water, wastewater and stormwater

services, providing opportunities for improved climate and environmental

outcomes over time.

Consultation / Engagement

57. Engagement regarding the option

of establishing a multi-council Water Organisation occurred alongside

Council’s 2025/2026 Annual Plan consultation process.

Significance

58. The Local Government Act 2002

requires an assessment of the significance of matters, issues, proposals and

decisions in this report against Council’s Significance and Engagement

Policy. Council acknowledges that in some instances a matter, issue,

proposal or decision may have a high degree of importance to individuals,

groups, or agencies affected by the report.

59. In making this assessment,

consideration has been given to the likely impact, and likely consequences for:

(a) the current

and future social, economic, environmental, or cultural well-being of the

district or region

(b) any persons who are likely to be

particularly affected by, or interested in, the decisions.

(c) the capacity of the local authority

to perform its role, and the financial and other costs of doing so.

60. In accordance with the

considerations above, criteria and thresholds in the policy, it is considered

that the decisions proposed by this report are of medium significance. The

recommendations are focused on enabling participation of Tangata Whenua, have minimal

cost implications, and propose an approach which is based on existing

arrangements.

61. The decision of whether to

proceed with establishment of a WO is of high significance and was consulted on

alongside the 2025/2026 Annual Plan. This decision will be brought to Council

on 2 April 2026, but will not require further consultation prior to decision-making.

ENGAGEMENT

62. Taking into consideration the

above assessment, that the decisions are of medium significance, officers are

of the opinion that no further engagement is required prior to Council making a

decision, noting that the required engagement has already occurred in 2025

(alongside consultation for the 2025/26 Annual Plan).

Next Steps

63. The next steps for this project

depend on Council decisions scheduled for 2 April 2026. If Council decides to

continue to establish a WO with WBOPDC, next steps will include:

· Seeking

Council approval to appoint the preferred candidate as the Establishment Chief

Executive for the WO.

· Seeking approval to initiate the

Board appointments.

· Establishing

the formal Joint Committee.

· Developing

a work programme through to 1 July 2027 to establish the WO and set it up for

success. This will include transition pathways for staff.

· Scoping

Phase 2 of the digital programme, ahead of bringing a proposal to Council for

consideration in June 2026.

· Commencing

work to develop key policies, processes and plans for the WO, including a

Tangata Whenua Engagement Policy and a Tangata Whenua Remuneration Policy,

alongside development of other required policies and plans such as a

Significance and Engagement Policy and the Water Services Strategy.

Attachments

1. Detailed

Budget Information - A19930973 - Public Excluded

2. Name

and identity development for Water Organisation - A19917686 ⇩

3. Items for

consideration and inclusion in forward work programme - A19917684 ⇩

|

Ordinary

Council meeting Agenda

|

24

March 2026

|

|

Ordinary

Council meeting Agenda

|

24

March 2026

|

|

Ordinary

Council meeting Agenda

|

24

March 2026

|

11.2 Local Water Done Well

- Commercial Terms

File

Number: A19713134

Author: Charles

Lane, Team Leader: Commercial Legal

Tyler Buckley,

Commercial Solicitor

Authoriser: Christine

Jones, General Manager: Strategy, Partnerships & Growth

Purpose of the Report

1. The purpose of this report is to present

recommendations of the Joint Working Group (comprised of representatives from

Tauranga City Council, Western Bay District Council and Tangata Whenua) on the

Commercial Term Sheet for consideration and final decision by Tauranga City

Council and Western Bay of Plenty District Council. Once agreed, the Commercial

Term Sheet will inform the drafting of the proposed Water Organisation’s

founding documents (the Shareholders’ Agreement and Constitution) under

the Local Waters Done Well framework.

|

Recommendations

That the Council:

(a) Receives the report

"Local Water Done Well - Commercial Terms" and Attachment 1.

(b) Approves and endorses the

Commercial Term Sheet at Attachment 1:

(i) With no exceptions; or

(ii) With the exception of

commercial term(s):

(1) [insert commercial term #]

(2) [insert commercial term #]

(c) Subject to a decision by both

Tauranga City Council and Western Bay of Plenty District Council to approve

the Local Water Done Well due diligence (proposed for 24 March 2026), and a

decision by both Tauranga City Council and Western Bay of Plenty District

Council to establish the Water Organisation (proposed for 2 April 2026):

(i) Tauranga City Council

and Western Bay of Plenty District Council shall work together in good faith

to resolve any outstanding commercial terms not yet approved by both Tauranga

City Council and Western Bay of Plenty District Council.

(ii) Notes that staff will

prepare the Water Organisation’s Shareholders’ Agreement and

Company Constitution:

(1) In a manner that is

consistent with the approved Commercial Term Sheet and any additional

commercial terms subsequently agreed by Tauranga City Council and Western Bay

of Plenty District Council; and

(2) To enable incorporation of

the Water Organisation by 1 July 2026, with operations commencing on 1 July

2027.

(d) In relation to whether

Tangata Whenua may hold Class A (voting) shares in the Water Organisation,

confirms that Class A (voting) shares in the Water Organisation may either:

(i) be held by Tangata

Whenua; or

(ii) be held only by shareholding

councils.

(e) Notes all parties on the

Joint Working Group have reached a consensus on all terms within the

Commercial Term Sheet at Attachment 1, with the exception of whether Tangata

Whenua should hold Class A (voting) shares in the Water Organisation

(f) Notes staff will report

back to Tauranga City Council and Western Bay of Plenty District Council in

relation to the draft Shareholders’ Agreement and Company Constitution

for the Water Organisation for endorsement and approval prior to execution by

the Mayor and Chief Executive.

|

Executive Summary

1. Tauranga City

Council (“TCC”) and Western Bay of Plenty District Council

(“WBOPDC”) are considering whether to establish a

multi-Council Water Organisation (“WO”) under the Local

Government (Water Services) Act 2025 (“Act”). If

established, the WO will be responsible for managing and delivering drinking

water, wastewater and stormwater[1]

within the TCC and WBOPDC boundaries. In terms of timing:

(a) TCC and WBOPDC will decide

whether to establish the WO on 2 April 2026; and,

(b) If TCC and WBOPDC decide to

proceed with the WO’s establishment, the intention is to incorporate that

WO around July 2026. The WO would then have a 1-year establishment phase before

a “go-live” date of 1 July 2027.

2. This report presents

the Commercial Term Sheet (“CTS”), which outlines the key

commercial terms that will underpin the WO’s foundation documents (the

Constitution and Shareholders’ Agreement). The CTS has been developed

through a robust due diligence process and extensive engagement with the Joint

Working Group (“JWG”), comprising representatives from TCC,

WBOPDC and Tangata Whenua. The JWG has reached consensus on all but one of the

commercial terms, and this paper seeks Council’s endorsement of the CTS

and direction on the outstanding matter.

3. Endorsing the CTS

will enable staff to begin drafting the WO’s foundation documents

following the decisions of TCC and WBOPDC on 2 April 2026. It will also provide

clarity on the governance, ownership and operational arrangements of the

proposed WO, including the establishment of a Joint Committee (“JC”)

to support strategic alignment between the shareholders, Tangata Whenua and the

WO Board. The JC will initially have a recommendatory / advisory role only, and

will sit between the shareholders and the WO Board, helping to ensure effective

governance and oversight during the WO’s establishment and beyond.

Background to the Joint Working

Group (“JWG”) and JWG recommendations within this Paper

4. In September 2025,

TCC and WBOPDC entered a Commitment Agreement to explore the establishment of a

WO. Between late 2025 and early 2026, TCC and WBOPDC have been undertaking an

establishment planning and due diligence process for the proposed WO.

5. As anticipated under

the Commitment Agreement,[2]

working group representatives[3]

from TCC, WBOPDC and Tangata Whenua formed the JWG. Part of the JWG’s

role has been to receive presentations and Issues & Options papers from

staff regarding the structure of the WO’s foundation documents (being the

WO’s company Constitution and the Shareholders’ Agreement) so that

if TCC and WBOPDC decide to proceed with the establishment of the WO on 2 April

2026, the foundation documents can be promptly prepared.

6. The JWG’s

Terms of Reference require the JWG to form a consensus view on each matter

(where possible) and then present that consensus view as a recommendation to

the respective councils for final decision making. Where a consensus view

cannot be reached, the matter is to be reported to the respective councils with

an outline of each party’s position and associated rationale.

7. To date, staff have

met with the JWG on 10 separate occasions (each JWG meeting has run for

approximately 3 hours) to work through the detail of each Issues & Options

Paper.[4]

The JWG meetings (and accompanying papers) have provided an opportunity for the

JWG members to undertake detailed consideration of each matter presented to

them.

8. In addition to the

JWG meetings outlined above, the representatives for each council have attended

weekly meetings with staff (each internal meeting has run for approximately 1

to 2 hours) where the Issues & Options Papers for the upcoming JWG meeting

have also been introduced.

9. Elected Members from